A Viatical Settlement enables qualified Policy Owners with Chronic or Terminal illness to sell their life insurance policy, providing funds for medical expenses and alternate treatments.

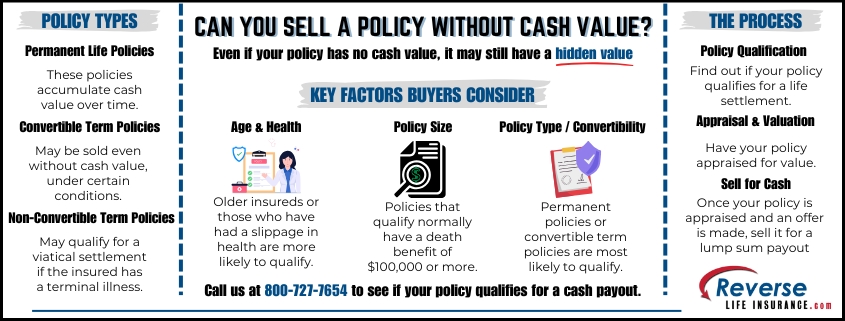

When most people think of selling a life insurance policy, they assume it must have significant cash value. But can you sell a policy without cash value? Surprisingly, even policies without cash value can sometimes be sold through a life settlement. Whether it’s a term policy that’s nearing expiration or a policy without any accumulated savings, there are options available for converting it into cash. This post will explain how the life settlement process works for policies with no cash value, what factors buyers consider, and how to determine if selling your policy is a viable option.

Understanding Policies with No Cash Value

Most people are familiar with permanent life insurance policies, like whole life or universal life, that accumulate a cash value over time. While this cash value increases the policy’s overall worth, it’s not the only factor that makes a policy eligible for a life settlement. Convertible term life insurance policies, which have no cash value, can also be sold in certain circumstances. Even though these policies lack an investment component, buyers may still be interested if the policyholder meets specific criteria, such as age or health condition. Non-convertible term policies may potentially qualify for a viatical settlement if the insured has a terminal illness, offering a financial lifeline in times of need.

Why Would Someone Buy a Policy Without Cash Value?

Life settlement buyers are primarily interested in the death benefit of the policy. If a policyholder has a term life insurance policy that’s nearing its expiration date or if they no longer need the coverage, a buyer may purchase the policy in exchange for a lump sum. In return, the buyer becomes the new beneficiary and takes on the responsibility of paying the premiums. When the original policyholder passes away, the buyer collects the death benefit. Even though there’s no cash value in the policy, the future payout from the death benefit makes it a valuable asset for life settlement companies.

Factors That Impact the Sale

Several factors influence whether a life settlement buyer will purchase a policy with no cash value. The most critical considerations include:

Policyholder’s Age and Health: The older the policyholder or the more significant their health issues, the more likely a life settlement company will be to purchase the policy. Buyers have to factor in how long they are likely to be paying policy costs when determining their offer.

Policy Size: Larger death benefits are more attractive to buyers, even for policies without cash value. Policies must typically have a death benefit of $100,000 or more to qualify.

Policy Term Length: For term policies, the remaining length of coverage is important. It’s always a good idea to have your policy appraised for its value at least six months before your conversion period deadline if possible.

Options for Term Life Insurance

If you have a term life policy with no cash value, you may still be able to sell it in a term life insurance settlement. Policies that are convertible to permanent insurance are particularly attractive because they can be extended into the future. Even if your policy is not convertible, there may be interest if the policyholder meets certain age or health requirements. Non-convertible policies with a terminally ill insured may also qualify for a viatical settlement, providing a critical source of funds.

Is Selling Your Policy Right for You?

Selling a life insurance policy without cash value can provide immediate financial relief. If you no longer need the coverage or the premiums have become unaffordable, a life settlement might be a practical option to access hidden value within your policy.

You don’t need a policy with cash value to take advantage of a life settlement. If you’re curious about whether your policy qualifies, especially if it’s a convertible term life insurance policy, now is the time to explore your options. Even policies without cash value may be eligible to be sold, potentially giving you access to a significant cash payout when you need it most. To find out if you’re likely to qualify and unlock value from your policy, give us a call at 800-727-7654.

If you’re considering selling your life insurance policy, one important question to address is: are life settlement proceeds taxed? The answer isn’t straightforward, as it depends on a number of factors, including your cost basis, the amount you receive, and whether the policy is classified as a term or permanent policy. In this post, we will break down how life settlements are taxed and help you understand what you might owe in taxes after cashing in your life insurance policy.

What is a Life Settlement?

A life settlement is a financial transaction where a policyholder sells their life insurance policy to a third party for a lump sum cash payment. Typically, the payment is higher than the surrender value offered by the insurance company but lower than the death benefit. Life settlements can be an attractive option for those who no longer need or want to keep paying premiums on their policy, are facing financial challenges, or are interested in monetizing their policy to improve their quality of life.

Taxation Basics for Life Settlements

The proceeds from a life settlement can be subject to taxes, but the specific tax treatment depends on a variety of factors. The Tax Cuts and Jobs Act (TCJA) of 2017 also impacted the taxation of life settlements, altering some of the rules around policy valuation and reporting requirements. It’s important to understand how these changes may affect the tax treatment of your life settlement. Let’s break down the general rules for life settlement taxation.

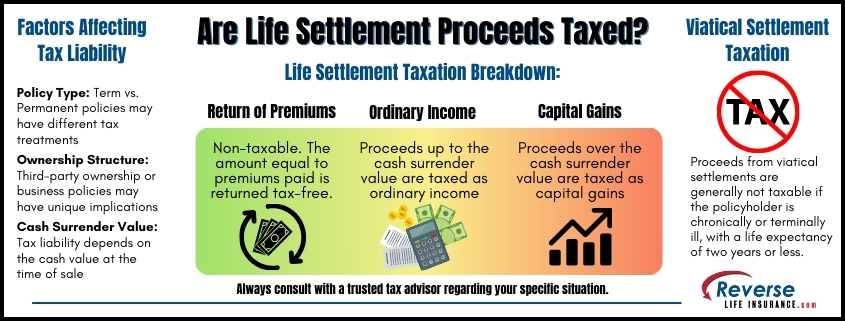

Return of Premiums

The first portion of the life settlement proceeds, up to the amount of premiums you’ve paid, is generally considered a return of your investment and is not subject to income tax. For example, if you have paid $50,000 in premiums over the life of the policy and receive $100,000 from the sale, the first $50,000 would be tax-free.

Taxation of Gains Above Cost Basis

Once you exceed the amount you have paid in premiums (your cost basis), the next portion is considered a gain. This gain is subject to income tax, but the classification of that tax depends on the nature of the gains.

Capital Gains Tax

If the proceeds you receive from the sale exceed the cost basis but do not exceed the policy’s cash surrender value, the difference is treated as ordinary income. Any amount above the cash surrender value may be considered a capital gain, which could qualify for lower tax rates.

In summary, life settlement proceeds are typically divided into three categories:

The return of premiums (not taxable)

Ordinary income (taxable up to the policy’s cash value)

Capital gains (taxable at capital gains rates for any amount above the cash value)

An Example of Life Settlement Taxation

To make this clearer, let’s look at an example. Suppose you have a life insurance policy for which you have paid $60,000 in premiums. The cash surrender value of the policy is $80,000, and you manage to sell it for $120,000 in a life settlement.

The first $60,000 you receive is not taxable because it represents the return of the premiums you paid.

The next $20,000 (which represents the difference between your cost basis and the cash surrender value) is taxable as ordinary income.

The remaining $40,000 (the amount over the cash surrender value) is taxable as a capital gain.

Factors that Affect Taxation

There are several factors that can affect how much tax you owe on your life settlement proceeds:

Policy Type

The type of life insurance policy (permanent vs. term) can influence the taxation. For instance, term policies may be eligible for different treatment since they often lack a cash surrender value.

