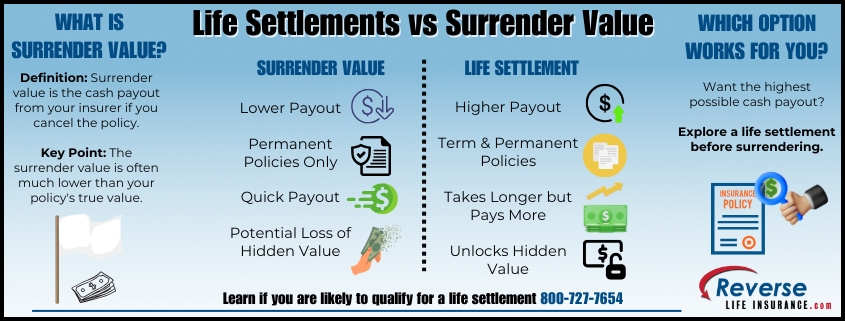

When faced with the decision to let go of a life insurance policy, many policyholders wonder: should I surrender my policy for its cash value or sell it through a life settlement? Both options offer a way to access cash, but life settlements vs surrender value differ significantly in terms of value, eligibility, and process. Understanding the key differences can help you make the most financially beneficial choice.

What Is Surrender Value?

The surrender value is the amount your insurance company pays you if you decide to cancel your policy. This option is typically available for permanent life insurance policies, such as whole life or universal life, which accumulate cash value over time. For term life insurance, which does not build cash value, surrendering the policy for cash is not an option.

Pros of Surrendering:

Simple Process: You work directly with your insurance company to cancel the policy.

Immediate Access: The surrender value is usually available quickly.

No Market Uncertainty: The value is predefined and does not depend on external buyers.

Cons of Surrendering:

Lower Payout: The surrender value is often significantly less than the policy’s potential worth in a life settlement.

Hidden Value Lost: Surrendering could mean throwing away enormous hidden value in your policy, as the payout is often only a fraction of what you could receive through a life settlement.

Fees May Apply: Surrender charges can reduce the cash value you receive.

What Is a Life Settlement?

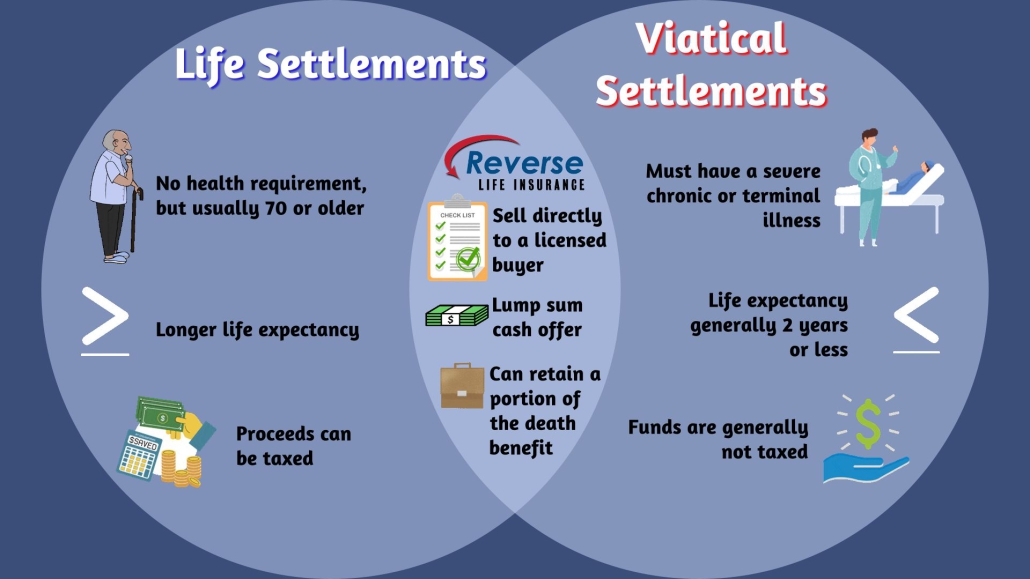

A life settlement involves selling your life insurance policy to a third party for a lump sum that is greater than the policy’s surrender value but less than its death benefit. The buyer assumes responsibility for future premiums and receives the death benefit when you pass away. Life settlements are an option for permanent and, in some cases, term life policies.

Pros of Life Settlements:

Higher Payout: A life settlement often yields significantly more than the policy’s surrender value.

Broad Eligibility: Policies with no cash value, such as convertible term policies, may still qualify for a settlement.

Relief from Premiums: Once sold, you no longer have to pay premiums.

Cons of Life Settlements:

Longer Process: A life settlement typically takes weeks to months to complete. However, our direct-to-consumer automated platform can speed up the process.

Health Assessment: Your health status can affect the offers you receive.

Tax Implications: Are life settlement proceeds taxed? Life settlement proceeds may be subject to taxes. Always consult with your trusted tax professional.

Comparing the Two Options

Feature

Surrender Value

Life Settlement

Payout Amount

Lower

Higher

Eligibility

Permanent policies only

Permanent and some term

Process Time

Fast

Moderate to long

Health Consideration

Not required

May impact offer amount

Premium Relief

Policy ends

Buyer assumes responsibility

Which Option Is Right for You?

Choosing between surrendering your policy or pursuing a life settlement depends on your financial goals and circumstances:

If you need quick cash and your policy has a low death benefit or minimal market appeal, surrendering might be the simplest route.

If you want to maximize your payout and avoid throwing away significant hidden value, a life settlement could be worth the additional time and effort, especially if your policy has a substantial death benefit or unique features like a waiver of premium rider.

While surrendering a life insurance policy offers convenience, it can often mean giving up significant hidden value. A life settlement generally provides a much higher financial return, especially for larger policies or those with strong market interest. If you’re considering letting go of your policy, exploring a life settlement prior to surrendering the policy is essential to ensure you make the most informed and beneficial decision.

Contact us today to learn if your policy qualifies for a life settlement and how much cash you could receive. 800-727-7654

Selling your life insurance policy can be a valuable financial decision, especially when you no longer need coverage or could benefit from a lump sum payout to cover expenses like medical bills, debt relief, or retirement needs. However, the process can be complex, and many policyholders make costly mistakes that reduce their payout or create unnecessary complications. Understanding the most common mistakes to avoid when selling your life insurance policy can help you maximize your payout.

1. Not Fully Understanding Your Policy’s Value

One of the most significant mistakes policyholders make is underestimating their policy’s worth. Life insurance policies can hold substantial value, particularly if you’ve paid premiums for many years or have a permanent policy with a cash value component. Factors such as your age, health status, policy type (term, whole, or universal), and the death benefit can all influence your policy’s market value.

To avoid this mistake, it’s important to seek a life settlement appraisal before beginning the process.

2. Settling for a Low Offer Without Proper Evaluation

A common mistake is accepting an offer without understanding whether it’s truly competitive. Some life settlement brokers may offer less than your policy is worth, especially if you haven’t reviewed the key factors affecting your policy’s value.

It’s important to have a clear understanding of your policy’s worth before accepting an offer. A professional evaluation can help you feel confident you’re receiving a fair deal based on the market value and the specifics of your policy.

3. Overlooking Policy Loans and Liens

If you’ve borrowed against your life insurance policy or have any outstanding loans or liens, they will reduce the final payout you receive from a life settlement. This is because policy loans decrease the death benefit payout.

Before moving forward, verify whether your policy has any loans. Clear communication with potential buyers about these financial details is essential to avoid disappointment.

4. Ignoring Tax Implications

The proceeds from selling a life insurance policy can have tax consequences, yet many policyholders overlook this important detail. Depending on the amount you’ve paid in premiums and the size of the payout, a portion of a life settlement may be subject to federal income taxes. On the other hand, proceeds from viatical settlements typically are not subject to tax as they are considered an advance of your policy’s death benefit.

