When you sell your life insurance policy, the cash you receive can be a valuable financial resource, but it may also have tax consequences. Understanding how to estimate taxes on a life settlement payout helps you prepare for what you will actually keep after taxes, not just the gross offer amount. While every situation is unique and you should consult a qualified tax professional, there are general IRS guidelines that can help you anticipate how your proceeds may be taxed.

How Life Settlement Proceeds Are Taxed

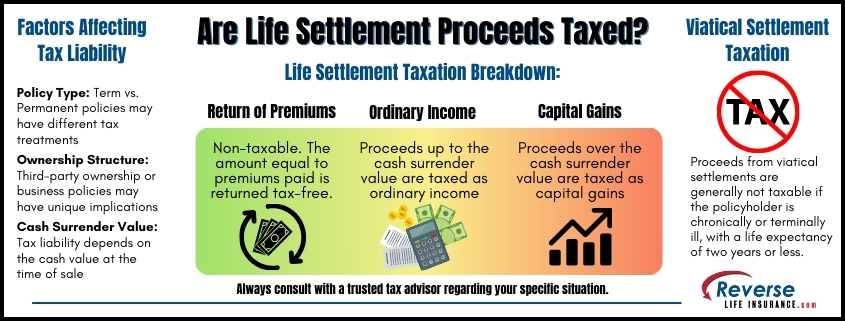

The IRS divides life settlement proceeds into three parts, each treated differently for tax purposes:

Tax-Free Return of Premiums Any amount you receive up to your cost basis, which is generally the total premiums you have paid into the policy, is not taxable. This is considered a return of your own money.

Ordinary Income The amount you receive above your cost basis but up to the cash surrender value of the policy is usually taxed as ordinary income. This is similar to how you would be taxed if you surrendered the policy back to the insurance company.

Capital Gains Any amount you receive above the cash surrender value is typically taxed as long-term capital gains.

Example:

Total premiums paid = $50,000 Cash surrender value = $80,000 Life settlement offer = $120,000

The first $50,000 (your cost basis) is tax-free.

The next $30,000 (the difference between $80,000 and $50,000) is taxed as ordinary income.

The final $40,000 (the difference between $120,000 and $80,000) is taxed as capital gains.

Estimating Your Cost Basis

Your cost basis is typically the total amount of premiums you have paid over the life of the policy. If you have owned the policy for many years, review past statements or contact your insurance carrier to get an accurate figure. For a term life insurance settlement on a policy that has been converted or renewed, determining the cost basis may involve reviewing both the original and converted policy history.

Factors That Can Affect Tax Calculations

Several variables can influence how much tax you owe after a life settlement:

Policy Type: Permanent policies, such as universal or whole life, often have a cash surrender value, which impacts how the payout is taxed. Term policies may not have cash value, so proceeds above your cost basis could be taxed differently.

Premium Financing or Loans: If the policy has an outstanding loan, it may reduce your cost basis and affect the taxable amount.

State Taxes: Some states may tax life settlement proceeds in addition to federal taxes.

Your Income Bracket: Ordinary income and capital gains rates depend on your overall income, which affects your final tax obligation.

Why Accurate Estimates Matter

Many sellers focus only on the gross offer amount without realizing how taxes will impact their net proceeds. Knowing how to estimate taxes in advance allows you to:

Avoid unpleasant surprises at tax time

Plan for medical care, assisted living, or other financial goals

Reporting Life Settlement Proceeds to the IRS

The IRS generally requires you to report the taxable portions of your settlement proceeds on your income tax return. In many cases, the buyer or provider may issue a Form 1099-LS, which reports the gross proceeds from the sale. It is best to provide this documentation to your accountant or tax preparer to ensure everything is filed correctly. If your transaction involves complex circumstances, such as a trust-owned policy or premium financing, professional tax guidance is strongly recommended.

Professional Guidance for Tax Planning

While IRS guidance provides a framework, life settlement taxation can become complicated depending on your situation. A tax professional can:

Accurately calculate your cost basis

Identify applicable state tax rules

Determine your exact ordinary income and capital gains exposure

Understanding the Net Payout

Knowing how to estimate taxes on a life settlement payout is essential for making informed financial decisions. By breaking your offer down into tax-free, ordinary income, and capital gains components, you can more accurately project what you will keep after taxes. Consult with a qualified tax advisor to ensure your calculations align with current IRS rules and your personal financial situation.