Ownership and Beneficiaries

If the policy was part of a business, or if a third party paid the premiums, the tax implications might be different. Ownership structure plays a crucial role in determining taxable events.

Age and Health

Your age and health condition might also influence the settlement offer and taxation implications. Generally, older policyholders or those with health concerns might receive higher offers, impacting how much is taxable.

Are There Any Exemptions?

In certain circumstances, life settlement proceeds may be tax-exempt. For instance, if the policy qualifies as a viatical settlement—meaning it was sold by someone who is chronically or terminally ill—then the proceeds are often entirely exempt from taxation. Viatical settlements are treated differently because they are considered to be an advance of the death benefit and a source of financial support for individuals dealing with severe health challenges.

Consult a Tax Professional

It’s essential to consult with a trusted tax professional to make sure you understand the tax implications. The TCJA introduced new reporting requirements for insurance companies, which means you may need to provide additional documentation when filing your taxes. A tax advisor can help you navigate these complexities. Tax rules can be complicated, and missteps can be costly. A tax advisor can help you determine your cost basis, calculate potential taxes owed, and even explore strategies to minimize your tax liability. Since the IRS treats life settlements differently depending on each policyholder’s unique situation, professional advice can ensure you fully understand your obligations.

Other Financial Considerations

Beyond taxation, there are additional financial implications to consider before deciding on a life settlement:

Impact on Government Benefits: Receiving a lump sum from a life settlement could impact your eligibility for certain government benefits, like Medicaid. It’s important to understand how the extra income will affect your financial standing. A medical life settlement might be a valuable option if this is a concern for you.

Estate Planning: If your life insurance policy was part of your estate plan, selling it may impact the inheritance you leave behind. The death benefit that would have gone to your beneficiaries will be forfeited once the policy is sold.

So, are life settlement proceeds taxed? Yes, in most cases, life settlement proceeds are taxable, but how much you owe will depend on factors like your cost basis, the cash surrender value, and whether the policy qualifies as a viatical settlement.

Understanding the tax implications is important. If you’re considering a life settlement, it’s wise to understand the financial and tax consequences fully. Consult with a tax advisor and evaluate your options carefully to ensure that you make the best decision for your financial future.

To learn if you are likely to qualify for a life settlement, please give us a call today at 800-727-7654.

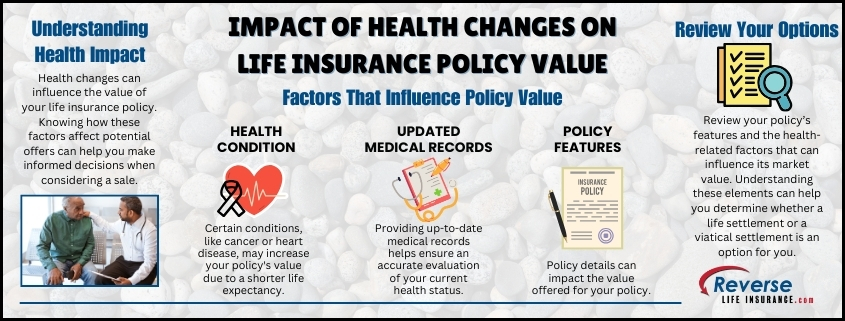

Health changes can significantly affect your life insurance policy’s hidden value, especially if you’re considering selling it in the secondary market for life insurance. Understanding the impact of health changes on life insurance policy value can help you determine the best time to pursue a life settlement and maximize your payout. When health declines, the perceived risk to buyers decreases, potentially raising the market value of your policy.

How Health Affects Life Settlement Value: What You Need to Know

When it comes to selling life insurance, one of the most critical factors influencing its value is the insured’s health status. In the life settlement market, potential buyers assess policies based on the policyholder’s life expectancy, which means recent health changes can greatly impact the policy’s worth. For instance, a diagnosis of a severe medical condition, such as cancer, heart disease, or ALS may increase the value of the life insurance policy to investors. This is because a reduced life expectancy typically can make the period for a payout shorter, meaning the buyer would likely receive the death benefit sooner.

Understanding how health conditions affect life settlement offers can be crucial for policyholders considering selling. If a chronic illness or other serious medical diagnosis has reduced life expectancy, it may lead to higher offers for the life insurance policy. Conversely, if health improves or a medical condition stabilizes, the policy’s value might decrease because potential buyers would anticipate a longer time frame for payout. Knowing when to sell a life insurance policy due to health changes can therefore make a significant difference in the financial outcome.

Viatical Settlements vs. Life Settlements: What’s the Difference?

While life settlements are often an option for policyholders with declining health, it’s important to understand the distinction between life settlements and viatical settlements. Viatical settlements are specifically designed for individuals who have been diagnosed with a terminal illness or other medical conditions qualifying for viatical settlements, with a life expectancy of two years or less. In these cases, the policyholder may be able to receive a higher payout because the death benefit is expected to be paid sooner.

On the other hand, life settlements do not require the policyholder to have a terminal illness. Individuals with less serious health conditions, such as manageable chronic illnesses or age-related health declines, may still qualify for a life settlement. While the payout may be lower compared to a viatical settlement, it can still provide a significant amount of cash for those looking to liquidate an unneeded life insurance policy. Understanding the difference between these options can help you decide which may be most suitable based on your health situation.

Why Medical Conditions Can Increase the Market Value of Your Life Insurance Policy

Investors looking to buy life insurance policies in the life settlement market are often willing to pay more if they believe the policyholder’s health issues will lead to a shorter life expectancy. Health conditions such as advanced diabetes, cancer, or severe heart disease can significantly increase the market value of a life insurance policy because these conditions indicate a reduced period before the death benefit is expected to be paid out. Even less severe health issues can impact the value of life insurance if they are expected to shorten the life expectancy to some degree.

However, if a policyholder experiences health improvements due to a new treatment or lifestyle changes, this can affect the value in a negative way. When a medical condition improves or stabilizes, it may indicate a longer life expectancy, prompting potential buyers to lower their offers because they would anticipate paying premiums for a more extended period before receiving the death benefit.

Maximizing Life Settlement Offers When Your Health Changes

To optimize the value of a life insurance policy in the life settlement market, understanding how health changes affect life insurance value is essential. Timing the sale to coincide with declining health can often lead to higher offers, whereas waiting too long might result in reduced offers if health improves. Selling life insurance with health issues can therefore be financially beneficial, but it’s important to know the right time to proceed. For example, after a significant health diagnosis, the market may be more favorable for selling.

Additionally, some policies may have riders or provisions that could be impacted by health changes. For instance, certain policies have accelerated death benefits that may be accessed if the insured has a very reduced life expectancy. Knowing how medical conditions and policy features interact can provide insight into whether selling the policy is the right decision.

The Importance of a Medical Underwriting Review for Life Insurance Sales

A medical underwriting review is a crucial step in determining the value of a life insurance policy in the life settlement market. During this review, independent underwriters assess the policyholder’s medical records to estimate life expectancy and evaluate the risk. The findings from this review, combined with the insured’s age and policy details, significantly impact the offers made for the policy. Accurate underwriting can better reflect how health conditions affect life settlement offers and the sale value of the policy.

For those considering selling a life insurance policy due to health changes, providing comprehensive medical records is vital. This ensures that the underwriting review accurately reflects the current health situation, potentially leading to higher offers in the market.

Strategies for Selling Life Insurance with Medical Conditions

If you have medical conditions, selling your life insurance policy can be a practical way to get more value from it. Understanding the impact of health changes on life insurance policy value is an important factor to consider. Here are a few strategies:

Know how medical conditions affect policy value: Different health conditions can influence the market value of a life insurance policy in various ways. Diagnoses like cancer or heart disease may increase the amount offered by life settlement providers, depending on the specifics of the condition.