To avoid unexpected tax burdens, consult a qualified tax professional who can explain how are life settlement proceeds taxed. Understanding these details upfront can help you make more informed decisions about how to use the proceeds and avoid financial surprises.

5. Not Clarifying Your Policy’s Eligibility

Not all life insurance policies qualify for a life settlement, and assuming your policy is eligible can waste time and effort. For example, most term policies must be convertible to qualify for sale because term policy premiums can skyrocket after the initial term. On the other hand, permanent policies like whole life or universal life are more commonly sold.

Before starting the process, review your policy terms carefully. If you’re unsure, a life settlement professional can help determine whether your policy meets eligibility criteria.

6. Underestimating the Role of Health and Age Factors

Health and age play critical roles in determining your policy’s market value. Generally, policies from older individuals or those with declining health tend to receive higher offers because they represent lower risk for investors.

However, even if you’re in good health, your policy can still hold value. It’s essential to have realistic expectations and understand how these factors influence settlement offers.

7. Not Asking the Right Questions Before Accepting an Offer

Many policyholders fail to ask important questions before accepting a life settlement offer. Key details such as how long the process will take, what factors impact the payout, and whether there are any broker fees should be clearly explained upfront.

Clarify all terms with the settlement provider before signing any agreements. Being informed can help you feel more confident that you’re making the best decision for your situation.

8. Overlooking Alternative Financial Options

While life settlements can provide a valuable financial boost, they aren’t always the only—or best—solution for every policyholder. Some people sell their policies without fully exploring alternative options, such as:

Accelerated Death Benefits: If you have a qualifying medical condition, your insurer may offer a partial payout while you’re still alive. Not everyone will qualify for this option.

Policy Loans: Permanent policies may allow you to borrow against the cash value without selling the policy.

Reducing Coverage: Adjusting your coverage amount can lower premiums while retaining some benefits.

Selling Only a Portion of the Policy: In some cases, you may be able to retain part of the death benefit for your loved ones while selling a portion of your policy for cash.

Evaluating these alternatives can help you make a more informed decision before committing to a life settlement.

9. Attempting to Sell Without Professional Guidance

The life settlement market can be complex, and attempting to navigate it alone can lead to mistakes such as accepting low offers or missing important details. Working with a professional life settlement company can ensure you understand your options and receive a fair offer.

Selling your life insurance policy can be a strategic financial move, but avoiding common mistakes is essential for maximizing your payout and ensuring a smooth transaction. By fully understanding your policy’s value, comparing offers, and consulting with professionals, you can make informed decisions that protect your financial interests.

Remember, educating yourself about the mistakes to avoid when selling your life insurance policy can make a significant difference in the outcome. Taking these proactive steps will help you unlock the full potential of your policy.

To find out if you’re likely to qualify for a life settlement, please give us a call at 800-727-7654.

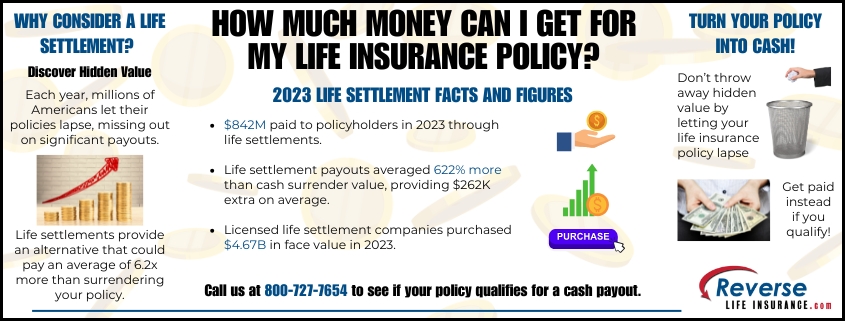

If you’ve ever asked yourself, “how much money can I get for my life insurance policy?”, you’re tapping into an increasingly popular financial solution. Selling a life insurance policy through a life settlement can be a game-changer, especially for seniors seeking to enhance their retirement income or reduce financial burdens. Recent market trends and data underscore just how beneficial this option can be.

Why Consider a Life Settlement?

Life settlements involve selling your life insurance policy to a third-party buyer for a one-time cash payment. The payment you receive is typically higher than the cash surrender value (CSV) but less than the death benefit. For many policyholders, particularly seniors, this option has proven to be a lucrative way to leverage an asset that might otherwise lapse or be surrendered for a minimal return.

The Growing Value of Life Settlements

Recent data from a 2023 market survey highlights the life settlement market’s potential:

Policyholders who sold their policies in 2023 received over $842 million collectively. This marked the third consecutive year of increased payouts, signaling the growth and stability of the market.

On average, life settlement payouts were 6.2 times greater than the CSV, a 622% increase. This translated to an average additional $262,000 in the pockets of American seniors who opted for life settlements rather than letting their policies lapse or surrendering them.

These figures demonstrate how life settlements have become a valuable financial strategy, offering policyholders much more than they would otherwise receive.

Factors That Determine How Much You Can Get

When considering a life settlement, it’s important to understand the factors that influence your policy’s value:

Your Age and Health: The older you are and the more serious your health condition, the higher the payout you are likely to receive. In 2023, this trend was evident as life settlement buyers continued to seek policies that promised quicker returns on investment.

Type of Policy: Permanent life insurance policies, such as universal life, tend to command higher cash offers than term policies. However, convertible term policies remain attractive. In some cases, non-convertible term policies can qualify if the insured has a terminal medical condition.

Death Benefit and Premiums: Policies with a higher face value generally receive higher offers. Additionally, policies with manageable premium payments are more appealing to buyers, impacting the cash offer you receive.

The Financial Impact: More Than Just Statistics

The real-life impact of life settlements is highlighted by the data. In 2023, life settlement transactions not only increased but also provided policyholders with $707 million more in payouts compared to what they would have received from surrendering their policies or allowing them to lapse. This is the largest amount ever recorded, showcasing how life settlements have become a crucial alternative for policyholders looking to maximize their financial returns.

While 3,218 transactions were completed in 2023, representing a 2-3% increase from previous years, this number still pales compared to the potential market. Over 9 million life insurance policies, with a collective value exceeding $725 billion, are surrendered or lapsed annually. This disparity underscores the significant opportunity many policyholders miss out on by not exploring life settlements. Don’t let the potential hidden value in your policy go to waste.

Maximizing Your Payout: What You Can Do

To ensure you receive the highest possible value for your life insurance policy, consider these tips:

Work with Experts: Engage with a trusted life settlement company. Their expertise can help navigate the process and secure competitive offers.

Utilize our Direct Platform: By getting a direct offer, there is no need to subtract a broker fee from the offer you receive.

Be Aware of Taxes: While the financial boost from a life settlement is significant, understanding the potential tax implications is important. Consulting your trusted tax advisor can help you navigate this aspect.

Is a Life Settlement Right for You?

So, how much money can you get for your life insurance policy? The answer is dependent on your unique situation, the type of policy you hold, and current market conditions. However, with average payouts reaching 622% more than cash surrender value and a total of $4.67 billion in face value policies purchased in 2023 alone, the potential returns are undeniable. By exploring the option of a life settlement, you could unlock substantial cash that can be used to support retirement, manage healthcare costs, or meet other financial needs.

With the life settlement market continuing to grow, now might be the ideal time to consider if this option is right for you. Give us a call at 800-727-7654 to find out if you’re likely to qualify and to learn more about how much your policy could be worth.

