The impact of inflation on life settlements can affect the amount of hidden value your policy has.

The impact of inflation on life settlements can affect the amount of hidden value your policy has.Inflation is a financial reality that affects everyone, especially those on fixed incomes. As prices rise and the cost of living increases, seniors and retirees often face difficult financial decisions. One option that has gained attention is the sale of life insurance policies through life settlements. The impact of inflation on life settlements is significant and worth considering for anyone exploring this option as part of their financial planning strategy.

Understanding Life Settlements

A life settlement is a financial transaction in which a policyholder sells their life insurance policy to a third-party buyer for a lump sum cash payment. The buyer takes over the ownership and beneficiary rights to the policy, pays the premiums, and collects the death benefit when the insured person passes away. For many seniors, this can be an attractive option, especially if they no longer need the policy or can no longer afford the premiums.

Life settlements offer an alternative to surrendering a policy for its cash value or allowing it to lapse. By selling the policy, the policyholder can receive a lump sum that is greater than the surrender value but less than the death benefit.

Inflation and Its Effects on Retirement

Inflation erodes purchasing power over time, meaning that the same amount of money buys less as prices rise. For retirees, who often rely on fixed incomes from pensions, Social Security, or retirement savings, inflation can pose a significant threat to financial stability.

As inflation increases, so do the costs of healthcare, housing, food, and other essential expenses. This can create a gap between income and necessary spending, forcing retirees to look for ways to supplement their income. Selling a life insurance policy through a life settlement becomes a viable option for many, particularly when they are facing unexpected financial challenges due to rising prices.

The Role of Inflation in Determining Life Settlement Value

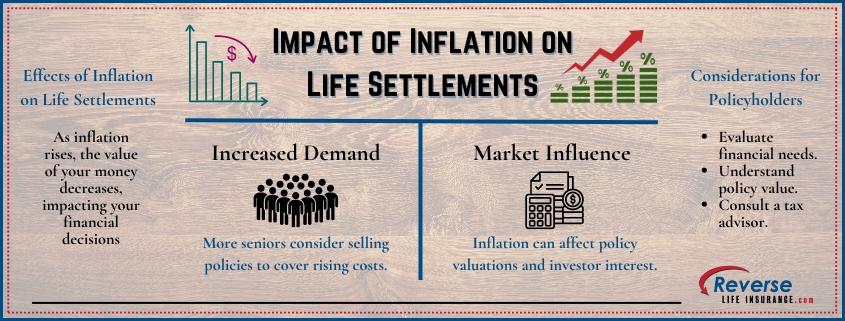

The impact of inflation on life settlements is twofold. First, inflation can increase the attractiveness of life settlements as policyholders seek additional funds to cover rising expenses. Second, inflation can influence the secondary market value of life insurance policies themselves.

As inflation drives up the cost of living, more seniors may consider selling their life insurance policies to access the policy’s hidden value immediately. This increased demand can lead to more competitive offers from life settlement purchasers. In other words, the need for liquidity among seniors can create a more favorable market for selling policies.

However, inflation can also affect the buyers of life settlements. Investors who purchase life insurance policies through life settlements must consider the future value of the death benefit in the context of inflation. If inflation is expected to remain high, the future value of the death benefit may be worth less in real terms, making the policy less attractive to buyers. This could result in lower offers for certain life insurance policies.

Strategic Considerations for Policyholders

Given the impact of inflation on life settlements, it is crucial for policyholders to carefully evaluate their options before selling a policy. Here are some key considerations:

- Current and Future Financial Needs: Consider your current financial situation and how inflation is affecting your budget. If you anticipate needing more cash to cover rising expenses, a life settlement may provide a solution. However, it’s essential to weigh this against the long-term benefit your life insurance policy could provide to your beneficiaries.

- Policy Valuation: The value of your life insurance policy in a life settlement is influenced by factors such as your age, health, and the policy’s death benefit. Inflation can impact these factors, so it’s important to work with a reputable life settlement company who can offer an appraisal of your policy’s value in the current economic environment.

- Tax Implications: Life settlements are generally subject to taxation, with different portions of the payout being taxed as ordinary income, capital gains, or not at all. Inflation can influence tax brackets and rates, so it’s wise to consult with your trusted tax advisor to understand how selling your policy could affect your tax situation.

- Alternative Income Sources: Before deciding on a life settlement, consider other ways to supplement your income. For example, you may have investments, assets, or other retirement savings that could be leveraged without selling your life insurance policy. Comparing the potential returns and risks of different options is crucial in an inflationary environment.

The Future Outlook for Life Settlements in an Inflationary Economy

As inflation continues to be a concern for retirees, the demand for life settlements is likely to grow. This could lead to a more competitive market, potentially benefiting policyholders looking to sell their policies. The future outlook will also depend on broader economic conditions, including interest rates, market stability, and the overall performance of the life insurance industry.

For investors, life settlements may remain an attractive asset class, offering diversification and the potential for returns that are not directly tied to traditional financial markets. However, they will need to factor in inflation when evaluating potential returns, which could impact the prices they are willing to pay for life insurance policies.

For policyholders, the key takeaway is that inflation adds another layer of complexity to the decision to sell a life insurance policy. While life settlements can provide much needed liquidity, especially in a high-inflation environment, it’s essential to approach the decision with careful consideration of all factors involved.

The impact of inflation on life settlements is an important consideration for anyone thinking about selling their life insurance policy. As inflation continues to affect the cost of living, life settlements may become an increasingly attractive option for retirees seeking to supplement their income. Policy owners should carefully evaluate their financial situation, the value of their policy, and the potential implications of selling before making a decision. By understanding how inflation influences the life settlement market, seniors can make more informed choices that align with their long-term financial goals.

To find out if you are likely to qualify for a life settlement or any other Reverse Life Insurance solution, such as a viatical settlement or term life settlement, please give us a call at 800-727-7654.

Do You Qualify?

Do You Qualify?