To learn if you qualify for a life settlement and obtain a no-obligation policy appraisal, please give us a call at 800-727-7654.

Selling your life insurance policy can be a valuable financial decision, especially when you no longer need coverage or could benefit from a lump sum payout to cover expenses like medical bills, debt relief, or retirement needs. However, the process can be complex, and many policyholders make costly mistakes that reduce their payout or create unnecessary complications. Understanding the most common mistakes to avoid when selling your life insurance policy can help you maximize your payout.

1. Not Fully Understanding Your Policy’s Value

One of the most significant mistakes policyholders make is underestimating their policy’s worth. Life insurance policies can hold substantial value, particularly if you’ve paid premiums for many years or have a permanent policy with a cash value component. Factors such as your age, health status, policy type (term, whole, or universal), and the death benefit can all influence your policy’s market value.

To avoid this mistake, it’s important to seek a life settlement appraisal before beginning the process.

2. Settling for a Low Offer Without Proper Evaluation

A common mistake is accepting an offer without understanding whether it’s truly competitive. Some life settlement brokers may offer less than your policy is worth, especially if you haven’t reviewed the key factors affecting your policy’s value.

It’s important to have a clear understanding of your policy’s worth before accepting an offer. A professional evaluation can help you feel confident you’re receiving a fair deal based on the market value and the specifics of your policy.

3. Overlooking Policy Loans and Liens

If you’ve borrowed against your life insurance policy or have any outstanding loans or liens, they will reduce the final payout you receive from a life settlement. This is because policy loans decrease the death benefit payout.

Before moving forward, verify whether your policy has any loans. Clear communication with potential buyers about these financial details is essential to avoid disappointment.

4. Ignoring Tax Implications

The proceeds from selling a life insurance policy can have tax consequences, yet many policyholders overlook this important detail. Depending on the amount you’ve paid in premiums and the size of the payout, a portion of a life settlement may be subject to federal income taxes. On the other hand, proceeds from viatical settlements typically are not subject to tax as they are considered an advance of your policy’s death benefit.

To avoid unexpected tax burdens, consult a qualified tax professional who can explain how are life settlement proceeds taxed. Understanding these details upfront can help you make more informed decisions about how to use the proceeds and avoid financial surprises.

5. Not Clarifying Your Policy’s Eligibility

Not all life insurance policies qualify for a life settlement, and assuming your policy is eligible can waste time and effort. For example, most term policies must be convertible to qualify for sale because term policy premiums can skyrocket after the initial term. On the other hand, permanent policies like whole life or universal life are more commonly sold.

Before starting the process, review your policy terms carefully. If you’re unsure, a life settlement professional can help determine whether your policy meets eligibility criteria.

6. Underestimating the Role of Health and Age Factors

Health and age play critical roles in determining your policy’s market value. Generally, policies from older individuals or those with declining health tend to receive higher offers because they represent lower risk for investors.

However, even if you’re in good health, your policy can still hold value. It’s essential to have realistic expectations and understand how these factors influence settlement offers.

7. Not Asking the Right Questions Before Accepting an Offer

Many policyholders fail to ask important questions before accepting a life settlement offer. Key details such as how long the process will take, what factors impact the payout, and whether there are any broker fees should be clearly explained upfront.

Clarify all terms with the settlement provider before signing any agreements. Being informed can help you feel more confident that you’re making the best decision for your situation.

8. Overlooking Alternative Financial Options

While life settlements can provide a valuable financial boost, they aren’t always the only—or best—solution for every policyholder. Some people sell their policies without fully exploring alternative options, such as:

Accelerated Death Benefits: If you have a qualifying medical condition, your insurer may offer a partial payout while you’re still alive. Not everyone will qualify for this option.

Policy Loans: Permanent policies may allow you to borrow against the cash value without selling the policy.

Reducing Coverage: Adjusting your coverage amount can lower premiums while retaining some benefits.