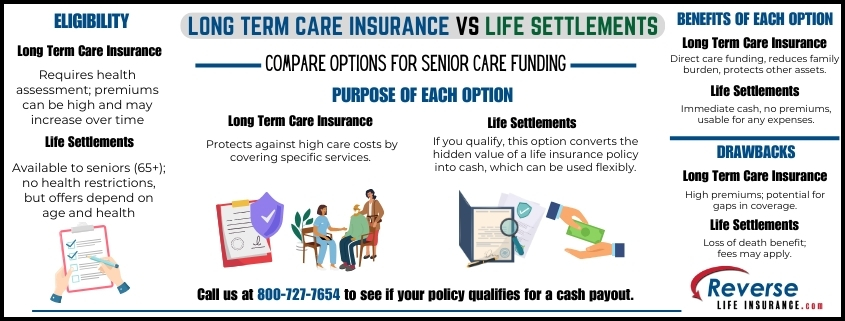

When it comes to long term care insurance vs life settlements, many people find themselves comparing these options when they or their loved ones need funds to cover aging-related expenses. Long-term care insurance is designed to support individuals with the costs of long-term healthcare, but not everyone has a policy when they need it most. In fact, many people don’t anticipate the rising costs of care until they’re already facing them. For those without a long-term care policy in place or who find the premiums unaffordable, a life settlement can be a viable alternative, providing access to cash that can help pay for these expenses.

Understanding Long Term Care Insurance

Long-term care insurance policies are specifically crafted to cover a range of services, such as in-home care, assisted living, nursing home care, and other support for daily living needs. Many individuals consider this type of insurance to avoid depleting their savings or relying solely on family members for support. However, qualifying for long-term care insurance is not always easy or affordable, particularly for older individuals or those with existing health conditions. Premiums for long-term care policies can also rise sharply over time, and many find it difficult to keep up with these increasing costs as they age.

In many cases, people reach retirement age without having secured a long-term care policy and then face the burden of high healthcare costs later. Additionally, even those who do have long-term care insurance may still encounter limitations on what their policy will cover, especially if they require specialized or extensive care.

What Is a Life Settlement?

A life settlement offers a way to access funds by selling an existing life insurance policy to a third-party buyer. Unlike a surrender value, which is generally a smaller payout, a life settlement allows the policyholder to receive a larger lump sum, which can often be used for any purpose—including healthcare or long-term care needs. This flexibility makes using life settlements to pay for long-term care an appealing choice for those facing unexpected healthcare expenses.

For individuals who do not have long-term care insurance, a life settlement can offer a financial solution that doesn’t require new qualifications or high ongoing premiums. Typically, life settlements are most accessible to seniors over 65 or those with health conditions that may shorten life expectancy, as these factors tend to yield higher offers. However, they can also be a suitable option for younger policyholders with significant healthcare needs.

Long Term Care Insurance vs Life Settlements: A Side-by-Side Comparison

Here’s a deeper look at the pros and cons of each option:

Long Term Care Insurance

Pros:

Coverage for Care Services: Designed specifically to cover costs associated with long-term care, such as nursing homes, assisted living, or home care, which can relieve family members of the financial burden.

Protected Assets: Allows individuals to receive care without needing to sell off other assets.

Cons:

High Premiums: Premiums for long-term care insurance can increase sharply, especially as individuals age, making it less affordable for those on a fixed income.

Health Requirements: To qualify, applicants often need to meet certain health criteria, which can exclude some individuals who already have significant healthcare needs.

Potential for Limited Coverage: Not all policies cover all types of care, leaving policyholders with gaps in their care options.

Life Settlements

Pros:

Immediate Cash Access: Life settlements provide a lump sum payment, giving individuals flexibility to cover any expenses they choose, including medical costs, home care, or assisted living.

Freedom from Premiums: Selling a life insurance policy eliminates the need to pay ongoing premiums, which can be a relief for individuals with fixed or limited income.

Cons:

Loss of Death Benefit: Once a life insurance policy is sold, beneficiaries no longer receive the policy’s death benefit. For some, this can be a significant drawback, especially if the policy was intended to support family members financially.

Possible Transaction Fees: Life settlements may involve broker fees or take time to process, so it’s essential to work with reputable companies and understand all costs involved.

Choosing Between Long Term Care Insurance and Life Settlements

If you’re comparing long term care insurance vs life settlements to determine the best option for covering healthcare costs, it’s crucial to evaluate your current situation and future needs. For those who already have long-term care insurance and can afford to maintain it, this coverage can offer peace of mind with predictable support for care services. However, for many who do not have this type of insurance or can no longer manage the premiums, a life settlement can be a valuable financial resource.

When a Life Settlement May Be the Better Choice

For people who find themselves unexpectedly needing care, a life settlement can provide immediate funds without requiring new health qualifications or high premiums. Whether the goal is to cover in-home care, pay down medical debt, or simply improve quality of life in retirement, a life settlement can provide flexibility and access to cash that might otherwise be tied up in a life insurance policy.

When it comes to long term care insurance vs life settlements, each offers unique advantages depending on your financial position and healthcare needs. Long-term care insurance can provide targeted support for care needs, but its premiums and health requirements may limit access for some. On the other hand, a life settlement offers a flexible alternative for those who need immediate funds and have an existing life insurance policy they no longer require for its original purpose.

To learn if you’re likely to be eligible for a life settlement, please give us a call today at 800-727-7654

When considering a life settlement, one of the most important questions is, “Do you qualify to sell your policy?” Understanding life settlement eligibility do you qualify? is key to determining whether you can turn your life insurance policy into a cash payout. In this post, we’ll explore the factors that determine life settlement eligibility and help you assess if selling your policy is an option for you.

What Is a Life Settlement?

Before learning about eligibility, it’s important to understand what a life settlement is. A life settlement involves selling your existing life insurance policy to a third party for more than its cash surrender value, but less than its death benefit. The buyer takes over ownership and beneficiary rights to the policy, continues paying the premiums, and ultimately collects the death benefit when the insured passes away.

Many people choose a life settlement when they no longer need their life insurance or if the premiums have become too expensive. The funds from selling a policy can be used for a variety of financial needs including medical bills, retirement expenses, or even a more affordable insurance plan.

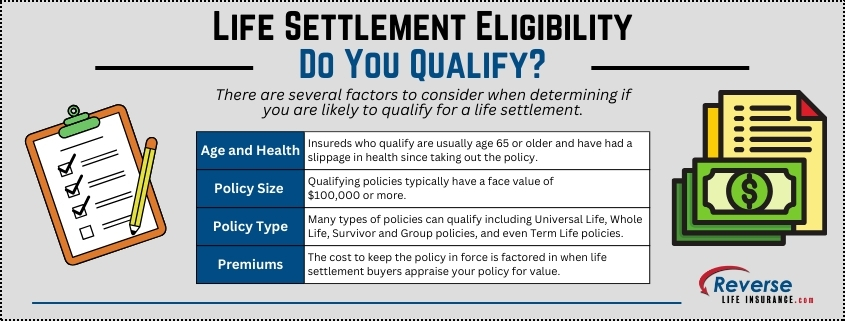

Age and Health: Two Key Factors

The first major factor in determining your eligibility for a life settlement is your age and health status. Typically, seniors that qualify for a life settlement are 65 or older, but this can vary based on health condition.

Age Requirements:

The general benchmark for qualifying is being at least 65 years old, but insureds who are younger may qualify if they have a chronic or terminal health condition. It is always best to give us a call to discuss your unique case.

Health Condition:

Health is a crucial aspect of life settlement eligibility. Buyers are more interested in policies from individuals with shorter life expectancies because they’ll receive the death benefit sooner. While you don’t need to be terminally ill, those with chronic or serious medical conditions are more likely to qualify.

Policy Size and Type Matter

The type and size of your life insurance policy can also impact your eligibility for a life settlement.

