What Is a Life Insurance Policy Buyback and Should You Accept It?

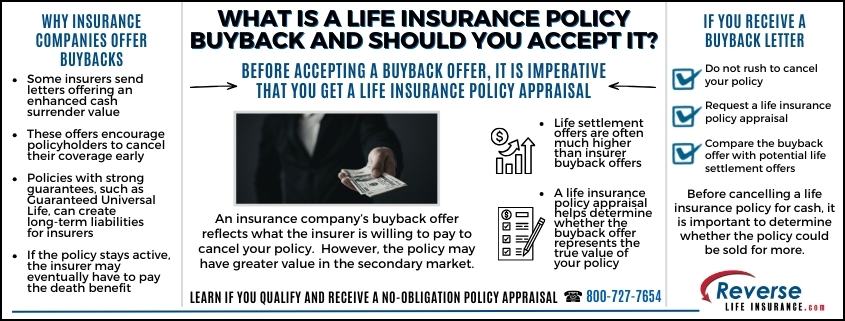

Policyholders sometimes receive a letter from their insurance company offering additional cash if they surrender their policy. This often leads people to ask: What Is a life insurance policy buyback and should you accept it? In these situations, an insurer may offer to repurchase a policy by paying more than the current cash surrender value. While these offers may appear appealing, they are often made because the insurance company believes the policy could become more valuable or costly for them in the future. Before accepting any buyback or enhanced surrender offer, it is extremely important to obtain a life insurance policy appraisal to determine the policy’s potential value in the secondary market for life insurance.

What Is a Life Insurance Policy Buyback?

A life insurance policy buyback occurs when an insurance company offers a policyholder a lump sum payment to surrender or cancel their policy. The offer may be described as an enhanced cash surrender value or a life insurance buyout offer.

If a buyback offer is accepted:

- The policy is cancelled permanently

- The insurance company keeps all prior premiums paid

- The insurer is no longer obligated to pay the death benefit

In some cases, the offer may be higher than the current cash value shown on the policy statement. The insurer may also place a deadline on the offer, encouraging the policyholder to make a quick decision.

However, accepting a buyback without first evaluating the policy’s value in the secondary market could result in leaving significant money on the table.

Why Would an Insurance Company Offer to Buy Back a Policy?

Insurance companies sometimes offer buybacks because the policy may represent a larger future liability for them. If the policy remains active until the insured passes away, the insurer must pay the full death benefit.

Certain types of policies may be more likely to receive buyback offers, particularly Guaranteed Universal Life (GUL) policies. These policies are designed to remain in force for life as long as the required premiums are paid. Unlike many other types of policies, a Guaranteed Universal Life contract can remain active even if it has little or no cash value.

Because these policies are guaranteed to pay a death claim if premiums are maintained, they can represent long-term financial obligations for insurers. Offering policyholders an enhanced surrender value can sometimes reduce that future liability.

If an insurance company is offering to buy back a policy, it may indicate that the policy has significant value.

Why a Life Insurance Policy Appraisal Matters

Before accepting any buyback or enhanced surrender offer, policyholders should strongly consider obtaining a life settlement policy appraisal.

A policy appraisal allows licensed life settlement purchasers to evaluate the policy and determine what it may be worth in the competitive secondary market. Instead of relying on a single offer from the insurance company, a policy appraisal can reveal the policy’s secondary market value.

In many cases, life settlement offers may exceed an insurer’s buyback offer because:

- Multiple institutional buyers may compete for the policy

- Buyers are willing to assume the future premium payments

- The policy’s value is determined through market competition

Without a policy appraisal, a policyholder may never know whether the buyback offer represents the highest possible value.

Comparing Buyback Offers with Life Settlements

If a policyholder decides to sell their policy, a life settlement allows the policy to be sold to a licensed purchaser rather than returned to the insurance company.

In a life settlement transaction:

- A purchaser buys the policy from the policyholder

- The purchaser becomes responsible for future premiums

- The purchaser ultimately receives the death benefit

Because life settlement purchasers are evaluating policies as investments, they may recognize value that exceeds what the insurer is offering through a buyback.

For this reason, policyholders often obtain a policy appraisal before deciding whether to accept an insurance company’s buyback offer.

Understanding the True Value of Your Policy

Life insurance policies that are no longer needed for family protection may still hold substantial financial value. When an insurance company approaches a policyholder with an offer to cancel a policy for cash, it can be a signal that the policy is worth evaluating more carefully.

Before accepting a buyback offer, taking the time to obtain a life insurance policy appraisal can provide important insight into the policy’s fair market value and help determine whether a higher offer may be available through the life settlement market.

Please give us a call at 800-727-7654. It only takes a short 5 minute conversation to learn if you’re likely to qualify for a life settlement and to find out if your policy may be worth more than what your insurance company is offering.

Do You Qualify?

Do You Qualify?