Selling Only a Portion of the Policy: In some cases, you may be able to retain part of the death benefit for your loved ones while selling a portion of your policy for cash.

Evaluating these alternatives can help you make a more informed decision before committing to a life settlement.

9. Attempting to Sell Without Professional Guidance

The life settlement market can be complex, and attempting to navigate it alone can lead to mistakes such as accepting low offers or missing important details. Working with a professional life settlement company can ensure you understand your options and receive a fair offer.

Selling your life insurance policy can be a strategic financial move, but avoiding common mistakes is essential for maximizing your payout and ensuring a smooth transaction. By fully understanding your policy’s value, comparing offers, and consulting with professionals, you can make informed decisions that protect your financial interests.

Remember, educating yourself about the mistakes to avoid when selling your life insurance policy can make a significant difference in the outcome. Taking these proactive steps will help you unlock the full potential of your policy.

To find out if you’re likely to qualify for a life settlement, please give us a call at 800-727-7654.

If you’re considering selling your life insurance policy, one important question to address is: are life settlement proceeds taxed? The answer isn’t straightforward, as it depends on a number of factors, including your cost basis, the amount you receive, and whether the policy is classified as a term or permanent policy. In this post, we will break down how life settlements are taxed and help you understand what you might owe in taxes after cashing in your life insurance policy.

What is a Life Settlement?

A life settlement is a financial transaction where a policyholder sells their life insurance policy to a third party for a lump sum cash payment. Typically, the payment is higher than the surrender value offered by the insurance company but lower than the death benefit. Life settlements can be an attractive option for those who no longer need or want to keep paying premiums on their policy, are facing financial challenges, or are interested in monetizing their policy to improve their quality of life.

Taxation Basics for Life Settlements

The proceeds from a life settlement can be subject to taxes, but the specific tax treatment depends on a variety of factors. The Tax Cuts and Jobs Act (TCJA) of 2017 also impacted the taxation of life settlements, altering some of the rules around policy valuation and reporting requirements. It’s important to understand how these changes may affect the tax treatment of your life settlement. Let’s break down the general rules for life settlement taxation.

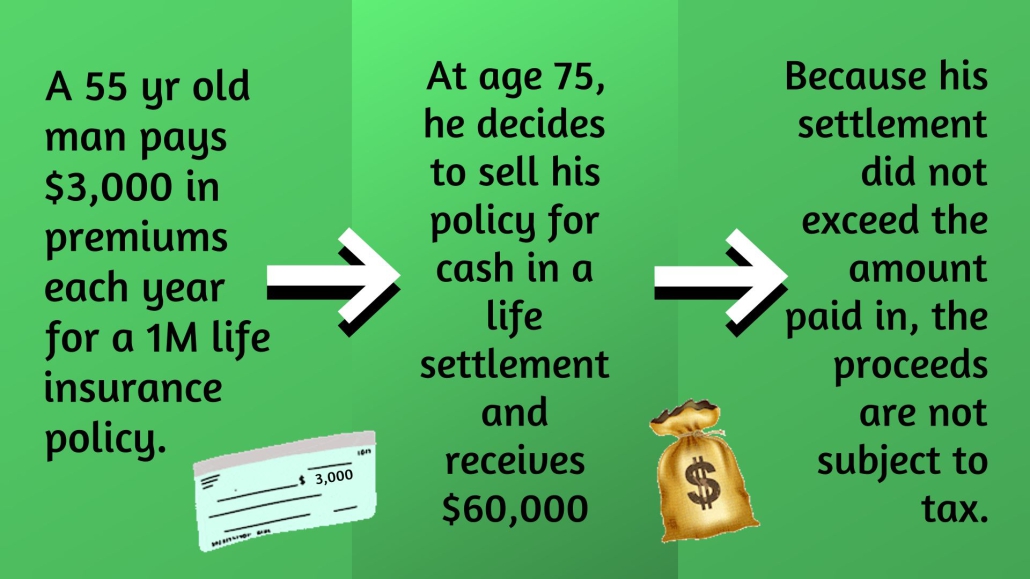

Return of Premiums

The first portion of the life settlement proceeds, up to the amount of premiums you’ve paid, is generally considered a return of your investment and is not subject to income tax. For example, if you have paid $50,000 in premiums over the life of the policy and receive $100,000 from the sale, the first $50,000 would be tax-free.