Policy Size:

Most life settlement purchasers look for policies with a face value (death benefit) of $100,000 or more. While smaller policies can sometimes qualify, they may not be as attractive to investors.

Policy Type:

Almost all types of life insurance policies can be sold in a life settlement. However, some policies are more appealing to buyers:

Universal Life: These policies are highly attractive because they offer flexibility in premium payments and potential cash value growth.

Term Life: Term policies can be eligible, but usually only if they can be converted into a permanent policy. Some non-convertible term policies may qualify for a viatical settlement if the insured is dealing with a serious health concern.

Whole Life: Whole life policies often qualify due to their guaranteed coverage and built-in cash value.

Variable Life: While more complex, variable life policies can also qualify.

Premium Amounts and Cash Surrender Value

Another factor affecting a policy’s eligibility for a life settlement is the amount of premium payments. Potential buyers will factor in costs to keep the policy in force over your expected lifetime when calculating an offer.

In some cases, policies with a high cash surrender value can still qualify for a life settlement, but this is generally not ideal for a life settlement. If your policy has no or little cash value, it can be more likely to qualify.

How Long Have You Held the Policy?

Most life settlement companies require that policies have been in force for at least two years. This is due to contestability clauses. If your policy is relatively new, it may not yet be eligible for a life settlement.

Financial and Legal Considerations

While not a direct factor in determining eligibility, there are several financial and legal considerations that can impact your decision to sell your policy.

Outstanding Loans on the Policy:

If you have taken out loans against your life insurance policy, this can reduce its overall value in a life settlement. Some buyers may still be interested, but they will deduct the loan balance from any offer they make.

Legal Ownership:

You must be the legal owner of the policy in order to sell it. If the policy is part of a trust or another entity holds ownership, a principal, such as a trustee, must be available to sign initial paperwork and the contract should you proceed with a sale.

Beneficiary Concerns:

If you’re considering selling your policy, it’s important to consider the needs of your beneficiaries. Once the policy is sold, the buyer becomes the new beneficiary, and your heirs will no longer receive the death benefit. Discussing this decision with your family can help avoid misunderstandings later on.

Getting a Life Settlement Valuation

If you’re unsure whether your policy qualifies for a life settlement, the best first step is to contact us for a no obligation policy appraisal. After learning your age, policy type and premiums, and approximate health condition, we will be able to let you know if you are likely to be eligible for a life settlement or viatical settlement.

A valuation can give you a better idea of what to expect, and whether it’s worth pursuing a life settlement based on your specific circumstances.

Should You Pursue a Life Settlement?

Deciding whether to sell your life insurance policy through a life settlement is a personal decision that depends on your financial situation, health, and future needs. While many seniors find life settlements to be a valuable source of extra income, it’s important to weigh the pros and cons carefully. If you no longer need your policy or can’t afford the premiums, selling it might be a smart financial move.

Life settlement eligibility depends on several factors, including your age, health, policy type, and size. While every situation is unique, understanding these core aspects can help you determine whether selling your policy is the right choice. If you think you might qualify, the next step is to consult a life settlement company for an initial evaluation.

Please give us a call at 800-727-7654 to learn if you are likely to qualify to sell your policy for cash.

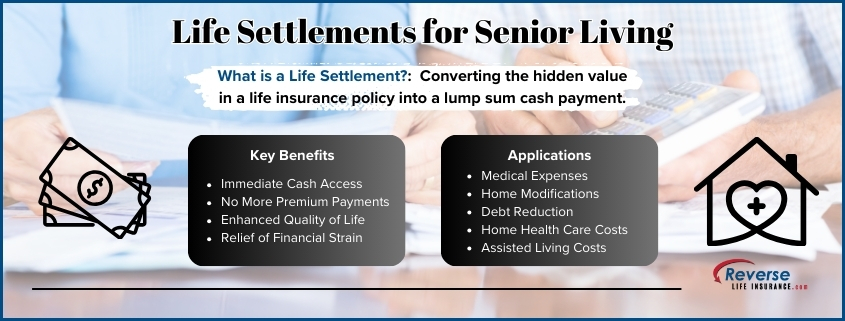

As seniors seek ways to fund their retirement and care needs, life settlements for senior living offer a practical solution. This innovative financial strategy allows policyholders to convert their life insurance policies into cash, providing the necessary funds for senior living expenses such as assisted living, in-home care, and medical bills.

Understanding Life Settlements

A life settlement involves selling an existing life insurance policy to a third party for a lump sum payment that exceeds the policy’s cash surrender value but is less than the death benefit. The buyer assumes responsibility for premium payments and collects the death benefit upon the policyholder’s passing.

Advantages of Life Settlements for Senior Living

Immediate Financial Relief: Provides quick access to funds for senior living expenses.

Elimination of Premium Payments: Reduces financial burden by removing the need to pay ongoing premiums.

Enhanced Quality of Life: Enables better living arrangements and care, improving overall well-being.

Detailed Benefits and Applications

Life settlements offer multiple advantages tailored to the specific needs of seniors:

Medical Expenses: Covering unexpected medical bills can be a significant concern for seniors. A life settlement provides the necessary funds to ensure that medical needs are met without compromising other aspects of daily living.

Home Modifications: For seniors who wish to age in place, making necessary modifications to their homes for safety and accessibility can be costly. Funds from a life settlement can be used to install ramps, modify bathrooms, and make other necessary adjustments.

Debt Reduction: Seniors often face various forms of debt, from mortgages to credit cards. Utilizing funds from a life settlement can help reduce or eliminate these debts, providing financial peace of mind.

Living Enhancements: Beyond basic needs, life settlements can fund hobbies, travel, and other activities that enhance the quality of life.

Factors to Consider

Policy Value: The amount received depends on the policyholder’s age, health, and policy specifics.

Tax Implications: Consult a tax advisor to understand potential tax consequences.

Eligibility: Not all policies qualify, so assessing the policy’s eligibility is crucial.

Steps to Take

Evaluate the Policy: Assess the policy’s eligibility and potential value by having your policy appraised.

Consult Professionals: Work with life settlement companies to determine potential value and consult with a trusted tax advisor to be aware of any potential tax implications.

Consider Alternatives: Explore other financial options to determine the best strategy.

Consulting Professionals

Working with professionals is critical when considering a life settlement. A life settlement broker can help navigate the complexities of the transaction, ensuring that the policyholder receives a fair offer. Financial advisors can provide a comprehensive view of how a life settlement fits into the overall financial plan, and tax advisors can clarify the tax implications of the transaction.

Potential Drawbacks

While life settlements provide significant benefits, there are potential drawbacks:

Reduced Inheritance: The death benefit intended for heirs is forfeited, which may not align with the policyholder’s initial goals.

Market Conditions: The amount received from a life settlement can be influenced by market conditions, the policyholder’s health, and the specifics of the policy.

Life settlements for senior living provide a valuable option for seniors needing financial support for their living and care needs. By unlocking the hidden value of a life insurance policy, seniors can achieve financial relief and improve their quality of life. Understanding the process and working with knowledgeable professionals can help maximize the benefits of a life settlement.

To find out if you’re likely to qualify for this valuable financial tool, please give us a call at 800-727-7654. It usually only takes a 5 minute phone call to find out if you’re eligible.

