Can You Sell a Life Insurance Policy in a Trust?

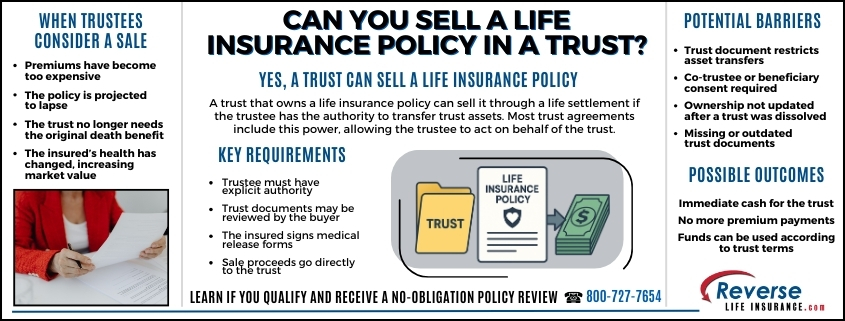

Many trustees discover that rising premiums or an underperforming universal life policy is placing financial strain on the trust. This often leads to the question of can you sell a life insurance policy in a trust and whether the trust has the authority to pursue a life settlement. In most cases the answer is yes. A trust can sell a policy just as an individual owner can, as long as the trustee has the power to transfer trust assets.

How Ownership Works When a Policy Is Held in a Trust

When a trust owns a life insurance policy, the trust is the legal policyowner. The trustee manages the policy and makes all decisions tied to it. The insured person and beneficiaries do not control the contract unless the trust agreement grants them specific rights. Because the trust is the owner, it has the ability to request illustrations, review performance, evaluate rising premium requirements, and explore alternatives such as surrendering the policy or selling it.

Many policies placed into trusts years ago were expected to perform well based on older interest rate assumptions. As market conditions changed, trustees often found themselves facing premium increases that no longer match the original funding plan. This is one of the most common situations that leads trustees to explore a life settlement.

Trustee Authority and Necessary Documentation

A life settlement can only proceed if the trustee has the authority to sell or transfer trust assets. Most trust documents include this language because trustees are responsible for managing investments and preserving the financial stability of the trust. If the trust document limits this authority, legal guidance or beneficiary consent might be required.

A buyer will review the trust agreement and any amendments to confirm who must sign the sale documents. The trustee typically signs on behalf of the trust, and the insured signs to allow the buyer to obtain medical records for valuation purposes. Beneficiaries do not usually sign anything unless the trust requires their approval.

Complications can arise when a trust has been dissolved, but policy ownership was never updated, since the insurance company may require legal documentation or a reinstated trustee before the policy can be transferred or sold.

How a Sale Affects Trust Beneficiaries

Selling the policy eliminates the future death benefit, but provides the trust with immediate cash. The trustee must then manage those funds according to the terms of the trust. In many cases, a life settlement benefits the beneficiaries because it prevents the policy from lapsing and removes the need for ongoing funding. Instead of future coverage that may no longer be affordable, the trust gains liquidity that can be used for investment, expenses, or distributions.

Trustees often choose to inform adult beneficiaries before moving forward. Open communication helps avoid misunderstandings about why the policy is being sold and how the proceeds will be handled.

Why Many Trust-Owned Policies Become Life Settlement Candidates

Trusts often hold large universal life policies purchased for estate planning purposes. These policies are more susceptible to performance issues as interest rates change. When cost of insurance charges increase or crediting rates decline, trustees may face steep premium hikes. This makes it difficult to keep coverage in force without altering the trust’s broader financial plan.

A life settlement is often considered when:

• The trust no longer needs the original death benefit

• Premiums have become unsustainable

• The insured’s health has changed, increasing the policy’s market value

• The policy is at risk of lapsing

• Trustees want to reallocate trust assets toward more stable investments

These factors can significantly increase the cash value of a policy on the secondary market.

Steps for a Trustee to Sell a Trust-Owned Policy

Trustees follow a simple process when exploring a policy sale.

- Review the trust agreement to confirm authority.

- Request an appraisal to determine the policy’s market value.

- Provide in-force illustrations and trust documents to the buyer.

- Evaluate the offer and compare it to surrender value and ongoing funding needs.

- Complete the closing documents if the offer makes financial sense for the trust.

Once completed, the trust receives the sale proceeds directly.

When Selling the Policy Makes Sense

A trust-owned life insurance policy can be a strong candidate for a life settlement when premiums increase, funding becomes uncertain, or the trust no longer needs the original coverage. Trustees who understand their authority and review the policy’s current performance can determine whether a sale would provide greater value than keeping the policy in force. Selling the policy may offer the trust immediate liquidity and a more sustainable financial path forward.

To learn if your policy is a candidate for a life settlement, please give us a call at 800-727-7654.

Do You Qualify?

Do You Qualify?