Keep documentation updated: Providing accurate and up-to-date medical records during the medical underwriting review ensures the current health situation is properly evaluated, which may result in a better offer.

Be aware of policy details: Some life insurance policies have features that could affect the settlement offer. Understanding your policy’s terms can help set realistic expectations.

These factors can play a significant role in determining how much you might receive for your life insurance policy. Please give us a call at 800-727-7654 to learn if you’re likely to qualify to sell your policy for cash through a life settlement or a viatical settlement.

Did you know that you can turn your life insurance into cash when it’s no longer needed or becomes too costly to maintain? Many policyholders are unaware that selling their life insurance policy is an option that can provide significant financial relief. Known as a life settlement, this process allows you to sell your life insurance to a third party for more than its cash surrender value, but less than the death benefit, giving you immediate funds to meet current needs.

If your policy no longer fits your financial goals or is becoming a burden, a life settlement might be the right option for you.

What Is a Life Settlement?

A life settlement is a transaction where a policyholder sells their life insurance policy to a buyer in exchange for a cash payout. The buyer takes over premium payments and becomes the beneficiary, receiving the death benefit when the insured passes away. Life settlements offer policyholders a way to access the value of their life insurance while they are still alive, rather than surrendering it back to the insurance company for minimal value or letting it lapse.

This process has become more common as more people look for ways to tap into their assets to cover costs like healthcare, retirement, or simply to improve their quality of life. Instead of canceling a policy that no longer serves you, you can turn life insurance into cash that can be used for various needs.

Who Qualifies for a Life Settlement?

Not everyone will qualify for a life settlement, but several factors increase your chances of eligibility:

Age and Health: Seniors age 65 and older with declining health are typically the best candidates for life settlements. Buyers are looking for policies with a shorter life expectancy to receive a return on their investment sooner. When appraising a policy for value, the buyer must consider the amount of time they will be paying premiums on the policy.

Policy Size: Larger policies are more attractive to buyers, with most life settlements involving policies worth $100,000 or more. Some smaller policies may still qualify. If you are unsure, please give us a call to learn if yours may be eligible.

Type of Policy: While universal life and whole life policies are the most common for life settlements, some term life policies can also be sold in a term life insurance settlement, depending on their conversion options and the insured’s health. Convertible policies may be able to be sold, even if the insured is in relatively good health. Non-convertible term policies may be eligible if the insured has a terminal diagnosis.

The life settlement market is growing, giving more flexibility to policyholders who might otherwise let their policies lapse. However, each case is unique, and eligibility will depend on several individual factors.

Why Turn Life Insurance into Cash?

There are many reasons someone might choose to sell their life insurance policy:

Premiums Are Too Expensive: As you age, life insurance premiums can increase, especially for universal or whole life policies. If paying those premiums becomes a financial strain, selling the policy can relieve you of this burden while still giving you access to the policy’s value.

Life Changes: Perhaps your original reasons for purchasing life insurance have changed. You may no longer have dependents relying on the policy’s death benefit, or your financial situation may have improved to the point where the coverage is no longer necessary. As you are planning future financial goals, it may be worth reconsidering whether the policy still aligns with your needs.

Medical Expenses: Seniors often face significant medical costs that can drain savings and retirement funds. A life settlement provides a lump sum of cash that can be used to cover those expenses without depleting other assets.

Supplement Retirement Income: Many people use life settlements to enhance their retirement lifestyle. Selling a life insurance policy can provide additional sources of retirement income to travel, pursue hobbies, or enjoy a higher quality of life during retirement.

Debt Relief: If you have outstanding debts, a life settlement may be able to provide the funds necessary to pay them off, relieving financial stress and ensuring that your estate is debt-free for your heirs.

How Much Cash Can You Get?

The amount of money you can receive from selling your life insurance policy depends on several factors, including:

The size and type of the policy

Your age and health

The amount of premium payments remaining

The policy’s death benefit

Current market conditions for life settlements

Policy specifics and provisions

On average, policyholders receive anywhere between 10% to 30% of their policy’s death benefit, but this amount can vary widely. For example, a $500,000 life insurance policy could result in a life settlement payout of $50,000 to $150,000, depending on your circumstances. Some viatical settlements pay a much higher percentage. It is always wise to have your policy appraised for hidden value.

The Life Settlement Process

The process of turning your life insurance into cash is relatively straightforward. Here are the steps:

Policy Review: The first step is to contact a life settlement company who will review your policy to determine whether it’s a good candidate for a life settlement.

Application: If your policy is eligible, you may submit a formal application. This may require sharing information about your health, the policy, and your financial needs. With our direct platform, this step is greatly streamlined and you will only need to submit a few compliance forms rather than a lengthy application.

Offer Review: If your policy has value and there is interest, you’ll receive offers from interested buyers.

Accepting an Offer: Once you’ve reviewed the offers, you can accept the one that best meets your financial goals. The sale process will begin, and you’ll receive a lump sum payment in exchange for transferring ownership of the policy.

Completion: The buyer takes over the policy’s premium payments and becomes the beneficiary, while you receive cash and no longer have any obligations regarding the policy.

Is a Life Settlement Right for You?

Turning your life insurance into cash can be an excellent option for those who no longer need the coverage or who are facing financial difficulties. However, it’s essential to consider the following:

Impact on Estate Plans: Selling your policy means your beneficiaries will no longer receive the death benefit, so it’s crucial to consider how this will affect your overall estate plans.

Tax Implications: Are life settlement proceeds taxed? Life settlement proceeds may be subject to taxes, depending on your individual circumstances. It’s a good idea to consult with a trusted tax professional to understand the tax impact of a life settlement. Typically, viatical settlement proceeds are not taxed.

Alternatives: If a life settlement isn’t the right choice for you, there are other ways to access the value of your policy, such as a loan against the policy’s cash value or surrendering it for a smaller payout. Loans do require repayment and surrendering a policy usually results in a much lower payout than a life settlement.

For many, the ability to turn life insurance into cash can provide financial freedom and peace of mind. Whether you need to cover medical expenses, supplement your retirement, or simply no longer need the coverage, a life settlement offers a practical solution.

If you’re considering selling your life insurance policy, call us today at 800-727-7654 to learn more and find out if you’re likely to qualify for a life settlement.

As life circumstances change, many policyholders find themselves reconsidering the value of their life insurance policies. If you’ve ever wondered, “Can I sell my life insurance for cash?” you’re not alone. This option is becoming popular among those looking to unlock the cash value of their policies for immediate financial needs. In this post, we’ll explore how to sell your life insurance for cash, the benefits of doing so, and key considerations to keep in mind.

What Does It Mean to Sell My Life Insurance for Cash?

Selling your life insurance policy as reverse life insurance, often referred to as a life settlement, means transferring ownership of the policy to a third party in exchange for a lump sum payment. The option to turn life insurance into cash is appealing for various reasons, from financial necessity to changing life situations. When selling a policy through a life settlement, the offer you receive will always be higher than the cash surrender value offered by the insurance company, but lower than the death benefit of the policy.

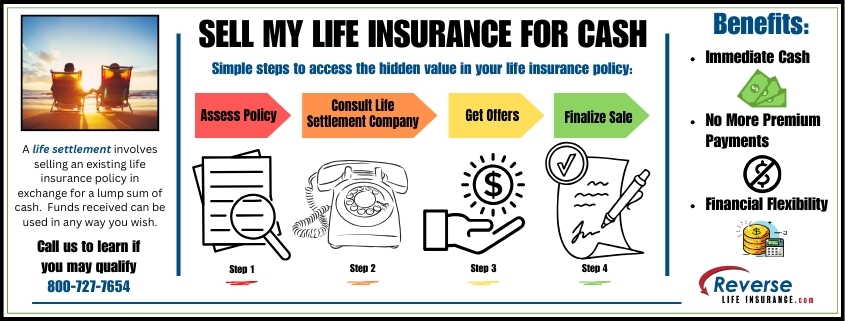

Steps to Sell Your Life Insurance Policy

The process of selling your life insurance can be straightforward if you understand the steps involved:

Assess Your Policy: Start by reviewing the details of your life insurance policy. Note the face value, type of policy, and your current health status. Policies typically eligible for sale have a face value of $100,000 or more. Some smaller policies can qualify. Please give us a call and we’ll be happy to help you learn if your policy may be eligible.