Taxation of Gains Above Cost Basis

Once you exceed the amount you have paid in premiums (your cost basis), the next portion is considered a gain. This gain is subject to income tax, but the classification of that tax depends on the nature of the gains.

Capital Gains Tax

If the proceeds you receive from the sale exceed the cost basis but do not exceed the policy’s cash surrender value, the difference is treated as ordinary income. Any amount above the cash surrender value may be considered a capital gain, which could qualify for lower tax rates.

In summary, life settlement proceeds are typically divided into three categories:

The return of premiums (not taxable)

Ordinary income (taxable up to the policy’s cash value)

Capital gains (taxable at capital gains rates for any amount above the cash value)

An Example of Life Settlement Taxation

To make this clearer, let’s look at an example. Suppose you have a life insurance policy for which you have paid $60,000 in premiums. The cash surrender value of the policy is $80,000, and you manage to sell it for $120,000 in a life settlement.

The first $60,000 you receive is not taxable because it represents the return of the premiums you paid.

The next $20,000 (which represents the difference between your cost basis and the cash surrender value) is taxable as ordinary income.

The remaining $40,000 (the amount over the cash surrender value) is taxable as a capital gain.

Factors that Affect Taxation

There are several factors that can affect how much tax you owe on your life settlement proceeds:

Policy Type

The type of life insurance policy (permanent vs. term) can influence the taxation. For instance, term policies may be eligible for different treatment since they often lack a cash surrender value.

Ownership and Beneficiaries

If the policy was part of a business, or if a third party paid the premiums, the tax implications might be different. Ownership structure plays a crucial role in determining taxable events.

Age and Health

Your age and health condition might also influence the settlement offer and taxation implications. Generally, older policyholders or those with health concerns might receive higher offers, impacting how much is taxable.

Are There Any Exemptions?

In certain circumstances, life settlement proceeds may be tax-exempt. For instance, if the policy qualifies as a viatical settlement—meaning it was sold by someone who is chronically or terminally ill—then the proceeds are often entirely exempt from taxation. Viatical settlements are treated differently because they are considered to be an advance of the death benefit and a source of financial support for individuals dealing with severe health challenges.

Consult a Tax Professional

It’s essential to consult with a trusted tax professional to make sure you understand the tax implications. The TCJA introduced new reporting requirements for insurance companies, which means you may need to provide additional documentation when filing your taxes. A tax advisor can help you navigate these complexities. Tax rules can be complicated, and missteps can be costly. A tax advisor can help you determine your cost basis, calculate potential taxes owed, and even explore strategies to minimize your tax liability. Since the IRS treats life settlements differently depending on each policyholder’s unique situation, professional advice can ensure you fully understand your obligations.

Other Financial Considerations

Beyond taxation, there are additional financial implications to consider before deciding on a life settlement:

Impact on Government Benefits: Receiving a lump sum from a life settlement could impact your eligibility for certain government benefits, like Medicaid. It’s important to understand how the extra income will affect your financial standing. A medical life settlement might be a valuable option if this is a concern for you.

Estate Planning: If your life insurance policy was part of your estate plan, selling it may impact the inheritance you leave behind. The death benefit that would have gone to your beneficiaries will be forfeited once the policy is sold.

So, are life settlement proceeds taxed? Yes, in most cases, life settlement proceeds are taxable, but how much you owe will depend on factors like your cost basis, the cash surrender value, and whether the policy qualifies as a viatical settlement.

Understanding the tax implications is important. If you’re considering a life settlement, it’s wise to understand the financial and tax consequences fully. Consult with a tax advisor and evaluate your options carefully to ensure that you make the best decision for your financial future.

To learn if you are likely to qualify for a life settlement, please give us a call today at 800-727-7654.

Most calls we have fielded from CPAs and Accountants over the past 15 years have been around cost basis. Accountants -many for the first time- were trying to calculate the cost basis of a life insurance policy. There was a next to impossible computation to interpolate the cost basis, which relied on cost of insurance information from the insurance company and many insurance companies wouldn’t disclose the information and some didn’t even track it. It became much easier to determine life insurance cost basis in 2017 with the passage of the Tax Cuts and Jobs Act.