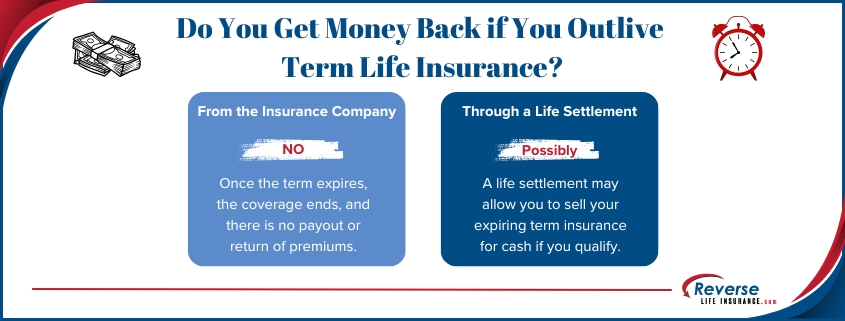

Term life insurance is a popular choice for many people because it offers substantial coverage at a relatively low cost for a specific period. However, a common question arises: what happens if you outlive your term life insurance policy? Do you get money back if you outlive term life insurance?

The short answer is no, you don’t get your premiums back at the end of a term life insurance policy. Unlike permanent life insurance, which includes a cash value component, term life insurance is designed to provide pure death benefit protection without any savings element. Once the term expires, the coverage ends, and there is no payout or return of premiums.

Understanding Term Life Insurance

Term life insurance provides coverage for a specified period, typically 10, 20, or 30 years. During this term, if the policyholder passes away, the beneficiaries receive the death benefit. If the policyholder outlives the term, the coverage ends, and no benefits are paid out.

The main advantages of term life insurance are its simplicity and affordability. It’s an excellent option for those who need coverage for a specific period, such as the duration of a mortgage, until children are financially independent, or while income replacement is necessary.

What Happens When the Term Ends?

When a term life insurance policy expires, you generally have a few options:

Renew the Policy: Many term policies offer a renewal option, allowing you to extend your coverage. However, this typically comes with significantly higher premiums since you’re older and possibly less healthy.

Convert to Permanent Insurance: Some term policies include a conversion option, which allows you to convert the term policy into a permanent one without undergoing a medical exam. This can be a beneficial option if you still need life insurance coverage and are concerned about qualifying for a new policy due to health reasons.

Let the Policy Expire: If you no longer need life insurance coverage, you can simply let the policy lapse. While you won’t get your premiums back, you’ve had the peace of mind that comes with being insured during the term.

The Life Settlement Option

For those who find themselves outliving their term life insurance but still have a need for some return on their investment, a term life insurance settlement might be an attractive option. A life settlement involves selling your life insurance policy to a third party for a lump sum payment that is more than the cash surrender value (if any) but less than the death benefit.

How Does a Life Settlement Work?

Eligibility: To qualify for a life settlement, policyholders generally need to be over the age of 65 and have a life insurance policy with a death benefit of at least $100,000. Health status can also play a role in determining eligibility and the payout amount.

Evaluation: The life settlement company will evaluate the policyholder’s age, health, and the terms of the policy to determine the value of the policy.

Offer: If the policy is deemed valuable, the company will make an offer. This offer is usually a lump sum payment that is more than the surrender value but less than the policy’s face value.

Transaction: Once the offer is accepted, the ownership of the policy is transferred to the buyer. The buyer continues to pay the premiums and receives the death benefit when the original policyholder passes away.

Pros and Cons of Life Settlements

Pros:

Immediate Cash: Provides immediate access to funds that can be used for medical expenses, retirement, or other financial needs.

Recoup Investment: Allows policyholders to recoup some of the money spent on premiums, which would otherwise be lost if the policy lapsed.

Cons:

Loss of Death Benefit: Beneficiaries will no longer receive the death benefit since the new owner of the policy will.

Tax Implications: The lump sum received from a life settlement may be subject to taxes.

Do You Get Money Back if You Outlive Term Life Insurance? While you won’t get your premiums back if you outlive a term life insurance policy, options like renewing the policy, converting it to permanent insurance, or opting for a life settlement can provide alternative solutions to address your financial needs. A life settlement, in particular, offers a way to unlock some value from your policy, ensuring that your investment in life insurance doesn’t go entirely to waste.

It only takes a short 5 – 10 minute call to find out if your policy is eligible for a life settlement. Please give us a call at 800-727-7654 today to learn if you qualify.

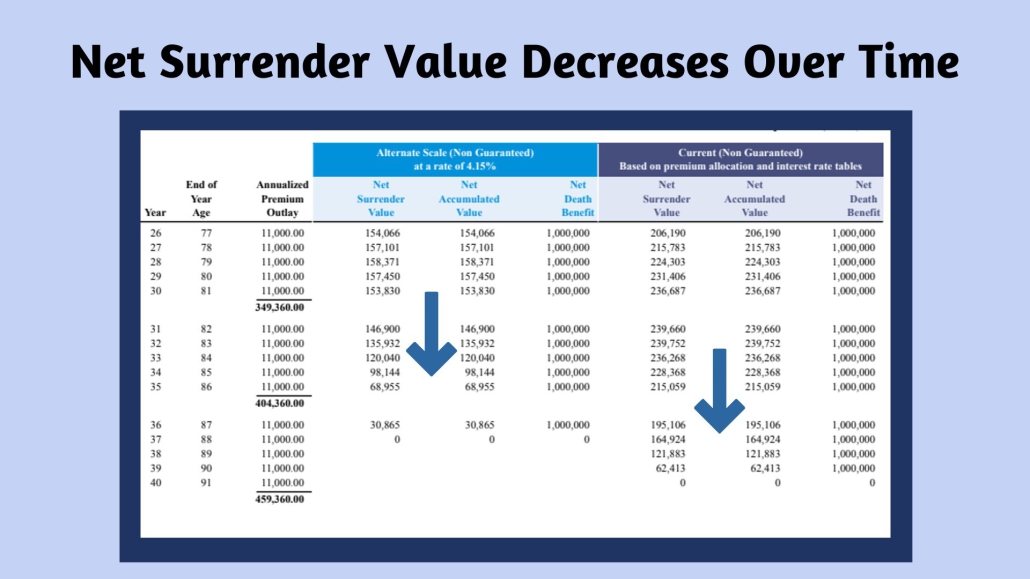

We speak with many long term financial advisers dealing with underperforming universal life insurance. Most remember writing universal life policies in the mid-eighties at 9% or more interest and having no qualms showing an illustration to that effect.

Underperforming Universal Life Policies

Though years and years of low interest rates have bolstered the stock market and the real estate market, insurance policies have largely underperformed the interest rates that were once illustrated comfortably.

What a lot of people don’t realize is that inside of a universal life insurance policy, the cost of insurance per 1000 increases exponentially as we age. The guaranteed cost of insurance rates on most universal life insurance policies do not guarantee that the policy will stay in force until age 100. There are many different approaches to this with respect to guaranteed provisions, target premiums, etc.. No two policies are exactly the same because no two people took them out at the exact same time, from the exact same company and paid the exact same amount during a low interest rate environment.

It’s very possible, in fact probable, that many policy owners who once saw their cash value going up, now see it plateauing or decreasing due to the rising cost of insurance. The scary part is that the less cash you have, the more insurance you have to pay for as the cost per 1000 increases dramatically.

Insurance companies rely heavily on life insurance policies lapsing. The best case scenario from an insurance company’s standpoint would be that you pay premiums for years and years and they never give you any money back and they never pay a death benefit.

Most policies lapse without ever paying a claim. In fact, over 642 billion dollars in face value of life insurance policies lapsed last year.

A Viable Solution – Life Settlements

Life insurance is no longer an all or nothing proposition. Reverse life insurance allows you to get the real hidden value of an underperforming universal life insurance policy in the form of cash today. Reverse life insurance is actually the opposite of life insurance with respect to qualifying. With reverse life insurance, the worse your health and the older you are, the more your life insurance policy is likely to be worth in the secondary market.

The cash surrender value or enhanced cash surrender value offer that you see on your statements for universal life are essentially an offer from your insurance company for your life insurance policy. Your policy may have a hidden value and it is your property to sell in a life settlement versus lapse.