Consult with Professionals: Engage with a reputable life settlement company who can guide you through the evaluation process. They will help you determine if your policy qualifies and what its potential market value might be. Reverse Life Insurance has been helping people sell their policies direct to life settlement purchasers for nearly 20 years.

Obtain a Policy Appraisal: A thorough appraisal will consider factors like your age, health, and the policy’s terms. Life settlement companies will use this information to estimate the amount you could receive from the sale.

Review Offers: After the appraisal, you will receive offers from potential buyers if value is found and they are interested in purchasing your policy.

Complete the Sale: If you accept an offer, you’ll need to sign the necessary paperwork to transfer ownership and beneficiary rights of the policy. Once the sale is finalized, the new owner takes over premium payments and becomes the beneficiary.

Receive Your Cash: After the transfer, you will receive your lump-sum payment, providing you with immediate funds to use as needed.

Benefits of Selling Your Life Insurance

Selling your life insurance for cash can offer several advantages:

Immediate Cash Flow: The most significant benefit is the immediate access to cash. This can be crucial for paying off debts, covering unexpected expenses, or simply improving your financial situation. Some policy sellers even use the funds to pay for vacations with loved ones.

No More Premium Payments: Once you sell your policy, you are relieved of the obligation to make ongoing premium payments, which can be a significant relief.

Flexibility: The cash obtained from selling your policy can be used for a wide range of purposes—whether you want to invest in a new opportunity, fund medical expenses, or treat yourself to a long-deserved vacation.

Tailored Financial Strategy: By converting your life insurance into cash, you can reassess your financial strategy to better align with your current needs and goals.

Who Should Consider Selling Their Life Insurance?

Not every policyholder should sell their life insurance policy. However, certain situations may warrant this decision:

Changing Life Circumstances: If your financial needs have changed—perhaps you no longer have dependents or your circumstances have shifted—it may be time to reconsider the necessity of your life insurance.

Unmanageable Premium Payments: For many, the cost of premiums can become a financial burden, especially for those on fixed incomes. Selling the policy can relieve this pressure.

Underperforming Policies: Sometimes, it can be beneficial to sell an underperforming policy and use the funds received to purchase a new policy. This does not make sense for everyone, but is an option you may want to discuss with your trusted personal financial advisors.

Increased Healthcare Costs: Rising medical expenses can be a challenge. The cash received from a life insurance policy sale can help cover these costs.

Considerations Before Selling

While there are many benefits to selling your life insurance, it’s important to consider a few key factors:

Loss of Coverage: Selling your policy means you will no longer have the life insurance coverage provided by that policy. This is a critical consideration, especially if you have dependents who may rely on the death benefit. Some policyholders choose to sell only some of their policies or a portion of a policy. If you are considering a life settlement, but may be interested in a retain a portion settlement, please reach out to see if you may qualify for this option.

Tax Implications: The proceeds from selling your life insurance may be subject to taxes, depending on the difference between what you paid into the policy and what you receive from the sale. Consulting your trusted tax professional is recommended to understand your specific situation. If you qualify for a viatical settlement, the proceeds are usually tax-free.

Potentially Lower Offers: Not every policy will fetch a high price. Be prepared for the possibility that offers may not meet your expectations, especially if your health is relatively good or the market conditions are unfavorable.

Real-Life Scenarios

Consider these examples of individuals who successfully sold their life insurance for cash:

Debt Management: A retiree facing credit card debt sold their life insurance policy to pay off their balance, achieving peace of mind and financial stability. They no longer needed the policy as they did not have any beneficiaries to leave it to.

Healthcare Needs: An individual diagnosed with a chronic illness opted to sell their policy to cover mounting medical bills, alleviating financial stress during a difficult time. They were also able to pay for alternative treatments not covered by their medical insurance.

Investment Opportunities: A policyholder who no longer needed their life insurance sold their policy to invest in real estate, leading to long-term financial growth.

Selling your life insurance for cash can be a smart financial decision that offers immediate benefits and enhances your overall financial flexibility. If you’re considering this option, it’s essential to understand the process, weigh the benefits against the potential drawbacks, and consult with professionals who can guide you.

We specialize in helping policyholders navigate the life settlement process. If you’re ready to explore your options, contact us today to see if selling your life insurance policy may be an option for you. 800-727-7654

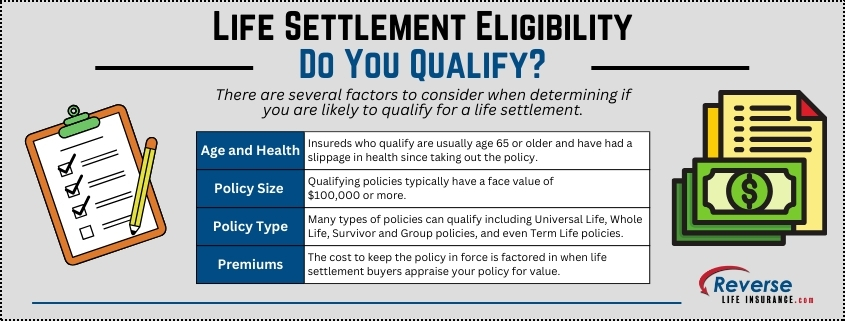

When considering a life settlement, one of the most important questions is, “Do you qualify to sell your policy?” Understanding life settlement eligibility do you qualify? is key to determining whether you can turn your life insurance policy into a cash payout. In this post, we’ll explore the factors that determine life settlement eligibility and help you assess if selling your policy is an option for you.

What Is a Life Settlement?

Before learning about eligibility, it’s important to understand what a life settlement is. A life settlement involves selling your existing life insurance policy to a third party for more than its cash surrender value, but less than its death benefit. The buyer takes over ownership and beneficiary rights to the policy, continues paying the premiums, and ultimately collects the death benefit when the insured passes away.

Many people choose a life settlement when they no longer need their life insurance or if the premiums have become too expensive. The funds from selling a policy can be used for a variety of financial needs including medical bills, retirement expenses, or even a more affordable insurance plan.

Age and Health: Two Key Factors

The first major factor in determining your eligibility for a life settlement is your age and health status. Typically, seniors that qualify for a life settlement are 65 or older, but this can vary based on health condition.

Age Requirements:

The general benchmark for qualifying is being at least 65 years old, but insureds who are younger may qualify if they have a chronic or terminal health condition. It is always best to give us a call to discuss your unique case.

Health Condition:

Health is a crucial aspect of life settlement eligibility. Buyers are more interested in policies from individuals with shorter life expectancies because they’ll receive the death benefit sooner. While you don’t need to be terminally ill, those with chronic or serious medical conditions are more likely to qualify.

Policy Size and Type Matter

The type and size of your life insurance policy can also impact your eligibility for a life settlement.

Policy Size:

Most life settlement purchasers look for policies with a face value (death benefit) of $100,000 or more. While smaller policies can sometimes qualify, they may not be as attractive to investors.

Policy Type:

Almost all types of life insurance policies can be sold in a life settlement. However, some policies are more appealing to buyers:

Universal Life: These policies are highly attractive because they offer flexibility in premium payments and potential cash value growth.

Term Life: Term policies can be eligible, but usually only if they can be converted into a permanent policy. Some non-convertible term policies may qualify for a viatical settlement if the insured is dealing with a serious health concern.

