Advisers Dealing with Underperforming Universal Life

We speak with many long term financial advisers dealing with underperforming universal life insurance. Most remember writing universal life policies in the mid-eighties at 9% or more interest and having no qualms showing an illustration to that effect.

Underperforming Universal Life Policies

Though years and years of low interest rates have bolstered the stock market and the real estate market, insurance policies have largely underperformed the interest rates that were once illustrated comfortably.

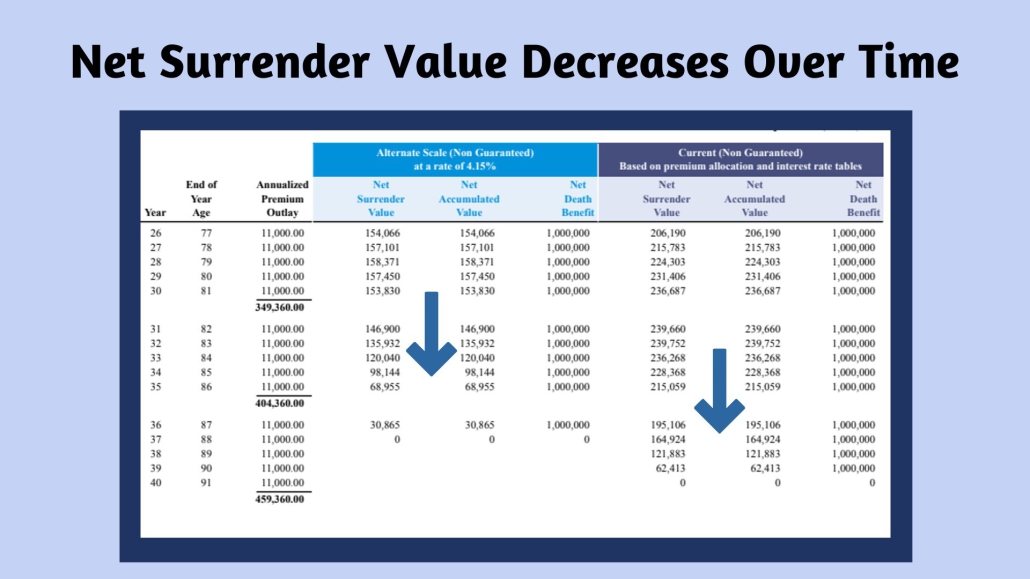

What a lot of people don’t realize is that inside of a universal life insurance policy, the cost of insurance per 1000 increases exponentially as we age. The guaranteed cost of insurance rates on most universal life insurance policies do not guarantee that the policy will stay in force until age 100. There are many different approaches to this with respect to guaranteed provisions, target premiums, etc.. No two policies are exactly the same because no two people took them out at the exact same time, from the exact same company and paid the exact same amount during a low interest rate environment.

It’s very possible, in fact probable, that many policy owners who once saw their cash value going up, now see it plateauing or decreasing due to the rising cost of insurance. The scary part is that the less cash you have, the more insurance you have to pay for as the cost per 1000 increases dramatically.

Insurance companies rely heavily on life insurance policies lapsing. The best case scenario from an insurance company’s standpoint would be that you pay premiums for years and years and they never give you any money back and they never pay a death benefit.

Most policies lapse without ever paying a claim. In fact, over 642 billion dollars in face value of life insurance policies lapsed last year.