If you’re an adviser, revealing this possibility to your clients might allow you to once again hold your head high, in case they hung on to the illustrations that you generated 35 years ago.

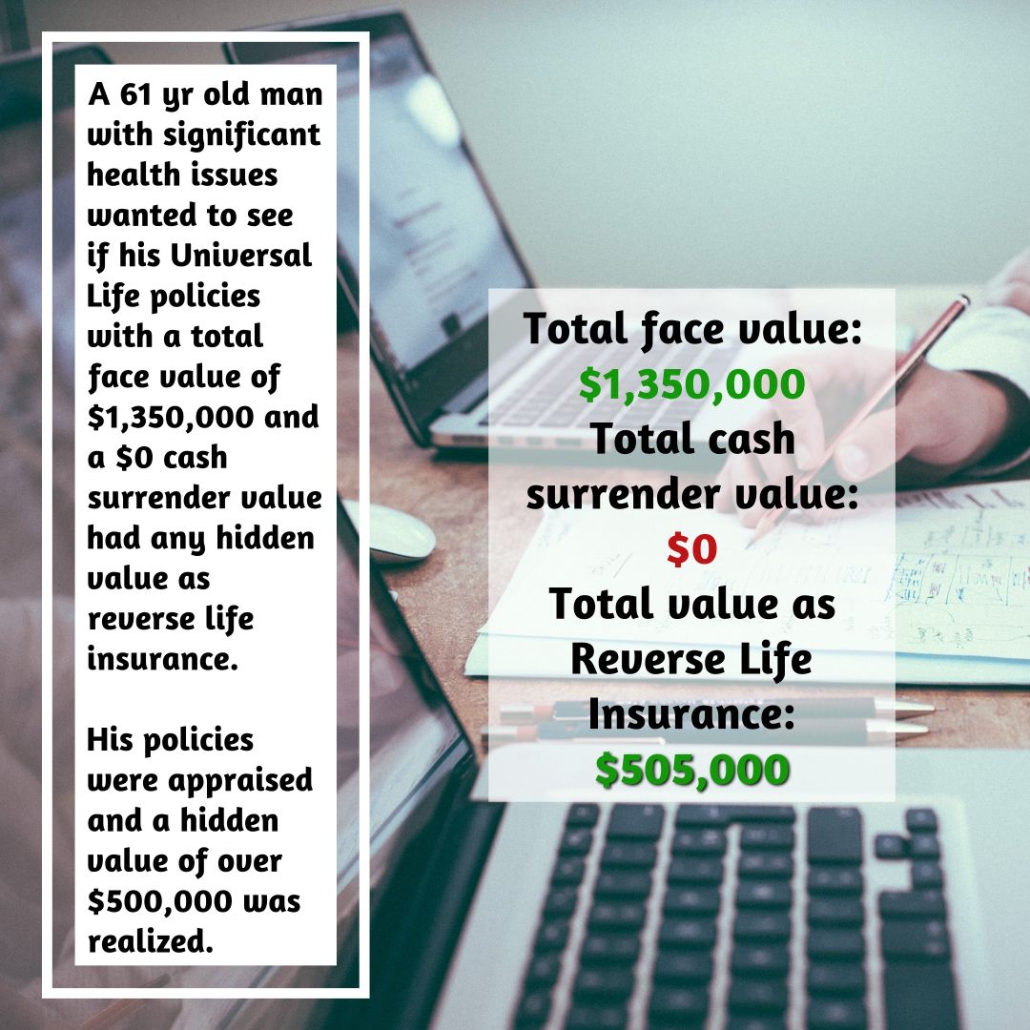

Universal life insurance policies with zero cash value and ready to lapse are often prime candidates for a life settlement. If someone has had any slippage in health, there’s a chance to qualify for something if you are over age 55 or 60.

Financial advisers dealing with underperforming universal life insurance policies now have an option. Not everyone and every policy qualify. Anyone over age 50 is crazy to lapse an underperforming universal life insurance policy without first having it appraised for hidden value.

The insured’s health is the main factor, but there are many factors to consider. Different guaranteed provisions, types of policies, different carriers and their ratings all matter. Each case must be considered on an individual basis.

Insurance companies and financial advisers are being sued for not informing their clients of their ability to possibly get more for their underperforming universal life insurance policy. Please do not allow someone to throw away a universal life insurance policy with no cash value without having it appraised. The hidden value can be life changing.

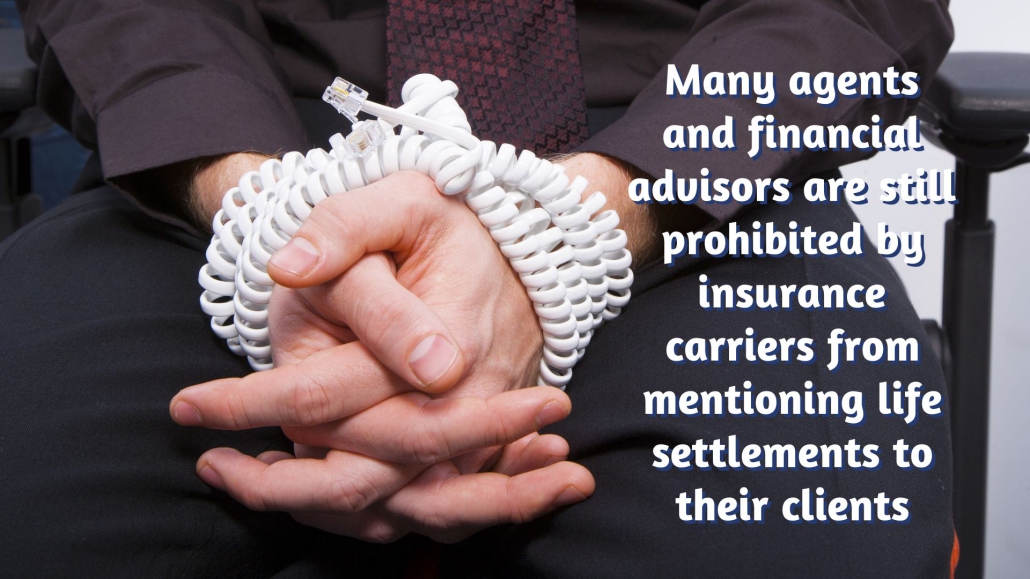

Financial Advisors and life settlements often do not mix. Your client, the person or even friend who has trusted your advice in financial matters for years, could sell their life insurance policy for cash. Yet, you allow them to just lapse or surrender it because the Life Insurance company you work for will not allow life settlements. There is a definite conflict here.

If you allow a client to cancel their policy because they cannot afford it without you ever informing them that there is a legal, regulated way to sell their policy to a licensed buyer, what liability do you create? Your client could receive the equivalent of 20 years of paid premiums back to them, tax free, for the TERM life insurance policy that they are lapsing, however you are not even permitted to offer the option. In this case, what can you do?

Reverse Life Insurance has helped thousands of people understand options for selling existing life insurance policies for over 15 years. We continue to help educate people on a daily basis. Nevertheless, there are still many who have never heard of any reverse life insurance options for their policies. As their trusted agent or advisor, you want to help your clients by offering them the best solutions. Whether they are seeking funds for medical treatments or simply want retirement planning advice, they look to you for guidance.

As a Senior Life Insurance Executive, our founder saw firsthand how valuable life insurance can be for families. In contrast, he also saw a darker side of the industry. Insurance carriers often encourage policyowners to lapse/cancel their policies for the meager cash value or nothing at all. However, these policies can often be sold in the secondary market for an exponentially higher amount than cash surrender value. Even policies with zero cash value often have a large hidden value as reverse life insurance.

