How to Access Enhanced Cash Value from Universal Life

If you’re wondering how to access enhanced cash value from universal life, you’re not alone. Many policyholders don’t realize that their universal life insurance policy might be worth more than its surrender value—especially if they explore their options in the secondary market. This blog post will break down what enhanced cash value means, how it differs from the traditional surrender value, and what steps you can take to access more value from your policy.

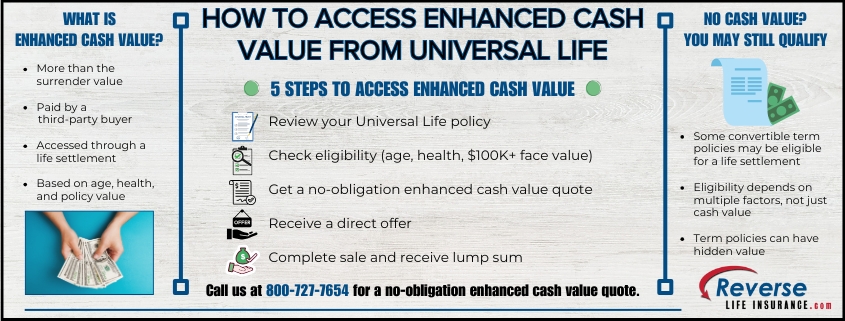

What Is Enhanced Cash Value?

Enhanced cash value refers to the potential of receiving more money from your universal life insurance policy than what your insurance company would pay if you surrendered the policy. This often occurs through a life settlement, where you sell your policy to a third-party buyer for an amount higher than the surrender value but less than the death benefit.

Why Your Surrender Value Isn’t the Whole Story

When you surrender your universal life insurance policy, your insurer typically offers the cash surrender value—a figure based on the policy’s accumulated cash value minus any fees and outstanding loans. For many seniors or individuals with changing financial priorities, this can be a disappointing amount.

However, in the secondary market, life settlement buyers assess your policy differently. They consider your age, health status, premium costs, and policy size to determine how much they’re willing to pay. Often, the amount they offer significantly exceeds the surrender value—this is what we refer to as enhanced cash value.

How to Access Enhanced Cash Value from Your Policy

To explore your policy’s enhanced cash value potential, follow these steps:

- Review Your Policy Details

Gather your policy specifics, including the face amount, premium history, and current cash surrender value. Confirm the policy type. While Universal Life policies most often qualify for enhanced cash value, other types may also be eligible. - Evaluate Your Eligibility

Life settlement buyers typically look for insureds who are age 65 or older or who have a serious health condition. The policy should also have a death benefit of $100,000 or more in most cases. - Request a Policy Appraisal

You can request a no-obligation policy appraisal to find out what your policy might be worth on the secondary market. This enhanced cash value quote will give you a better idea of the potential amount available to you. - Receive a Direct Offer

If your policy qualifies and there is interest, you’ll receive a direct offer from a buyer who would like to purchase it. This offer may be substantially higher than the surrender value, providing you with immediate funds you can use for any purpose. When you receive a direct offer through our platform, you always receive the full amount presented to you without the need to subtract a broker fee. - Complete the Sale

Once you accept an offer and sign contracts, ownership and beneficiary rights transfer to the buyer. They take over responsibility for paying the premiums and you receive a lump-sum cash payment. The entire process typically takes a few weeks to complete.

What If My Policy Has No Cash Value?

Even if your policy doesn’t have any cash value, you may still be able to sell it. For example, convertible term life insurance policies may qualify for a term life insurance settlement if they can be converted to permanent coverage. These policies often have hidden value that’s overlooked by policyholders who assume only cash value policies can be sold. If you’re not sure whether your policy qualifies, it’s worth checking—especially if you’re facing high premiums or no longer need the coverage.

When Is It a Good Idea?

Accessing enhanced cash value from your universal life policy might be a good move if:

- You no longer need the coverage

- You’re struggling to afford the premiums

- You want to supplement your retirement income

- You need funds for medical expenses, long-term care, or debt relief

Before you surrender your policy for a fraction of its worth, take the time to understand how to access enhanced cash value from universal life. In many cases, your policy may have significant hidden value that can be unlocked through a life settlement. Even if your policy doesn’t build cash value, like a convertible term policy, you might still qualify—especially if it’s convertible to the right type of policy. We help policyholders discover these opportunities and guide them through the process. If you would like to learn if you qualify, please give us a call at 800-727-7654

Learn the benefits of life settlements vs surrender value and which option is best for you.

Learn the benefits of life settlements vs surrender value and which option is best for you. Do You Qualify?

Do You Qualify?