Whole Life: Whole life policies often qualify due to their guaranteed coverage and built-in cash value.

Variable Life: While more complex, variable life policies can also qualify.

Premium Amounts and Cash Surrender Value

Another factor affecting a policy’s eligibility for a life settlement is the amount of premium payments. Potential buyers will factor in costs to keep the policy in force over your expected lifetime when calculating an offer.

In some cases, policies with a high cash surrender value can still qualify for a life settlement, but this is generally not ideal for a life settlement. If your policy has no or little cash value, it can be more likely to qualify.

How Long Have You Held the Policy?

Most life settlement companies require that policies have been in force for at least two years. This is due to contestability clauses. If your policy is relatively new, it may not yet be eligible for a life settlement.

Financial and Legal Considerations

While not a direct factor in determining eligibility, there are several financial and legal considerations that can impact your decision to sell your policy.

Outstanding Loans on the Policy:

If you have taken out loans against your life insurance policy, this can reduce its overall value in a life settlement. Some buyers may still be interested, but they will deduct the loan balance from any offer they make.

Legal Ownership:

You must be the legal owner of the policy in order to sell it. If the policy is part of a trust or another entity holds ownership, a principal, such as a trustee, must be available to sign initial paperwork and the contract should you proceed with a sale.

Beneficiary Concerns:

If you’re considering selling your policy, it’s important to consider the needs of your beneficiaries. Once the policy is sold, the buyer becomes the new beneficiary, and your heirs will no longer receive the death benefit. Discussing this decision with your family can help avoid misunderstandings later on.

Getting a Life Settlement Valuation

If you’re unsure whether your policy qualifies for a life settlement, the best first step is to contact us for a no obligation policy appraisal. After learning your age, policy type and premiums, and approximate health condition, we will be able to let you know if you are likely to be eligible for a life settlement or viatical settlement.

A valuation can give you a better idea of what to expect, and whether it’s worth pursuing a life settlement based on your specific circumstances.

Should You Pursue a Life Settlement?

Deciding whether to sell your life insurance policy through a life settlement is a personal decision that depends on your financial situation, health, and future needs. While many seniors find life settlements to be a valuable source of extra income, it’s important to weigh the pros and cons carefully. If you no longer need your policy or can’t afford the premiums, selling it might be a smart financial move.

Life settlement eligibility depends on several factors, including your age, health, policy type, and size. While every situation is unique, understanding these core aspects can help you determine whether selling your policy is the right choice. If you think you might qualify, the next step is to consult a life settlement company for an initial evaluation.

Please give us a call at 800-727-7654 to learn if you are likely to qualify to sell your policy for cash.

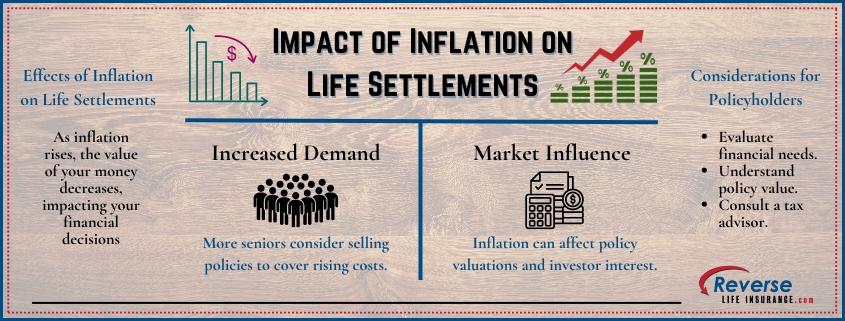

Inflation is a financial reality that affects everyone, especially those on fixed incomes. As prices rise and the cost of living increases, seniors and retirees often face difficult financial decisions. One option that has gained attention is the sale of life insurance policies through life settlements. The impact of inflation on life settlements is significant and worth considering for anyone exploring this option as part of their financial planning strategy.

Understanding Life Settlements

A life settlement is a financial transaction in which a policyholder sells their life insurance policy to a third-party buyer for a lump sum cash payment. The buyer takes over the ownership and beneficiary rights to the policy, pays the premiums, and collects the death benefit when the insured person passes away. For many seniors, this can be an attractive option, especially if they no longer need the policy or can no longer afford the premiums.

Life settlements offer an alternative to surrendering a policy for its cash value or allowing it to lapse. By selling the policy, the policyholder can receive a lump sum that is greater than the surrender value but less than the death benefit.

Inflation and Its Effects on Retirement

Inflation erodes purchasing power over time, meaning that the same amount of money buys less as prices rise. For retirees, who often rely on fixed incomes from pensions, Social Security, or retirement savings, inflation can pose a significant threat to financial stability.

As inflation increases, so do the costs of healthcare, housing, food, and other essential expenses. This can create a gap between income and necessary spending, forcing retirees to look for ways to supplement their income. Selling a life insurance policy through a life settlement becomes a viable option for many, particularly when they are facing unexpected financial challenges due to rising prices.

The Role of Inflation in Determining Life Settlement Value

The impact of inflation on life settlements is twofold. First, inflation can increase the attractiveness of life settlements as policyholders seek additional funds to cover rising expenses. Second, inflation can influence the secondary market value of life insurance policies themselves.

As inflation drives up the cost of living, more seniors may consider selling their life insurance policies to access the policy’s hidden value immediately. This increased demand can lead to more competitive offers from life settlement purchasers. In other words, the need for liquidity among seniors can create a more favorable market for selling policies.

However, inflation can also affect the buyers of life settlements. Investors who purchase life insurance policies through life settlements must consider the future value of the death benefit in the context of inflation. If inflation is expected to remain high, the future value of the death benefit may be worth less in real terms, making the policy less attractive to buyers. This could result in lower offers for certain life insurance policies.

Strategic Considerations for Policyholders

Given the impact of inflation on life settlements, it is crucial for policyholders to carefully evaluate their options before selling a policy. Here are some key considerations:

Current and Future Financial Needs: Consider your current financial situation and how inflation is affecting your budget. If you anticipate needing more cash to cover rising expenses, a life settlement may provide a solution. However, it’s essential to weigh this against the long-term benefit your life insurance policy could provide to your beneficiaries.

Policy Valuation: The value of your life insurance policy in a life settlement is influenced by factors such as your age, health, and the policy’s death benefit. Inflation can impact these factors, so it’s important to work with a reputable life settlement company who can offer an appraisal of your policy’s value in the current economic environment.

Tax Implications: Life settlements are generally subject to taxation, with different portions of the payout being taxed as ordinary income, capital gains, or not at all. Inflation can influence tax brackets and rates, so it’s wise to consult with your trusted tax advisor to understand how selling your policy could affect your tax situation.

Alternative Income Sources: Before deciding on a life settlement, consider other ways to supplement your income. For example, you may have investments, assets, or other retirement savings that could be leveraged without selling your life insurance policy. Comparing the potential returns and risks of different options is crucial in an inflationary environment.

The Future Outlook for Life Settlements in an Inflationary Economy

As inflation continues to be a concern for retirees, the demand for life settlements is likely to grow. This could lead to a more competitive market, potentially benefiting policyholders looking to sell their policies. The future outlook will also depend on broader economic conditions, including interest rates, market stability, and the overall performance of the life insurance industry.

For investors, life settlements may remain an attractive asset class, offering diversification and the potential for returns that are not directly tied to traditional financial markets. However, they will need to factor in inflation when evaluating potential returns, which could impact the prices they are willing to pay for life insurance policies.

For policyholders, the key takeaway is that inflation adds another layer of complexity to the decision to sell a life insurance policy. While life settlements can provide much needed liquidity, especially in a high-inflation environment, it’s essential to approach the decision with careful consideration of all factors involved.