A Viable Solution – Life Settlements

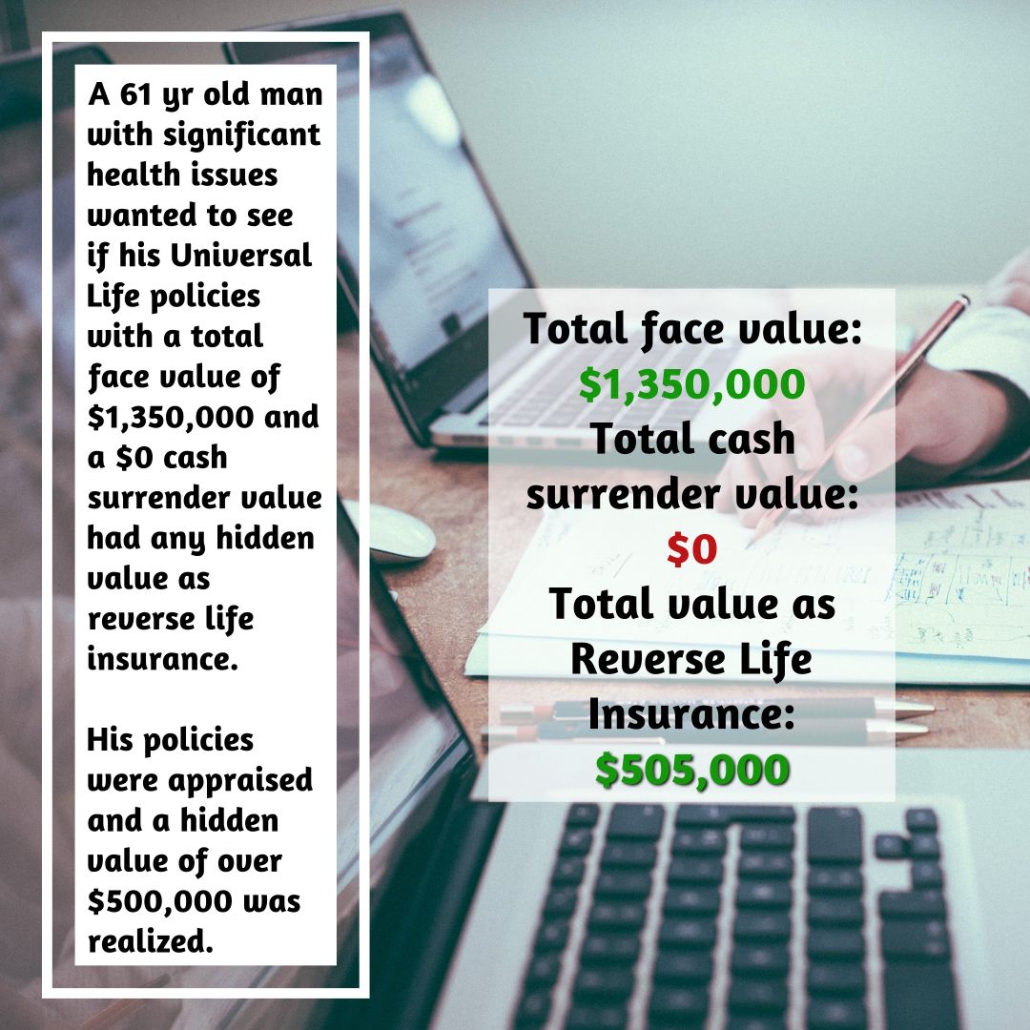

Life insurance is no longer an all or nothing proposition. Reverse life insurance allows you to get the real hidden value of an underperforming universal life insurance policy in the form of cash today. Reverse life insurance is actually the opposite of life insurance with respect to qualifying. With reverse life insurance, the worse your health and the older you are, the more your life insurance policy is likely to be worth in the secondary market.

The cash surrender value or enhanced cash surrender value offer that you see on your statements for universal life are essentially an offer from your insurance company for your life insurance policy. Your policy may have a hidden value and it is your property to sell in a life settlement versus lapse.

If you’re an adviser, revealing this possibility to your clients might allow you to once again hold your head high, in case they hung on to the illustrations that you generated 35 years ago.

Universal life insurance policies with zero cash value and ready to lapse are often prime candidates for a life settlement. If someone has had any slippage in health, there’s a chance to qualify for something if you are over age 55 or 60.

Financial advisers dealing with underperforming universal life insurance policies now have an option. Not everyone and every policy qualify. Anyone over age 50 is crazy to lapse an underperforming universal life insurance policy without first having it appraised for hidden value.

The insured’s health is the main factor, but there are many factors to consider. Different guaranteed provisions, types of policies, different carriers and their ratings all matter. Each case must be considered on an individual basis.

Insurance companies and financial advisers are being sued for not informing their clients of their ability to possibly get more for their underperforming universal life insurance policy. Please do not allow someone to throw away a universal life insurance policy with no cash value without having it appraised. The hidden value can be life changing.

Do You Qualify?

Do You Qualify?