If you’re asking yourself How do I get my life insurance policy appraised?, you’re starting at the right point. Never sell your life insurance policy without first getting it appraised yourself. Many policyholders reach a point where they want to understand the true value of their life insurance – not just the surrender value, but what it could actually be worth in the secondary market. Whether you’re facing rising premium costs, unexpected medical expenses, or simply reevaluating your financial plans, a life insurance appraisal can help you make an informed decision.

What Is a Life Insurance Policy Appraisal?

A life insurance appraisal estimates what your policy could sell for in a life settlement, a legal, regulated transaction where you sell your life insurance to a third-party buyer for a lump sum cash payment. Unlike cash value or surrender value, an appraisal reflects the fair market value, which can be significantly higher depending on your situation.

When Should You Consider an Appraisal?

There are several situations where an appraisal makes sense:

- Your policy premiums are becoming unaffordable

- You no longer need the coverage (e.g., your children are financially independent)

- You’re planning for retirement, long-term care, or assisted living

- You’re considering lapsing or surrendering your policy and want to explore alternatives

Even policies with no cash value, such as term life insurance, may be eligible — especially if you’re over age 65 or have a serious health condition.

What Factors Affect Your Policy’s Value?

Buyers consider several key factors when appraising a policy:

- Your age and health status: Older age or certain medical conditions can increase value

- Policy type: Universal and whole life are most commonly sold, but convertible term policies can qualify too

- Death benefit amount: Typically, policies valued at $100,000 or more are considered. Some lower face amount policies may qualify if someone has a serious medical condition.

- Premium costs: Lower premiums relative to the policy face value make policies more attractive to buyers

- Insurance carrier rating: Highly rated carriers are preferred by investors

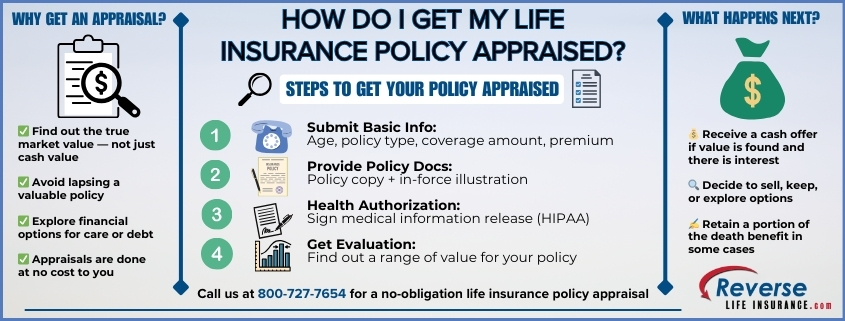

How to Get a Life Insurance Policy Appraised

Getting an appraisal is simpler than you might think. Here’s how it works:

- Submit basic information – This usually includes your age, policy type, face amount, and premium costs.

- Provide policy documents – A copy of the policy and an in-force illustration are often requested.

- Share health details – You will need to authorize release of medical records and in some cases complete a health questionnaire. No new medical exams are required.

- Wait for evaluation – Policy and health information will be reviewed in order to give you an idea of a potential range of value. If value is found and there is interest, a direct offer will be presented to you.

You’re under no obligation to sell just for requesting an appraisal.

What Happens After the Appraisal?

If your policy qualifies and there is interest from a buyer, you’ll receive a no-obligation offer. From there, you can decide whether to move forward, keep the policy, or explore other financial options. In some cases, you may even be able to retain a portion of the benefit while still receiving a cash payout.

Knowing how do I get my life insurance policy appraised gives you more control over your financial future. Rather than letting a policy lapse or accepting a low surrender value, you may be able to convert it into a lump sum of cash with no repayment required. If you’re unsure whether your policy qualifies, an appraisal is the first step toward unlocking its hidden value.

Learn if you qualify in a 5-10 minute phone call. 800-727-7654

Do You Qualify?

Do You Qualify?