The impact of inflation on life settlements is an important consideration for anyone thinking about selling their life insurance policy. As inflation continues to affect the cost of living, life settlements may become an increasingly attractive option for retirees seeking to supplement their income. Policy owners should carefully evaluate their financial situation, the value of their policy, and the potential implications of selling before making a decision. By understanding how inflation influences the life settlement market, seniors can make more informed choices that align with their long-term financial goals.

To find out if you are likely to qualify for a life settlement or any other Reverse Life Insurance solution, such as a viatical settlement or term life settlement, please give us a call at 800-727-7654.

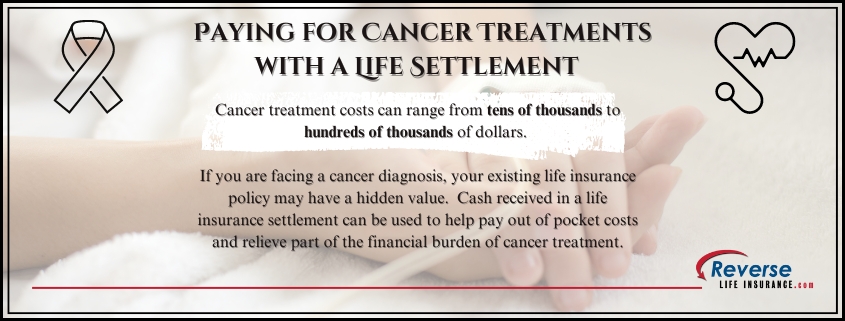

Cancer diagnosis and treatment can be an overwhelming experience, not only emotionally but also financially. The cost of cancer treatments has been steadily rising, often creating a significant burden for patients and their families. However, there are financial options available to help ease this burden. One such option is paying for cancer treatments with a life settlement. This is a financial strategy that can provide substantial funds to help cover the cost of cancer treatments and other expenses.

Understanding Life Settlements

A life settlement involves selling an existing life insurance policy to a third-party investor for a lump sum payment. This amount is typically more than the policy’s cash surrender value but less than its death benefit. Unlike viatical settlements, which are specifically for those with terminal illnesses and a life expectancy of two years or less, life settlements can be an option for individuals with longer life expectancies. This makes life settlements a viable choice for cancer patients who may not be terminally ill but still need financial support for their treatment and care. The impact of health changes on life insurance policy value is substantial, so it is always wise to make sure medical records are up to date.

Popular Cancer Treatments and Their Costs

Cancer treatments vary depending on the type and stage of cancer. Some of the most common cancers include breast cancer, lung cancer, colorectal cancer, and prostate cancer. Treatments often involve a combination of surgery, chemotherapy, radiation therapy, targeted therapy, and immunotherapy.

Breast Cancer

Treatments may include surgery (lumpectomy or mastectomy), chemotherapy, radiation therapy, and hormone therapy. Common medications include Tamoxifen and Herceptin. The cost of treating breast cancer can range from $20,000 to $100,000, depending on the stage and treatment plan.

Lung Cancer

Treatment options include surgery, chemotherapy, radiation therapy, and targeted therapies such as Tarceva and Keytruda. The average cost of lung cancer treatment can exceed $150,000.

Colorectal Cancer

Treatments include surgery, chemotherapy, and targeted therapies like Avastin and Erbitux. The cost can range from $30,000 to $120,000, depending on the stage and type of treatment.

Prostate Cancer

Common treatments are surgery, radiation therapy, hormone therapy, and chemotherapy. Medications like Lupron and Zytiga are often used. The cost of prostate cancer treatment can range from $10,000 to $50,000 or more.

Financial Impact and Statistics

The financial burden of cancer treatment is significant. According to a study published in the Journal of the National Cancer Institute, the annual cost of cancer treatment in the United States is expected to reach nearly $246 billion by 2030. The out-of-pocket expenses for patients can be staggering, with some spending tens of thousands of dollars annually even with insurance coverage.

A life settlement can provide a crucial financial resource, allowing patients to focus on their health and well-being rather than worrying about the cost of treatment. For instance, a policyholder might sell a life insurance policy with a death benefit of $500,000 for $200,000 in a life settlement. This lump sum can be used to cover medical bills, daily living expenses, or any other needs.

How to Qualify for a Life Settlement

To qualify for a life settlement, policyholders typically need to be 65 years or older, although younger individuals with serious health conditions may also qualify. The policy itself should usually have a death benefit of at least $100,000. The policyholder must no longer need or can no longer afford the policy, and the premiums should not be too high compared to the policy’s face value.

Cancer treatment can be financially overwhelming, but a life settlement offers a way to access funds that can help cover these expenses. Paying for cancer treatments with a life settlement is a valuable option for those who have a longer life expectancy and do not qualify for a viatical settlement. By converting a life insurance policy into cash, cancer patients can alleviate some of the financial burdens and focus on their health and recovery.

If you or a loved one is considering a life settlement, it’s essential to have your policy appraised and learn about your options. This will allow you to make the best decision for your situation. Please give us a call at 800-727-7654 to explore the possibilities of life settlements in managing the cost of cancer care.

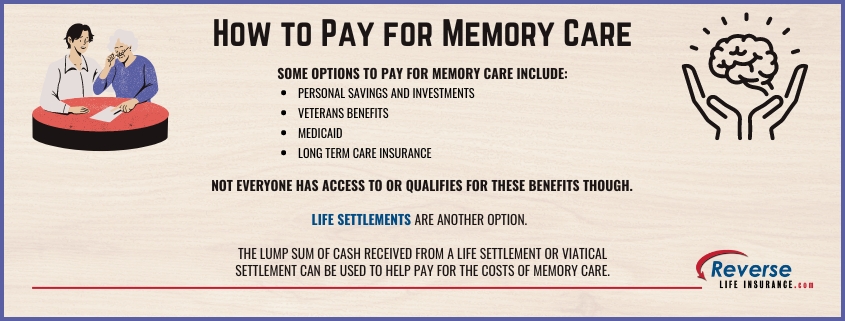

Facing the costs of memory care for a loved one with Dementia or Alzheimer’s can be overwhelming. “How to pay for memory care” is a common concern, especially as these expenses can quickly accumulate. One effective and often underutilized method to cover these costs is through life settlement options, selling a life insurance policy. This approach can provide immediate financial relief and help families afford the necessary care.

Current Costs of Memory Care

The cost of memory care varies significantly based on location, facility type, and the level of care required. As of 2024, the national median cost for memory care is approximately $5,430 per month. However, costs can range from $3,000 to over $10,000 per month, depending on the region. For example, the District of Columbia has the highest median cost at $11,490 per month, followed by Vermont at $8,400 and Hawaii at $8,100

Life Settlements: A Viable Funding Option

For those looking to cover the costs of memory care, a life settlement can provide a valuable financial option. In this process, you sell your life insurance policy to a life settlement company that purchases these policies. The buyer pays you a lump sum, which is always more than the cash surrender value, but less than the death benefit. This money can then be used to cover expenses like memory care.

This approach can be particularly helpful for individuals who no longer need their life insurance policy or can no longer afford the premiums. By converting the policy into immediate cash, families can better manage the high costs associated with specialized care. This can be a crucial source of funding for memory care, offering several advantages:

Immediate Access to Funds

Selling your policy provides quick liquidity, crucial for covering immediate memory care costs.

Maximized Value

The payout from a life settlement is generally higher than surrendering the policy back to the insurance company.

Flexibility in Use

The funds obtained can be used for any purpose, including medical expenses, memory care, or other living costs.

Is Selling a Life Insurance Policy Right for You?

Deciding whether to sell your life insurance policy depends on several factors. If you are asking, “Should I sell my life insurance policy?” consider the following:

Age and Health

Policyholders who are 65 or older, or those with significant health impairments, are more likely to qualify. If an insured is in need of memory care, they are likely to be eligible.

Policy Type and Value

Universal, whole, and convertible term life insurance policies are the most commonly sold types. Policies with a face value of $100,000 or more are often required.