Accountants, CPAs Discovering Hidden Value in Life Insurance

Today things are very different, most of the calls we get from Accountants are around assisting or facilitating the sale of their client’s life insurance policy. Many of the CPAs and Accountants are navigating a life settlement for the first time, because their client’s insurance agent or advisor is restrained from mentioning a life settlement, even though it is in their shared client’s best interest.

The Reverse Life Insurance platform digitally and compliantly garners all of your clients insurance information directly from the carrier and gathers all the appropriate medical information inside of HIPPA guidelines. Once the information is mustered, third party Life Expectancy estimates are obtained by licensed buyers utilizing our platform. There is no cost and no obligation to the seller. Accountants and CPAs discovering hidden value in life insurance can help their clients without taking an active part in the process.

Life Settlement Taxation

The Tax Cuts and Jobs Act of 2017 (TCJA) made a big impact on the taxation of life settlements. The law has two provisions favorable to life settlements. One makes the tax treatment to the seller more favorable by changing the treatment of proceeds from a settlement. The other provision is an increase in the estate tax exclusion amount, diminishing the need for a large policy to cover estate taxes.

Prior to the Tax Cuts and Jobs Act of 2017

Currently, the tax treatment of life settlement proceeds is the same as the treatment of funds received from surrendering your policy. Prior to TCJA, the tax treatment of funds received after policy surrender was more favorable than the tax treatment of funds received in a life settlement.

When surrendering a policy, the proceeds were taxed on the amount received minus the total cumulative investment (premiums paid in minus withdrawals and dividends.)

When selling a policy as a life insurance settlement, the basis was reduced by the cumulative cost of insurance (COI) charges. You could not deduct the full premiums paid into the policy and it was usually difficult to obtain a correct COI charge or any explanation for those charges from your insurance company. Now, the premiums paid are the cost basis, regardless of the amount utilized towards the cost of insurance. This is huge, and brings Term Life Insurance policies into play.

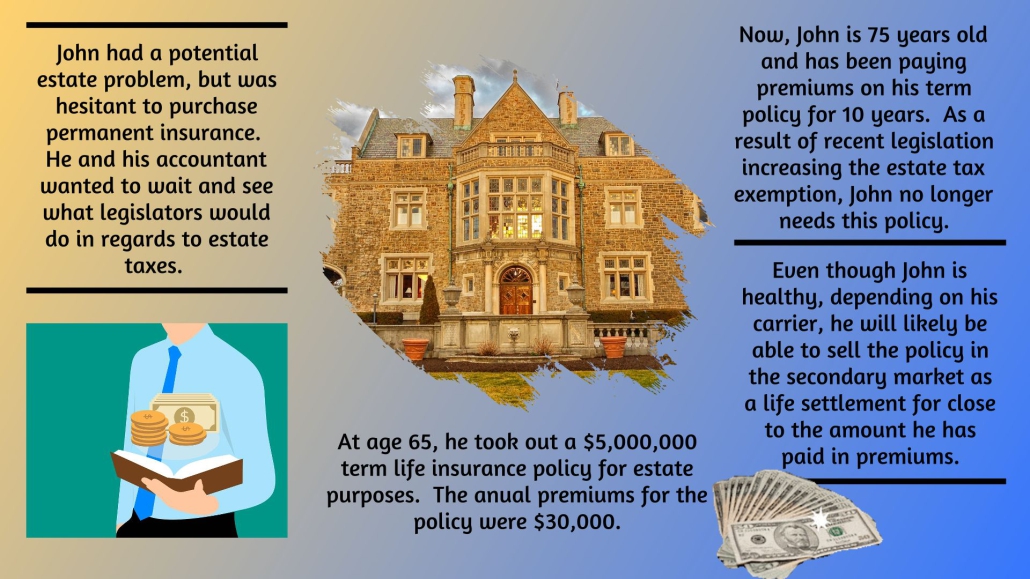

Prior to TCJA, the estate tax exemption was $5.49 million for a single taxpayer and $11.2 million for a couple filing jointly. There were many Estate Tax policies sold that have not only underperformed, but they often are no longer necessary. Universal Life and Flexible Premium Life policies with no cash value often have a hidden value as a life settlement. Many people hedged their insurance by purchasing large term insurance policies as the Federal Government discussed the potential estate tax threshold. If the term life insurance policies are convertible, which they typically are, there may very well be a hidden value, dependent upon the insured’s age, current health and policy specifics.

