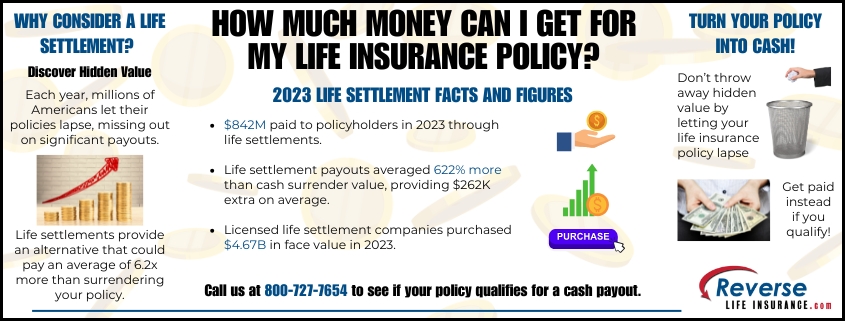

A life settlement can provide a way to access the hidden value in a life insurance policy. It allows policyholders to sell their coverage to a direct buyer in exchange for a cash payment that is often significantly higher than the policy’s surrender value. Many times, people consider this choice when premiums have become difficult to manage, when their financial needs change, or when the policy is no longer needed for family or estate protection. Selling a policy can turn something that would otherwise be surrendered or allowed to lapse into an important financial resource. But how do you sell a life insurance policy? The process is more simple and straightforward than many realize.

Understanding the Basics

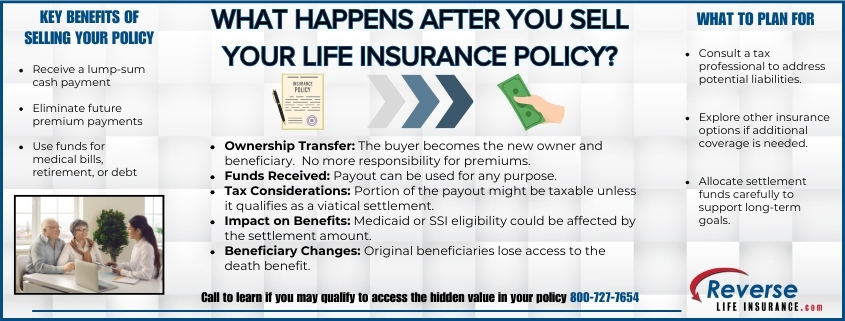

Selling a life insurance policy is not the same as canceling it with your insurance company. When you choose to sell your policy through a life settlement, ownership and beneficiary rights are transferred to a life settlement purchaser. In return, you receive a lump sum cash payment. From that moment forward, the buyer takes over premium responsibilities and eventually collects the death benefit.

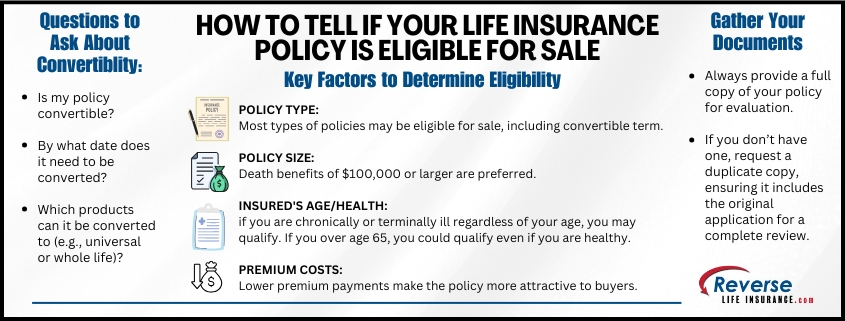

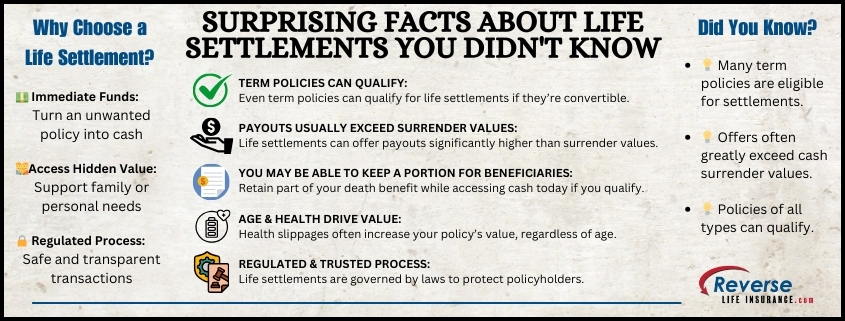

Not all policies are eligible, but many types can qualify, including universal life, whole life, and even term policies in certain situations. The most common reasons people consider selling include:

- High premium costs that are no longer affordable

- A policy that is no longer needed for family or estate protection

- A desire to access funds for retirement, healthcare, or other expenses

- A better alternative to letting the policy lapse

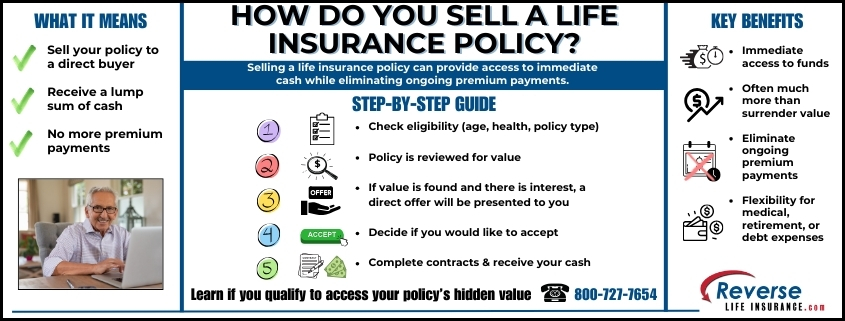

Step-by-Step Guide to Selling a Life Insurance Policy

If you are considering this option, the following steps outline the process:

- Check eligibility – Factors such as your age, health status, and policy size will determine whether you qualify. Seniors over 65 or those with serious health conditions are often the best candidates.

- Get a policy appraisal – A direct buyer will review your policy to determine its potential market value. This assessment takes into account your life expectancy, policy type, death benefit, and premium obligations.

- Receive an offer – If value is found and there is interest, a direct offer will be presented to you. When you receive a direct offer through our platform, you will never need to deduct broker fees.

- Decide if you would like to accept – If the offer makes sense for your financial needs, you can agree to the sale. Legal documents are prepared to transfer ownership and release you from future premium payments.

- Collect your cash – Once the paperwork is finalized, settlement funds are released to you in a lump sum.

Key Benefits of Selling

Selling a life insurance policy can provide immediate access to funds. Many people use the proceeds to:

- Cover long-term care or medical costs

- Pay down debt

- Supplement retirement income

- Reinvest in other financial strategies

The transaction also eliminates ongoing premium obligations, freeing up income for other expenses.

Considerations Before You Sell

Although selling your life insurance policy can be highly beneficial, there are some important points to consider:

- Tax implications – Are life settlement proceeds taxed? Depending on your settlement amount and policy basis, you may owe taxes on part of the proceeds.

- Impact on beneficiaries – Once sold, your family or loved ones will no longer receive the death benefit.

In many cases, the benefits of an immediate lump sum of cash provide far greater value than keeping a policy you no longer need, making a life settlement a worthwhile option for many policyholders.

Is Selling Your Life Insurance Policy Right for You?

Selling a life insurance policy is a decision that can bring financial relief and flexibility. By learning the process and considering your options, you can decide whether a life settlement is the right choice for your situation. If you find yourself asking, “How do you sell a life insurance policy?”, the steps outlined in this guide can help you take the next step toward unlocking the hidden value in your coverage.

To learn if you qualify, please give us a call today at 800-727-7654.

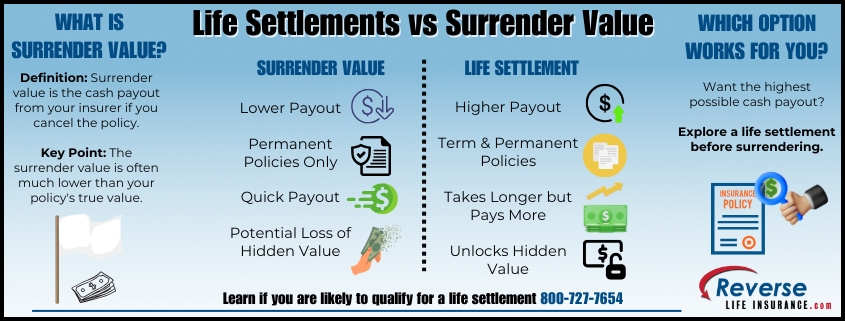

Learn the benefits of life settlements vs surrender value and which option is best for you.

Learn the benefits of life settlements vs surrender value and which option is best for you.

Do You Qualify?

Do You Qualify?