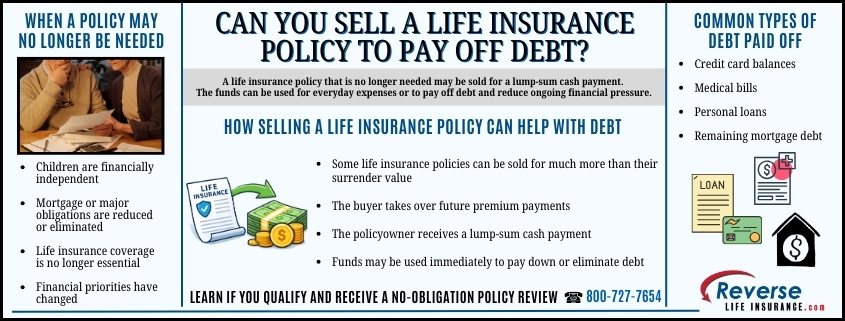

If you are struggling with debt and no longer need your life insurance coverage, you may be wondering whether the policy itself can be used as a financial resource. Many policyowners ask, “Can you sell a life insurance policy to pay off debt?” In some situations, the answer is yes. A life settlement or viatical settlement may allow you to sell an existing policy for a lump-sum cash payment that can be used to address outstanding financial obligations.

When a Life Insurance Policy Is No Longer Needed

Life insurance is often purchased during working years to protect dependents or cover specific financial responsibilities. Over time, those needs can change. Children may become financially independent, a mortgage may be paid down, or retirement income may be sufficient to support a surviving spouse. In these situations, a policy that once served an important purpose may no longer be essential.

At the same time, debt can become more difficult to manage later in life. Credit card balances, medical bills, personal loans, or even remaining mortgage debt can place pressure on a fixed income. When a policy is no longer needed for its original purpose, selling it rather than letting it lapse or surrendering it may provide access to funds that can be used to reduce or eliminate debt.

How Selling a Life Insurance Policy Works

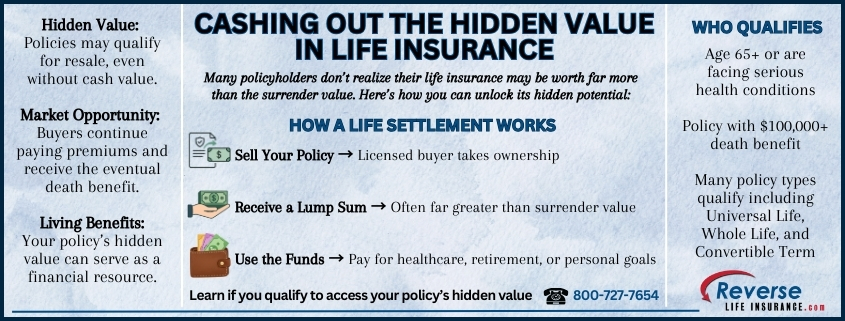

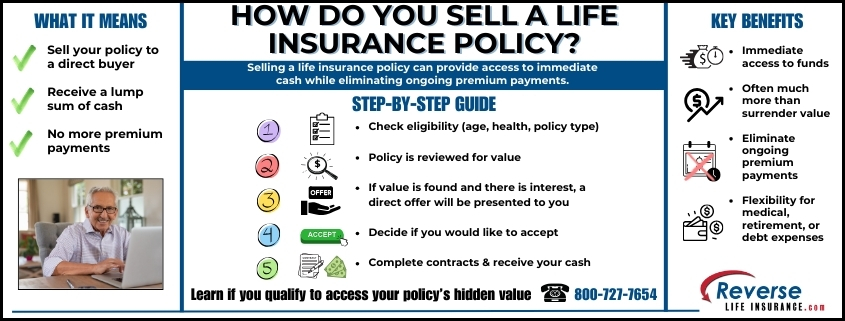

Selling a life insurance policy involves transferring ownership and beneficiary rights to a third party in exchange for a cash payment. The buyer takes over future premium payments and receives the death benefit when the insured passes away. The amount paid to the policyowner is typically much more than the policy’s cash surrender value, but less than the death benefit.

Not all policies qualify. Buyers generally look for policies with sufficient face value, manageable premiums, and an insured whose age or health profile meets eligibility guidelines. Both permanent policies and certain term policies may qualify, especially if they are still convertible.

Using Life Settlement Proceeds to Pay Off Debt

There are no restrictions on how life settlement proceeds must be used. Once the transaction is complete and funds are received, the money belongs to the seller. Many people choose to use the proceeds to pay off high-interest credit cards, medical debt, personal loans, or other obligations that are causing financial stress.

For individuals living on retirement income or dealing with health changes, reducing debt can significantly improve monthly cash flow. Eliminating recurring payments may make it easier to cover everyday expenses or prepare for future care needs.

Selling Versus Other Policy Options

Before selling a policy, it is important to understand the alternatives. Borrowing against a permanent policy may provide temporary relief, but loans accrue interest and reduce the death benefit. Surrendering a policy often results in a much lower payout than a sale. Letting a policy lapse typically provides no financial return at all.

For policyowners who no longer need coverage, selling the policy can be a way to recover value from an asset that might otherwise go unused.

Factors to Consider Before Selling

Selling a life insurance policy is a permanent decision. Once sold, the policy cannot be reclaimed, and beneficiaries will no longer receive a death benefit. It is important to consider whether coverage may still be needed in the future and to understand any tax implications associated with the transaction.

A careful review of the policy and your financial goals can help determine whether selling makes sense. For many people, especially those with policies they no longer need, selling life insurance can be a helpful way to reduce debt and regain financial stability.

If debt is weighing heavily on your finances and your life insurance coverage is no longer necessary, selling the policy may be an option worth exploring. To learn if you qualify to access the hidden value in your existing life insurance policy as cash today, please give us a call at 800-727-7654. It usually only takes a 5-10 minute phone call to check your eligibility.

Do You Qualify?

Do You Qualify?