If you or someone you love is experiencing a serious or chronic illness, you may be wondering whether your life insurance policy can be sold for cash. Conditions that may qualify for a life settlement vary widely, but they often include health issues that reduce life expectancy or cause a significant decline in health since the time the policy was issued. Even if a condition is not considered terminal, a life settlement may still be possible.

A life settlement is the sale of an existing life insurance policy to a third party buyer for a lump sum that is greater than the policy’s surrender value, but less than the death benefit. This option can provide financial relief for individuals who no longer need their coverage or who are struggling with healthcare and living expenses due to illness.

Common Conditions That May Qualify

Some of the more commonly accepted qualifying conditions for a life settlement include:

- Advanced Cancer (including recurrence or metastasis)

- Congestive Heart Failure (CHF)

- Chronic Obstructive Pulmonary Disease (COPD)

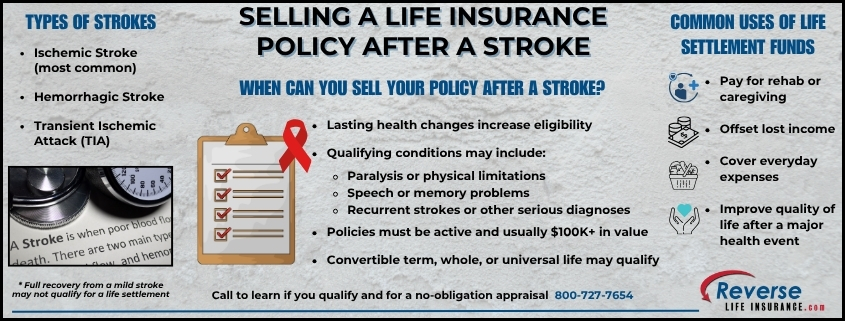

- Stroke with lasting effects

- Chronic Kidney Disease or Dialysis

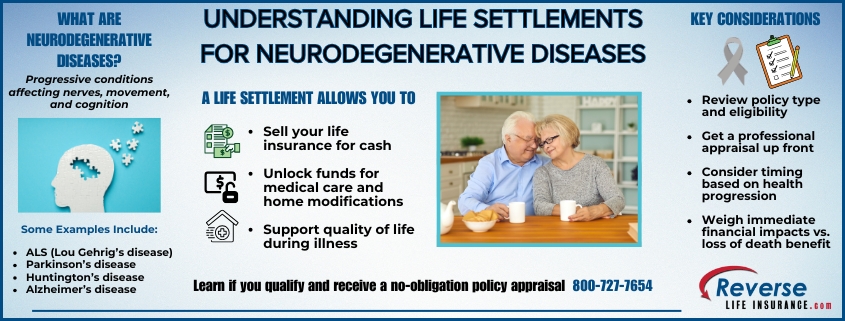

- Parkinson’s Disease

- Alzheimer’s Disease or Dementia

- ALS (Lou Gehrig’s Disease)

- Severe Diabetes with complications

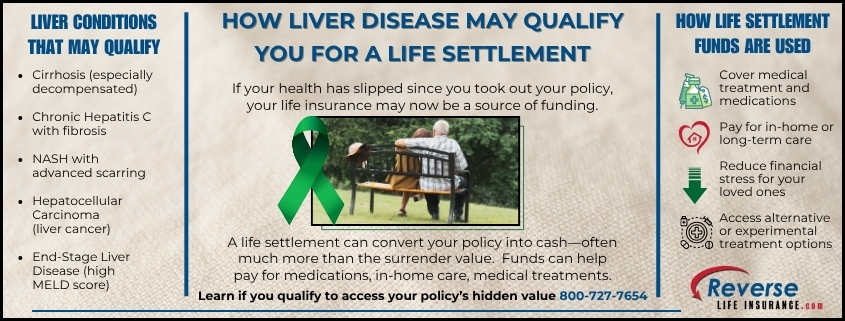

- Liver Disease or Cirrhosis

In many cases, the key eligibility factor is not the specific diagnosis but the slippage in health that has occurred since the policy was issued. If your health has declined significantly, even if the condition is managed, you may still be eligible.

Lesser-Known or Rare Conditions

While less common, the following conditions may also qualify, particularly when they limit life expectancy or cause functional decline:

- Pulmonary Hypertension

- Multiple Sclerosis (MS)

- Huntington’s Disease

- Myasthenia Gravis

- Systemic Sclerosis (Scleroderma)

- Traumatic Brain Injury (TBI)

- Septicemia (past or recurring)

- Organ Transplant Recipients

Each of these conditions may qualify depending on the specifics of the case. Factors such as the stage of the illness, rate of progression, and overall health history all play a role in determining eligibility. Even when a condition is less common, it may still meet the criteria for a life settlement based on life expectancy and policy details.

Other Factors That Affect Eligibility

In addition to the diagnosis itself, several other factors impact life settlement eligibility:

- Policy Type – Most universal life and convertible term policies qualify

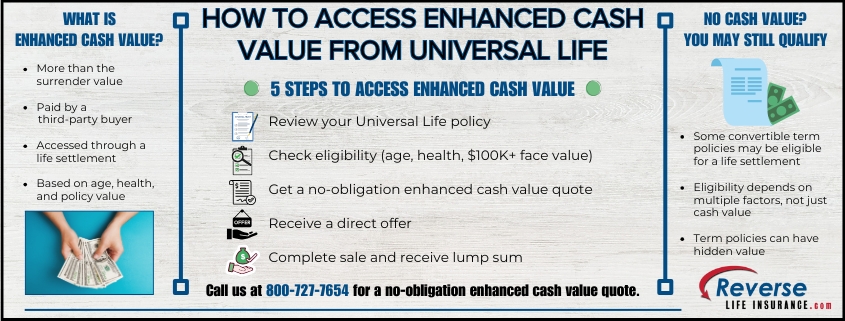

- Policy Size – Typically, policies with a $100,000 face value or more are eligible

- Health Changes – Decline in health since the time of policy issuance

- Age – Generally 65 or older, though younger individuals with serious health conditions may qualify

A Path to Financial Relief

If you’re unsure whether your condition qualifies, it’s worth exploring your options. Many people are surprised to learn that their policy still has value, even if it has no cash value or is close to lapsing. A life settlement may offer a practical way to reduce financial strain, fund care needs, or improve quality of life during a challenging time.

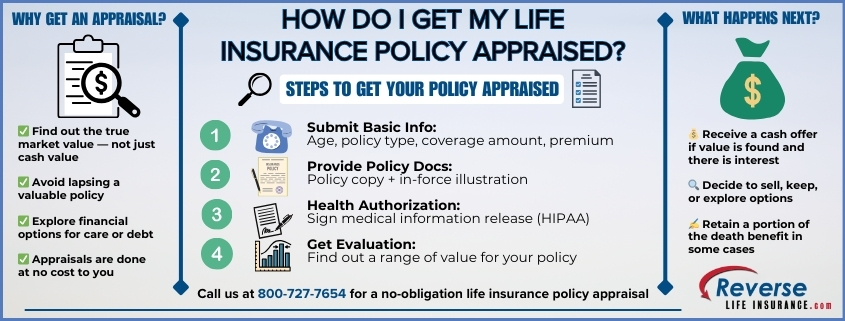

To learn if you qualify, please give us a call at 800-727-7654. In a short, 5-10 minute phone call, you can find out if your policy may have a hidden value.

Do You Qualify?

Do You Qualify?