Selling Life Insurance After Gastric Cancer Diagnosis

A gastric cancer diagnosis can be overwhelming, not only emotionally but also financially. The cost of treatment, medications, travel for specialized care, and day-to-day living expenses can place a heavy burden on patients and their families. Selling life insurance after gastric cancer diagnosis is one option that many people do not realize is available. By selling your existing policy, you can unlock its value and gain immediate funds that can help cover the high costs of care or provide financial stability during a difficult time.

Understanding Gastric Cancer Costs

Gastric cancer, also known as stomach cancer, often requires a combination of treatments such as surgery, chemotherapy, targeted therapy, and radiation. These treatments can span several months or longer and often come with significant out-of-pocket expenses. Even patients with comprehensive health insurance may face high deductibles, co-pays, or costs for medications and supportive therapies that are not fully covered.

In addition to direct medical expenses, many patients and families experience a loss of income due to time away from work. When these financial challenges are combined with the physical and emotional toll of cancer treatment, it is no surprise that many people begin looking for alternative financial resources.

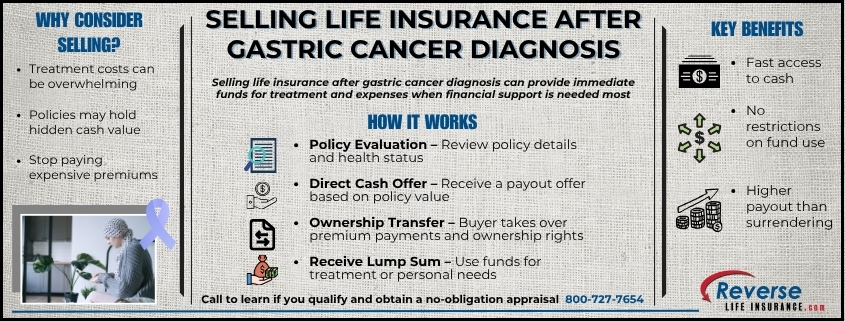

What Does It Mean to Sell a Life Insurance Policy?

Selling your life insurance policy, often called a life settlement or viatical settlement, involves transferring ownership of your policy to a third-party buyer. In return, you receive a lump sum cash payment. This payment is usually far greater than the cash surrender value offered by the insurance company and gives you immediate access to funds that can be used for any purpose.

Once the sale is complete, the buyer becomes responsible for future premium payments and collects the policy’s death benefit when the insured passes away. For many people facing a serious diagnosis, this trade-off is worth it because the funds can provide relief and flexibility now, when it is most needed.

Why Gastric Cancer Patients Often Qualify

Health conditions significantly influence the value of a life insurance policy in the secondary market. Buyers are typically willing to pay more for policies where the insured has a serious or advanced medical condition, such as gastric cancer. This is because the buyer assumes the financial risk of continuing premium payments and the timeframe for policy maturity is likely to be shorter.

Policies that typically qualify include:

- Whole life insurance policies

- Universal life policies

- Convertible term life policies

If your policy has a face value of at least $100,000, you may be eligible to sell it. The combination of an advanced illness and a larger policy value usually results in stronger offers from buyers.

How the Life Settlement Process Works

The process of selling life insurance after a gastric cancer diagnosis is generally straightforward:

- Policy Review and Initial Assessment

A direct buyer reviews your policy details and medical history to determine whether your policy is eligible. - Offer Stage

Based on the policy type, premium costs, and your health status, the buyer may make a cash offer. - Acceptance and Transfer

If you decide to accept the offer, you sign a contract the necessary documents to transfer ownership of the policy. From this point forward, you no longer have to pay premiums. - Lump Sum Payment

Once the transfer is complete, you receive a lump sum cash payment. These funds can be used for any purpose, from covering medical bills to paying off debt or even creating memorable experiences with loved ones.

The process is confidential, and there is never an obligation to accept an offer, which allows you to explore your options without risk.

Advantages of Selling Your Policy

There are several benefits to selling a life insurance policy when faced with a serious illness like gastric cancer:

- Immediate Funds: Provides quick access to money for treatment, medication, or everyday expenses.

- No More Premiums: Eliminates the financial burden of paying ongoing premiums.

- Higher Payout: Often results in more cash than surrendering the policy back to the insurance company.

- Flexible Use: Funds are not restricted and can be used however you choose.

Factors That Affect the Offer

Several elements determine how much a buyer is willing to pay for your policy, including:

- The face amount of the policy

- Your age and health condition

- The type of policy you have

- The ongoing cost of premiums

- Market conditions within the life settlement industry

Is Selling Your Life Insurance the Right Choice?

This decision depends on your financial needs, your family’s situation, and whether the death benefit is still essential for your beneficiaries. Some policyholders choose to sell only when premiums become unaffordable, while others view the cash payout as a more practical way to use the policy’s value during their lifetime.

Selling life insurance after gastric cancer diagnosis is an option that can provide immediate financial relief and peace of mind. It allows you to convert a non-liquid asset into cash at a time when financial flexibility is critical. If you are facing mounting medical costs or simply want to access the value of your policy now, exploring a life settlement could be a smart financial decision. Please give us a call at 800-727-7654 to learn if you qualify.

Do You Qualify?

Do You Qualify?