“My initial exposure to life settlements and the secondary market for life insurance was in the late 1990’s. At the time, I was a Life insurance Executive in Toronto. The international insurance company I represented began terminating agents and management for transacting life settlements. Most were unethically financing the premiums of life insurance for resale. STOLI, or Stranger Originated Life Insurance, became the go to black eye to the secondary insurance market. Broker Dealers and Insurance Companies still reference this, keeping their clients in the dark about all of their options. It’s come full circle. Now is the time for the Insurance Industry to be reconciled” – Reverse Life Insurance Founder, CE Dean FICF

The Secondary Market for insurance is regulated, vibrant, and benefiting the general public the way it should. Life Settlements, Viaticals, Life Insurance Advances as well as other Reverse Life Insurance options now abound. Still, some Broker Dealers and Insurance Companies continue to contractually prohibit their agents and advisors from taking part in the sale of a life insurance policy as a life settlement in the secondary market. To be clear, their actions harm clients, create an almost insurmountable conflict and therein lies the problem.

Financial Advisors Now Have Access to Compliant Life Settlement Platform

Our Reverse Life Insurance platform allows clients of financial advisors to access hidden value in their policies as life settlements. In addition, it allows you to be hands-off during the transaction. That means that you don’t have to do anything beyond mentioning to your clients the possibility of selling their policy. After connecting with your client, we will discuss the qualification process with them directly. Everything we do is automated. We collect signatures for HIPAA and disclosure documents electronically. We order medical records and insurance policy documents and illustrations, securely storing them. After reviewing this medical and policy information, direct buyers will make an offer to your client based on their appraisal. Your client is welcome to discuss everything with you as their trusted advisor. However, you do not have to take part in the process.

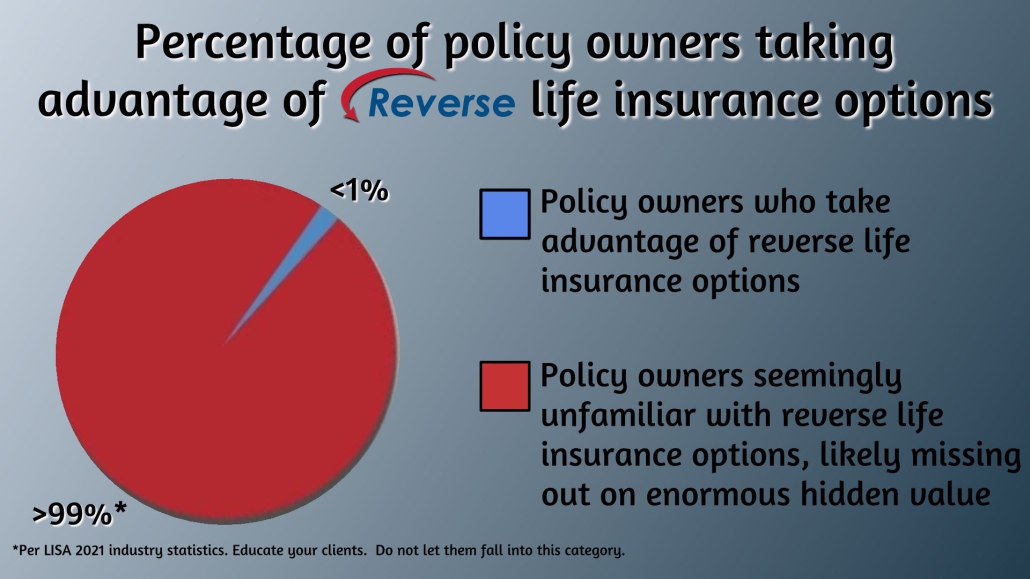

Less than 1% of those eligible for reverse life insurance ever take advantage of the life settlement option. People are simply unaware. Our direct licensed buyers pay a referral fee when a policy qualifies and is sold. If being held captive by your employer and unable to mention life settlements, know that anyone can make the referral. It is perfectly legal to pay a referral fee to someone or an entity that is not licensed if an employment contract has restrictions. Financial advisors and life settlements need to come together.

Financial Advisors Have Fiduciary Duty When It Comes to Life Settlements

Reverse life insurance options are valuable financial tools that can help your client retain value in a policy that they may otherwise lapse or surrender. Last year, over $642 billion dollars in face value of life insurance policies lapsed. Many of these policies could have and should have been sold instead. This would allow the policy owners to recoup some, all, or even more than the money actually paid in premiums.

Policy owners sold less than 1% of eligible policies last year. That is roughly 3,000 policies amounting to $4 billion in face value. These fortunate policy owners received over $750 million in cash payouts. The face value sold only represents less than 1% of the amount lapsed.

A life settlement is the sale of an existing life insurance policy to an investor fund for cash. The new owner takes over ownership and beneficiary rights to the policy and all responsibility for future premium payments. Life settlements and other types of reverse life insurance are legal and heavily regulated. In order to purchase policies, buyers must be licensed.

There are only five states that do not regulate life settlements; Alabama, Missouri, South Carolina, South Dakota, and Wyoming. Washington D.C. is also another unregulated jurisdiction.

What can you do when you have your client’s best interests at heart, but your employer has your hands tied? Beyond a moral obligation to consumers, are there legal reasons why you must consider advising a client about the possibility of selling their policy in the secondary market? Life settlements provide much more cash for the policyholder than a surrender or lapse of their policy. Therefore, not presenting reverse life insurance as an option could constitute a breach of fiduciary duty.

Advisors who neglect to tell clients about their reverse life insurance settlement options are being sued.

Advisors should be aware of the justifiable legal actions that policy owners have brought against carriers and advisors. The crime? Failing to disclose life settlement options. As precedent-setting legal actions against the concealment of information on life settlements come forth, more advisors educate their clients. It is both a smart business offering and protection against potential legal and financial liability.

In 2011, life insurance policyholders filed a lawsuit against John Hancock for violating Washington State’s Consumer Protection Act. Hancock’s appeal for summary judgment alleging the policyowner should have known about the secondary market on their own was denied. As a result, John Hancock settled the case prior to trial.1

In 2014, the owners of a life insurance policy filed a class-action lawsuit against their insurance company and advisor. This was in a state that doesn’t even have the disclosure mandate. The policy owner’s suit cited the “common and systemic practice” of “failing to inform and/or concealing from its insureds the option of a life settlement in connection with their life insurance policies.” The lawsuit sought damages based on the defendant “purposely omitting this information because it knows that other options, such as surrendering the policy (in whole or in part) or letting it lapse, will generate greater profits to the insurance company than a life settlement would.” The court confirmed that failure to disclose the life settlements option could result in financial harm to policyholders and beneficiaries. The case settled out of court in 2016.2

In 2016, a similar lawsuit was filed by the owners of a life insurance policy. The claims against the defendant were that they engaged in a “pervasive practice in the life insurance industry.” The defendant “instructs its own agents as well as independent agents that transact insurance to omit or conceal the option of a life settlement from its insureds.” The claim seeks compensatory damages and cites violations of the California Consumer Legal Remedies Act, financial abuse of an elder, and unlawful, unfair, and fraudulent business practices.3

The SEC approved Regulation Best Interest (Regulation BI) on June 5, 2019.4 The goal of this regulation was to impose higher standard of care rules for brokers, thereby protecting consumer interests.

Reverse Life Insurance Settlements Impacted by Regulation BI

After Regulation BI passed, the National Association of Insurance Commissioners created their own best interest standard. Many states adopted their own standards for insurance agents, some even more strict than the SEC’s policy. This regulation shows that that the government wants to protect consumers from conflicts of interest related to any financial services.

Of course the insurance company would prefer that policy owners surrender or lapse their unwanted or unaffordable policy. You have a responsibility to act in the best interest of your client though. Reverse life insurance almost always generates more cash than the surrender of a policy. Clients would almost certainly choose this option over a lapse or surrendering for a meager cash value.