Financial Needs

Assess your immediate and long-term financial needs. Selling your policy can provide necessary funds but means forfeiting the death benefit.

Other Funding Options

In addition to life settlements or a viatical settlement, families can explore other funding methods for how to pay for memory care:

Personal Savings and Investments

Using personal savings, retirement accounts, or investments can help cover costs.

Veterans Benefits

Eligible veterans and their spouses may qualify for Veterans Aid and Attendance benefits.

Medicaid

For those who qualify, Medicaid can cover memory care expenses, typically in a shared room.

Long-Term Care Insurance

If you have a policy, it may cover memory care costs, depending on the policy terms.

While these are viable options for many, not everyone has access to them. Many people do have existing life insurance policies that could be used while they are still living to help to pay for vital care.

To find out if you are likely to qualify, please give us a call at 800-727-7654. It usually only takes a 5-minute phone call to find out if you’re eligible to receive a lump sum cash offer for the hidden value in your existing life insurance policy.

Most calls we have fielded from CPAs and Accountants over the past 15 years have been around cost basis. Accountants -many for the first time- were trying to calculate the cost basis of a life insurance policy. There was a next to impossible computation to interpolate the cost basis, which relied on cost of insurance information from the insurance company and many insurance companies wouldn’t disclose the information and some didn’t even track it. It became much easier to determine life insurance cost basis in 2017 with the passage of the Tax Cuts and Jobs Act.

Accountants, CPAs Discovering Hidden Value in Life Insurance

Today things are very different, most of the calls we get from Accountants are around assisting or facilitating the sale of their client’s life insurance policy. Many of the CPAs and Accountants are navigating a life settlement for the first time, because their client’s insurance agent or advisor is restrained from mentioning a life settlement, even though it is in their shared client’s best interest.

The Reverse Life Insurance platform digitally and compliantly garners all of your clients insurance information directly from the carrier and gathers all the appropriate medical information inside of HIPPA guidelines. Once the information is mustered, third party Life Expectancy estimates are obtained by licensed buyers utilizing our platform. There is no cost and no obligation to the seller. Accountants and CPAs discovering hidden value in life insurance can help their clients without taking an active part in the process.

Life Settlement Taxation

The Tax Cuts and Jobs Act of 2017 (TCJA) made a big impact on the taxation of life settlements. The law has two provisions favorable to life settlements. One makes the tax treatment to the seller more favorable by changing the treatment of proceeds from a settlement. The other provision is an increase in the estate tax exclusion amount, diminishing the need for a large policy to cover estate taxes.

Prior to the Tax Cuts and Jobs Act of 2017

Currently, the tax treatment of life settlement proceeds is the same as the treatment of funds received from surrendering your policy. Prior to TCJA, the tax treatment of funds received after policy surrender was more favorable than the tax treatment of funds received in a life settlement.

When surrendering a policy, the proceeds were taxed on the amount received minus the total cumulative investment (premiums paid in minus withdrawals and dividends.)

When selling a policy as a life insurance settlement, the basis was reduced by the cumulative cost of insurance (COI) charges. You could not deduct the full premiums paid into the policy and it was usually difficult to obtain a correct COI charge or any explanation for those charges from your insurance company. Now, the premiums paid are the cost basis, regardless of the amount utilized towards the cost of insurance. This is huge, and brings Term Life Insurance policies into play.

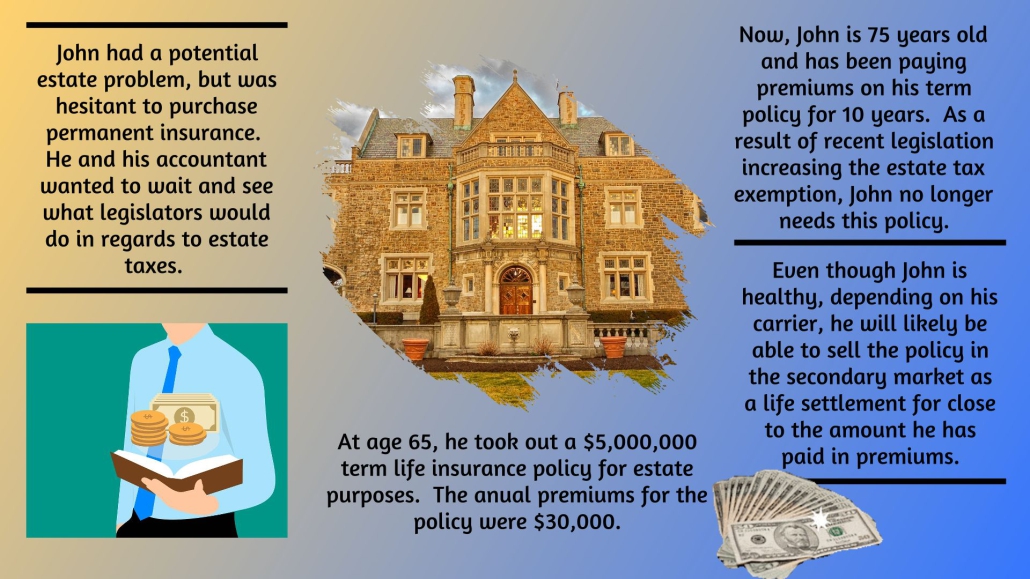

Prior to TCJA, the estate tax exemption was $5.49 million for a single taxpayer and $11.2 million for a couple filing jointly. There were many Estate Tax policies sold that have not only underperformed, but they often are no longer necessary. Universal Life and Flexible Premium Life policies with no cash value often have a hidden value as a life settlement. Many people hedged their insurance by purchasing large term insurance policies as the Federal Government discussed the potential estate tax threshold. If the term life insurance policies are convertible, which they typically are, there may very well be a hidden value, dependent upon the insured’s age, current health and policy specifics.

After the Tax Cuts and Jobs Act of 2017

As a result of TCJA, taxation of life settlements changed dramatically.

Tax Basis

Amounts received up to the tax basis are income tax free. Anything in excess of the tax basis (up to the surrender value) is taxed at ordinary income rates. Amounts received in excess of the cash value get favorable capital gains treatment. This applies to both funds received in a life settlement and those received after surrendering a policy.

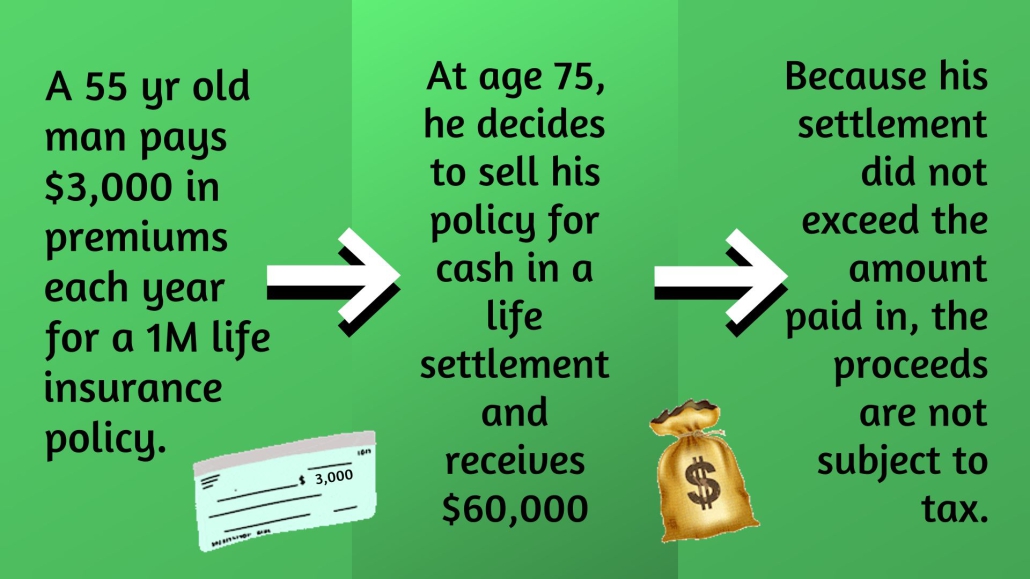

Whatever your client paid into the life insurance policy minus anything taken out in the form of dividends, cash, or loans is now the tax basis. Money taken out of the policy or any proceeds from a life settlement up to this tax basis should incur no income taxes. For example, if a client paid premiums for 20 years at $3000 per year, the tax basis would be $60,000 regardless of the type of life insurance policy. Any amount received over the tax basis up to the surrender value of their policy will be taxed as ordinary income. Anything in excess of the surrender value is still considered a capital gain.

