When it comes to long term care insurance vs life settlements, many people find themselves comparing these options when they or their loved ones need funds to cover aging-related expenses. Long-term care insurance is designed to support individuals with the costs of long-term healthcare, but not everyone has a policy when they need it most. In fact, many people don’t anticipate the rising costs of care until they’re already facing them. For those without a long-term care policy in place or who find the premiums unaffordable, a life settlement can be a viable alternative, providing access to cash that can help pay for these expenses.

Understanding Long Term Care Insurance

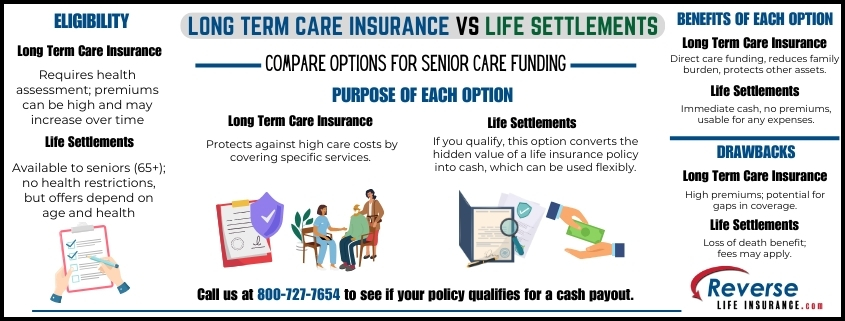

Long-term care insurance policies are specifically crafted to cover a range of services, such as in-home care, assisted living, nursing home care, and other support for daily living needs. Many individuals consider this type of insurance to avoid depleting their savings or relying solely on family members for support. However, qualifying for long-term care insurance is not always easy or affordable, particularly for older individuals or those with existing health conditions. Premiums for long-term care policies can also rise sharply over time, and many find it difficult to keep up with these increasing costs as they age.

In many cases, people reach retirement age without having secured a long-term care policy and then face the burden of high healthcare costs later. Additionally, even those who do have long-term care insurance may still encounter limitations on what their policy will cover, especially if they require specialized or extensive care.

What Is a Life Settlement?

A life settlement offers a way to access funds by selling an existing life insurance policy to a third-party buyer. Unlike a surrender value, which is generally a smaller payout, a life settlement allows the policyholder to receive a larger lump sum, which can often be used for any purpose—including healthcare or long-term care needs. This flexibility makes using life settlements to pay for long-term care an appealing choice for those facing unexpected healthcare expenses.

For individuals who do not have long-term care insurance, a life settlement can offer a financial solution that doesn’t require new qualifications or high ongoing premiums. Typically, life settlements are most accessible to seniors over 65 or those with health conditions that may shorten life expectancy, as these factors tend to yield higher offers. However, they can also be a suitable option for younger policyholders with significant healthcare needs.

Long Term Care Insurance vs Life Settlements: A Side-by-Side Comparison

Here’s a deeper look at the pros and cons of each option:

Long Term Care Insurance

Pros:

- Coverage for Care Services: Designed specifically to cover costs associated with long-term care, such as nursing homes, assisted living, or home care, which can relieve family members of the financial burden.

- Protected Assets: Allows individuals to receive care without needing to sell off other assets.

Cons:

- High Premiums: Premiums for long-term care insurance can increase sharply, especially as individuals age, making it less affordable for those on a fixed income.

- Health Requirements: To qualify, applicants often need to meet certain health criteria, which can exclude some individuals who already have significant healthcare needs.

- Potential for Limited Coverage: Not all policies cover all types of care, leaving policyholders with gaps in their care options.

Life Settlements

Pros:

- Immediate Cash Access: Life settlements provide a lump sum payment, giving individuals flexibility to cover any expenses they choose, including medical costs, home care, or assisted living.

- Freedom from Premiums: Selling a life insurance policy eliminates the need to pay ongoing premiums, which can be a relief for individuals with fixed or limited income.

Cons:

- Loss of Death Benefit: Once a life insurance policy is sold, beneficiaries no longer receive the policy’s death benefit. For some, this can be a significant drawback, especially if the policy was intended to support family members financially.

- Possible Transaction Fees: Life settlements may involve broker fees or take time to process, so it’s essential to work with reputable companies and understand all costs involved.

Choosing Between Long Term Care Insurance and Life Settlements

If you’re comparing long term care insurance vs life settlements to determine the best option for covering healthcare costs, it’s crucial to evaluate your current situation and future needs. For those who already have long-term care insurance and can afford to maintain it, this coverage can offer peace of mind with predictable support for care services. However, for many who do not have this type of insurance or can no longer manage the premiums, a life settlement can be a valuable financial resource.

When a Life Settlement May Be the Better Choice

For people who find themselves unexpectedly needing care, a life settlement can provide immediate funds without requiring new health qualifications or high premiums. Whether the goal is to cover in-home care, pay down medical debt, or simply improve quality of life in retirement, a life settlement can provide flexibility and access to cash that might otherwise be tied up in a life insurance policy.

When it comes to long term care insurance vs life settlements, each offers unique advantages depending on your financial position and healthcare needs. Long-term care insurance can provide targeted support for care needs, but its premiums and health requirements may limit access for some. On the other hand, a life settlement offers a flexible alternative for those who need immediate funds and have an existing life insurance policy they no longer require for its original purpose.

To learn if you’re likely to be eligible for a life settlement, please give us a call today at 800-727-7654

Do You Qualify?

Do You Qualify?