Withholding information about life settlements that could potentially benefit your clients violates fiduciary responsibility and the “best interest standard” of Regulation BI.

Reverse life insurance is a legal, regulated transaction that can provide much-needed cash flow for seniors. It’s a viable financial strategy and is usually the most beneficial approach when someone longer needs or wants their life insurance.

Scenarios where a reverse life insurance settlement may benefit your clients:

They are considering lapsing or surrendering their policy.

He or she suffers from a chronic or terminal illness.

The client needs, but cannot afford, home healthcare or long-term care services.

They can no longer afford the premium payments on their existing policy.

Your client has altered their estate plan, is selling a business, or is retiring.

He or she needs a smaller policy or no longer needs life insurance.

Life Insurance Laws

Georgia Passes Law to Protect Agents and Financial Advisors Who Mention Life Settlements

Georgia is the first state to enact a law to specifically protect agents. Gov. Nathan Deal signed Georgia H.B. 193 into law on April 26, 2016. This law prohibits life insurance companies from punishing or terminating agents who inform their clients about life settlement options. Financial advisors now avoid negative action when mentioning this alternative to lapsing or surrendering a policy.

“The Life Insurance Consumer Disclosure Act” specifically states that: “an insurer shall not terminate or otherwise penalize an agent for apprising a policy owner of alternatives to the lapse or surrender of an individual life insurance policy”

Multiple States Have Enacted Laws to Protect Consumers

Georgia is currently the only state with a law protecting life insurance agents and financial advisors who mention life settlements. The following six states have mandatory disclosure laws to protect consumers though. These laws stipulate that life insurance companies must inform policyholders considering a lapse or surrender of possible life settlement options.

Kentucky

Maine

New Hampshire

Oregon

Washington

Wisconsin

A financial advisor equipped with thorough knowledge of reverse life insurance options can better help clients reach their financial goals. Advisors who fail to mention these options may be in direct violation of their fiduciary duty. Make your clients aware of alternatives to a lapse or surrender. It is important to do your homework and educate your clients about the best options available to them.

Financial Advisors and Life Settlements

Reverse life insurance is a portfolio of solutions that enable policyowners to sell existing life insurance policies for cash. They many simply no longer be able to afford premiums, no longer need insurance, or need funds for medical care. In any case, you can offer them solutions beyond surrendering or lapsing their policy. Be their advocate (and likely hero) by offering them a better option.

Real Life Examples:

Life Settlement

A widow in her early 70s who no longer needed her life insurance policy, but was in need of cash, contacted us to find out if her policy had any value as reverse life insurance.

Her $0 cash value $145,000 Universal Life policy got a cash offer of nearly 30%. This life settlement provided some much-needed funds to supplement her pension.

Viatical Settlement

A 67 year old man with significant medical issues was facing financial distress. He thought about lapsing his policy as the premium cost was too much of a burden. His agent suggested that he look into reverse life insurance.

He was able to sell his zero cash value $200,000 term life insurance policy for over $100,000, providing some desperately needed financial relief and relieving him of the $500 monthly premium payments.

The money he received through this viatical settlement allowed him to pay for treatment that his medical insurance didn’t fully cover.

Medicaid Life Settlement

A Medicaid life settlement allows policyowners to convert their life insurance policy into a plan to cover the cost of assisted living directly each month. Rather than surrendering or lapsing their policy in order to qualify for Medicaid, they are able to retain more of their policy’s value. This type of settlement is considered a qualified spend down of the policy.

An 83 year old woman’s family was faced with the necessity of selling off her assets and surrendering her $100,000 life insurance policy in order for her to qualify for Medicaid as she needed to move into an assisted living facility. Luckily, they contacted us about a Medicaid Life Settlement first. The policy was able to be converted into funds in an account to pay directly for her assisted living costs. Not only did these funds provide some relief, but because the settlement is a qualified spend down, she was able to qualify for Medicaid assistance.

Long Term Care Benefit Plan

A daughter called in to find out about funding options for her father who needed long term care. The family was paying out of pocket, but their funds were drying up and they were looking for a solution to help maintain his current standard of care.

The man owned several small life insurance policies. Two of the policies, a $50,000 policy with a loan against it, and a $25,000 policy provided an approximately $30,000 payout towards the cost of his care over the next 3 years.

This payout was set up to be paid directly to his long term care facility each month. The family was happy to be able to keep him in his preferred facility. In addition to the relief of having funds to pay for his care, they no longer needed to make premium payments on the insurance policies.

Retain-a-portion Reverse Life Insurance

A 75 yr old man owned a $500,000 Universal Life insurance policy. While he had heard about life settlements and was interested in seeing what his policy was worth, he wanted to retain some life insurance benefit for his family.

After evaluating his policy, our direct buyer was able to offer him a hybrid offer of $50,000 cash in addition to a retained death benefit of $100,000 for his beneficiaries. He was no longer responsible for premium payments and had some additional cash for living expenses.

Life Insurance Advance

A man was facing a terminal diagnosis at age 72. He wanted desperately to try some alternative treatments to prolong his life, but they weren’t covered by his health insurance policy.

His financial advisor had heard of life settlements and suggested that he contact us to see if the man’s $500,000 policy had any value as reverse life insurance.

Rather than selling the policy, he was able to obtain a life insurance advance loan of $175,000. He received funds to pay for the treatment he desired and he was able to maintain ownership and beneficiary rights to his life insurance policy.

When he passes away, his beneficiaries will receive the death benefit minus the total of the lump sum cash advance, premiums, fees, and interest. If he survives much longer than expected, he is under no obligation to make future premium payments or pay back the advance if there is not enough benefit left in his policy to cover it.

Testimonials

“Seldom do I write a testimonial. Reverselifeinsurance.com exceeded my expectations. My experience was stress-free. They informed throughout the process and the standard of professionalism was outstanding. I would absolutely recommend Reverselifeinsurance.com without hesitation.”

E.C.

“ReverseLifeInsurance.com connected me with a direct buyer who purchased my life insurance policy. The Buyer was excellent to work with through the entire transaction. They got me the cash I needed just 2 days before Christmas.”

Jim

“I really didn’t have the extra money to pay for the therapy I felt was best for me. I tried to get a life insurance cash advance, but they (the insurance company) said I wasn’t sick enough. Reverselifeinsurance.com’s direct buyer gave me $95,000 for my $250,000 policy! I just finished my 13th treatment. I told them I would recommend them to anyone, so now I am!”

J.M.

Our reverse life insurance platform is consumer oriented and connects policyholders with companies that buy life insurance policies direct. We created it to help people sell their insurance policy direct to licensed buyers, when their advisors are not permitted to assist them.

Advisors utilize our platform because allows you to stay out of the process. We handle everything, from the initial client contact to secure and compliant gathering of documents directly from the insurance carrier and physicians.

Once your client receives their sales proceeds, a referral fee is paid to whomever makes the referral. You don’t have to be licensed, just know someone who is lapsing their coverage and telling them to call us is all it takes

There are no more excuses for allowing your clients to miss out on the hidden value in their life insurance. Financial Advisors who make their clients aware of the options life settlements provide are acting in their best interest. Call us or have your clients call directly. Every case and every situation is different.

Reverse Life Insurance pays you to live. Don’t leave money on the table.

3 Joseph v. Kaye, et al., Case No. SC125276 (Cal. Super. Ct.)

4 SECURITIES AND EXCHANGE COMMISSION 17 CFR Part 240 [Release No. 34–86031; File No. S7–07–18] RIN 3235–AM35 Regulation Best Interest: The Broker-Dealer Standard of Conduct

Learn the benefits of life settlements vs surrender value and which option is best for you.

Learn the benefits of life settlements vs surrender value and which option is best for you.

Do You Qualify?

Do You Qualify?