Did you know that you can turn your life insurance into cash when it’s no longer needed or becomes too costly to maintain? Many policyholders are unaware that selling their life insurance policy is an option that can provide significant financial relief. Known as a life settlement, this process allows you to sell your life insurance to a third party for more than its cash surrender value, but less than the death benefit, giving you immediate funds to meet current needs.

If your policy no longer fits your financial goals or is becoming a burden, a life settlement might be the right option for you.

What Is a Life Settlement?

A life settlement is a transaction where a policyholder sells their life insurance policy to a buyer in exchange for a cash payout. The buyer takes over premium payments and becomes the beneficiary, receiving the death benefit when the insured passes away. Life settlements offer policyholders a way to access the value of their life insurance while they are still alive, rather than surrendering it back to the insurance company for minimal value or letting it lapse.

This process has become more common as more people look for ways to tap into their assets to cover costs like healthcare, retirement, or simply to improve their quality of life. Instead of canceling a policy that no longer serves you, you can turn life insurance into cash that can be used for various needs.

Who Qualifies for a Life Settlement?

Not everyone will qualify for a life settlement, but several factors increase your chances of eligibility:

- Age and Health: Seniors age 65 and older with declining health are typically the best candidates for life settlements. Buyers are looking for policies with a shorter life expectancy to receive a return on their investment sooner. When appraising a policy for value, the buyer must consider the amount of time they will be paying premiums on the policy.

- Policy Size: Larger policies are more attractive to buyers, with most life settlements involving policies worth $100,000 or more. Some smaller policies may still qualify. If you are unsure, please give us a call to learn if yours may be eligible.

- Type of Policy: While universal life and whole life policies are the most common for life settlements, some term life policies can also be sold in a term life insurance settlement, depending on their conversion options and the insured’s health. Convertible policies may be able to be sold, even if the insured is in relatively good health. Non-convertible term policies may be eligible if the insured has a terminal diagnosis.

The life settlement market is growing, giving more flexibility to policyholders who might otherwise let their policies lapse. However, each case is unique, and eligibility will depend on several individual factors.

Why Turn Life Insurance into Cash?

There are many reasons someone might choose to sell their life insurance policy:

- Premiums Are Too Expensive: As you age, life insurance premiums can increase, especially for universal or whole life policies. If paying those premiums becomes a financial strain, selling the policy can relieve you of this burden while still giving you access to the policy’s value.

- Life Changes: Perhaps your original reasons for purchasing life insurance have changed. You may no longer have dependents relying on the policy’s death benefit, or your financial situation may have improved to the point where the coverage is no longer necessary. As you are planning future financial goals, it may be worth reconsidering whether the policy still aligns with your needs.

- Medical Expenses: Seniors often face significant medical costs that can drain savings and retirement funds. A life settlement provides a lump sum of cash that can be used to cover those expenses without depleting other assets.

- Supplement Retirement Income: Many people use life settlements to enhance their retirement lifestyle. Selling a life insurance policy can provide additional sources of retirement income to travel, pursue hobbies, or enjoy a higher quality of life during retirement.

- Debt Relief: If you have outstanding debts, a life settlement may be able to provide the funds necessary to pay them off, relieving financial stress and ensuring that your estate is debt-free for your heirs.

How Much Cash Can You Get?

The amount of money you can receive from selling your life insurance policy depends on several factors, including:

- The size and type of the policy

- Your age and health

- The amount of premium payments remaining

- The policy’s death benefit

- Current market conditions for life settlements

- Policy specifics and provisions

On average, policyholders receive anywhere between 10% to 30% of their policy’s death benefit, but this amount can vary widely. For example, a $500,000 life insurance policy could result in a life settlement payout of $50,000 to $150,000, depending on your circumstances. Some viatical settlements pay a much higher percentage. It is always wise to have your policy appraised for hidden value.

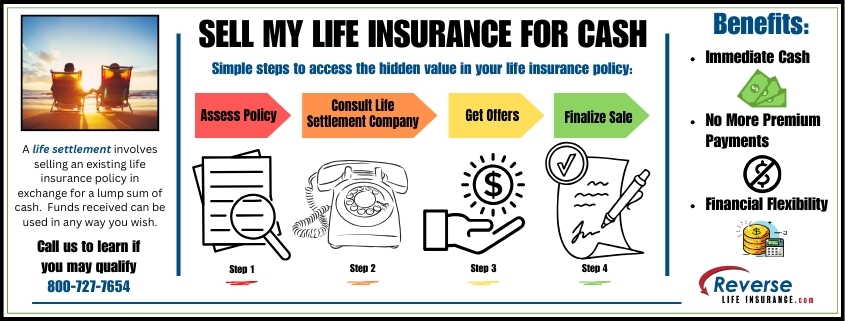

The Life Settlement Process

The process of turning your life insurance into cash is relatively straightforward. Here are the steps:

- Policy Review: The first step is to contact a life settlement company who will review your policy to determine whether it’s a good candidate for a life settlement.

- Application: If your policy is eligible, you may submit a formal application. This may require sharing information about your health, the policy, and your financial needs. With our direct platform, this step is greatly streamlined and you will only need to submit a few compliance forms rather than a lengthy application.

- Offer Review: If your policy has value and there is interest, you’ll receive offers from interested buyers.

- Accepting an Offer: Once you’ve reviewed the offers, you can accept the one that best meets your financial goals. The sale process will begin, and you’ll receive a lump sum payment in exchange for transferring ownership of the policy.

- Completion: The buyer takes over the policy’s premium payments and becomes the beneficiary, while you receive cash and no longer have any obligations regarding the policy.

Is a Life Settlement Right for You?

Turning your life insurance into cash can be an excellent option for those who no longer need the coverage or who are facing financial difficulties. However, it’s essential to consider the following:

- Impact on Estate Plans: Selling your policy means your beneficiaries will no longer receive the death benefit, so it’s crucial to consider how this will affect your overall estate plans.

- Tax Implications: Are life settlement proceeds taxed? Life settlement proceeds may be subject to taxes, depending on your individual circumstances. It’s a good idea to consult with a trusted tax professional to understand the tax impact of a life settlement. Typically, viatical settlement proceeds are not taxed.

- Alternatives: If a life settlement isn’t the right choice for you, there are other ways to access the value of your policy, such as a loan against the policy’s cash value or surrendering it for a smaller payout. Loans do require repayment and surrendering a policy usually results in a much lower payout than a life settlement.

For many, the ability to turn life insurance into cash can provide financial freedom and peace of mind. Whether you need to cover medical expenses, supplement your retirement, or simply no longer need the coverage, a life settlement offers a practical solution.

If you’re considering selling your life insurance policy, call us today at 800-727-7654 to learn more and find out if you’re likely to qualify for a life settlement.

Do You Qualify?

Do You Qualify?