Estate Tax Exemptions Changes

The amount excludable from estate tax is now $11.2 million per person and $22.4 million per couple. People with large estates used to purchase policies for the sole purpose of paying for estate taxes. Now that the exemption amounts have been raised, many of these policies are no longer necessary. A life settlement is a great option to access the hidden value of an unneeded policy. Someone in this scenario could be able to stop paying premiums and receive cash money now.

Viatical Settlement Taxation

Viatical settlement proceeds are taxed differently than life settlement proceeds, but only if they meet specific requirements. The taxation of the proceeds was not affected by recent tax law changes.

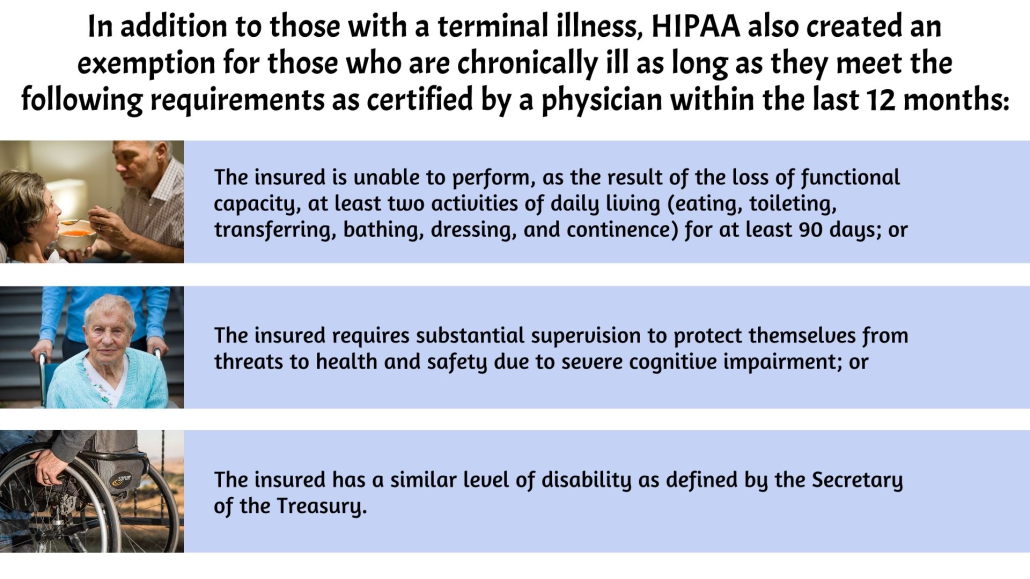

In 1996, the Health Insurance Portability and Accountability Act (HIPAA) was signed into law. This act specified that proceeds received either from a viatical settlement or as accelerated death benefits on a policy in which the insured was chronically or terminally ill would be tax free as long as the policy was purchased by a viatical settlement company who is licensed in the seller’s state. To qualify for this tax treatment, the insured must have less than two years to live. Although most states follow this federal law, some still impose taxes on viatical settlements. As a tax advisor, you need to be prepared to advise your clients of the laws affecting them.

The proceeds from a viatical settlement in which the insured is considered chronically ill are taxed differently. In order for money received by a chronically ill person to be tax free, the proceeds must be used for the costs of long-term care services that are not covered by insurance. Otherwise, benefits not used for long-term care received in excess of an annually-adjusted limit are subject to taxation.

Considering the recent tax law changes, a life settlement may be a better option now than ever before.

Funds received as a result of a life settlement no longer receive unfavorable tax treatment when compared to those received after a policy surrender.

Viatical settlement taxation has remained unchanged and funds received in this type of settlement are in most cases tax-free.

The estate tax exemption has been doubled, so many policies taken out for the sole purpose of paying taxes are no longer needed. These policies can be sold for cash now, eliminating premium payments.

Why Don’t More CPAs and Financial Advisors Mention Life Settlements?

Many accountants and financial advisors often wrongly assume that their client’s insurance agent or advisor has educated them about life settlements and has already helped them to have their policy appraised. Most seniors purchased their policy years ago and are no longer in contact with their original insurance agent. Insurance companies certainly don’t reach out to clients to make them aware of any potential value in a life settlement or discuss how a policy is performing. If no one else is assisting your clients in understanding the value of one of their biggest assets, the duty may fall to you. Accountants and CPAs can help clients with discovering the hidden value in their life insurance policies by telling them about life settlements.

Most Accountants, when asked, simply do not feel qualified to discuss life settlements, have a bad taste in their mouth from something they have heard or just don’t feel that it is their responsibility. Any advisor knowledgeable about life settlements and other reverse life insurance options is more prepared to help their clients discover the hidden value in their life insurance policy, but you don’t have to be an expert to simply tell your client to have a life insurance policy appraised prior to any surrender or lapse.

Life settlements are legal and heavily regulated in most states. Only 5 states, Alabama, Missouri, South Carolina, South Dakota, and Wyoming are without life settlement regulation.

Several states actually have laws in place to protect consumers. In those jurisdictions with disclosure laws, insurance companies must make consumers aware of the possibility of a life settlement as an alternative to a policy lapse or surrender. Agents and advisors have already been sued for neglecting to educate their clients.

Appraisals Necessary for Discovering the True Hidden Value in Life Insurance

If you are selling real estate, a business, or any other valuable asset, you would hopefully have the item evaluated by a qualified appraiser if you could. A life insurance policy is no different. A life insurance policy is an asset and unfortunately, all too often, we hear of someone surrendering a policy and unwittingly throwing away hundreds of thousands of dollars. The fact is, their life insurance policy may be the most or one of the most valuable of your client’s assets, and they are often completely unaware.

Term insurance and policies with zero cash value often qualify as a life settlement. Your client’s life insurance policy may have an exponentially higher hidden value than the obvious cash surrender value offered by the insurance company.

How to Talk to a Client About Life Settlements

When considering a surrender or lapse of an unneeded or too expensive life insurance policy, your client may not even think to ask for your input. If life insurance is not something you discuss regularly, consider adding it to your client checklist. An accountant or advisor can help prevent clients from lapsing or surrendering policies before exploring all of their options.

Your clients may see advertisements about life settlements on television or social media. You should tell them to always get more than one offer, and if they can get a direct offer from a licensed Reverse Life Insurance buyer and save the 30% or more commissions most brokers charge, they will thank you and so will we.

Referrals

Anyone can make a referral to Reverse Life Insurance for a possible life settlement. You do not have to have an insurance license or any licensing for that matter. Should your client qualify and accept and receive their cash offer, you or your designate is eligible for a referral fee in all but a few states. This fee is paid by the licensed buyer above and beyond the sales proceeds your client receives.

With the current and more favorable treatment of life settlement proceeds as well as the diminished need for estate tax policies, it is a great time for your clients to explore the hidden value in their policy before they cancel it. Accountants and CPAs discovering hidden value in life insurance can often make a big difference in the lives of their clients.

The impact of inflation on life settlements can affect the amount of hidden value your policy has.

The impact of inflation on life settlements can affect the amount of hidden value your policy has.

Do You Qualify?

Do You Qualify?