After the Tax Cuts and Jobs Act of 2017

As a result of TCJA, taxation of life settlements changed dramatically.

Tax Basis

Amounts received up to the tax basis are income tax free. Anything in excess of the tax basis (up to the surrender value) is taxed at ordinary income rates. Amounts received in excess of the cash value get favorable capital gains treatment. This applies to both funds received in a life settlement and those received after surrendering a policy.

Whatever your client paid into the life insurance policy minus anything taken out in the form of dividends, cash, or loans is now the tax basis. Money taken out of the policy or any proceeds from a life settlement up to this tax basis should incur no income taxes. For example, if a client paid premiums for 20 years at $3000 per year, the tax basis would be $60,000 regardless of the type of life insurance policy. Any amount received over the tax basis up to the surrender value of their policy will be taxed as ordinary income. Anything in excess of the surrender value is still considered a capital gain.

Estate Tax Exemptions Changes

The amount excludable from estate tax is now $11.2 million per person and $22.4 million per couple. People with large estates used to purchase policies for the sole purpose of paying for estate taxes. Now that the exemption amounts have been raised, many of these policies are no longer necessary. A life settlement is a great option to access the hidden value of an unneeded policy. Someone in this scenario could be able to stop paying premiums and receive cash money now.

Viatical Settlement Taxation

Viatical settlement proceeds are taxed differently than life settlement proceeds, but only if they meet specific requirements. The taxation of the proceeds was not affected by recent tax law changes.

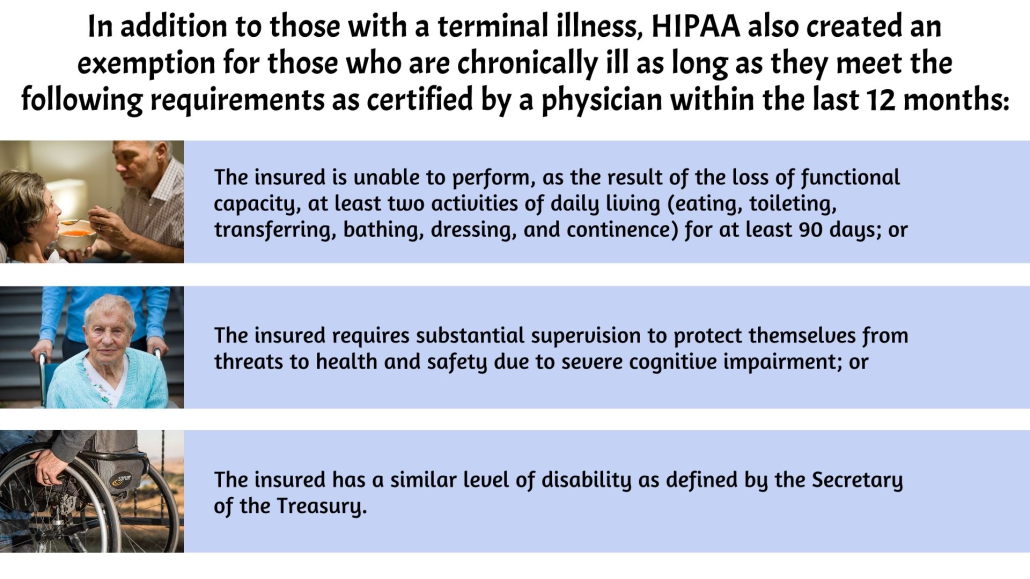

In 1996, the Health Insurance Portability and Accountability Act (HIPAA) was signed into law. This act specified that proceeds received either from a viatical settlement or as accelerated death benefits on a policy in which the insured was chronically or terminally ill would be tax free as long as the policy was purchased by a viatical settlement company who is licensed in the seller’s state. To qualify for this tax treatment, the insured must have less than two years to live. Although most states follow this federal law, some still impose taxes on viatical settlements. As a tax advisor, you need to be prepared to advise your clients of the laws affecting them.

The proceeds from a viatical settlement in which the insured is considered chronically ill are taxed differently. In order for money received by a chronically ill person to be tax free, the proceeds must be used for the costs of long-term care services that are not covered by insurance. Otherwise, benefits not used for long-term care received in excess of an annually-adjusted limit are subject to taxation.

Considering the recent tax law changes, a life settlement may be a better option now than ever before.

Funds received as a result of a life settlement no longer receive unfavorable tax treatment when compared to those received after a policy surrender.

Viatical settlement taxation has remained unchanged and funds received in this type of settlement are in most cases tax-free.

The estate tax exemption has been doubled, so many policies taken out for the sole purpose of paying taxes are no longer needed. These policies can be sold for cash now, eliminating premium payments.

Why Don’t More CPAs and Financial Advisors Mention Life Settlements?

Many accountants and financial advisors often wrongly assume that their client’s insurance agent or advisor has educated them about life settlements and has already helped them to have their policy appraised. Most seniors purchased their policy years ago and are no longer in contact with their original insurance agent. Insurance companies certainly don’t reach out to clients to make them aware of any potential value in a life settlement or discuss how a policy is performing. If no one else is assisting your clients in understanding the value of one of their biggest assets, the duty may fall to you. Accountants and CPAs can help clients with discovering the hidden value in their life insurance policies by telling them about life settlements.

Most Accountants, when asked, simply do not feel qualified to discuss life settlements, have a bad taste in their mouth from something they have heard or just don’t feel that it is their responsibility. Any advisor knowledgeable about life settlements and other reverse life insurance options is more prepared to help their clients discover the hidden value in their life insurance policy, but you don’t have to be an expert to simply tell your client to have a life insurance policy appraised prior to any surrender or lapse.

Life settlements are legal and heavily regulated in most states. Only 5 states, Alabama, Missouri, South Carolina, South Dakota, and Wyoming are without life settlement regulation.

Several states actually have laws in place to protect consumers. In those jurisdictions with disclosure laws, insurance companies must make consumers aware of the possibility of a life settlement as an alternative to a policy lapse or surrender. Agents and advisors have already been sued for neglecting to educate their clients.

Appraisals Necessary for Discovering the True Hidden Value in Life Insurance

If you are selling real estate, a business, or any other valuable asset, you would hopefully have the item evaluated by a qualified appraiser if you could. A life insurance policy is no different. A life insurance policy is an asset and unfortunately, all too often, we hear of someone surrendering a policy and unwittingly throwing away hundreds of thousands of dollars. The fact is, their life insurance policy may be the most or one of the most valuable of your client’s assets, and they are often completely unaware.

Term insurance and policies with zero cash value often qualify as a life settlement. Your client’s life insurance policy may have an exponentially higher hidden value than the obvious cash surrender value offered by the insurance company.

How to Talk to a Client About Life Settlements

When considering a surrender or lapse of an unneeded or too expensive life insurance policy, your client may not even think to ask for your input. If life insurance is not something you discuss regularly, consider adding it to your client checklist. An accountant or advisor can help prevent clients from lapsing or surrendering policies before exploring all of their options.

Your clients may see advertisements about life settlements on television or social media. You should tell them to always get more than one offer, and if they can get a direct offer from a licensed Reverse Life Insurance buyer and save the 30% or more commissions most brokers charge, they will thank you and so will we.

Referrals

Anyone can make a referral to Reverse Life Insurance for a possible life settlement. You do not have to have an insurance license or any licensing for that matter. Should your client qualify and accept and receive their cash offer, you or your designate is eligible for a referral fee in all but a few states. This fee is paid by the licensed buyer above and beyond the sales proceeds your client receives.

With the current and more favorable treatment of life settlement proceeds as well as the diminished need for estate tax policies, it is a great time for your clients to explore the hidden value in their policy before they cancel it. Accountants and CPAs discovering hidden value in life insurance can often make a big difference in the lives of their clients.

Do You Qualify?

Do You Qualify?