Experiencing a stroke can dramatically shift a person’s financial and medical outlook. For seniors or their families, selling a life insurance policy after a stroke may offer a way to relieve financial pressure, particularly when long-term care, rehabilitation, or loss of income becomes a concern. While not everyone who’s had a stroke will qualify, a life settlement can be a powerful tool for those whose health has been seriously affected.

What Is a Life Settlement?

A life settlement allows a policyholder to sell their life insurance policy to a third-party buyer for a lump sum cash payment. The buyer takes over premium payments and receives the death benefit when the insured passes away. Life settlements are typically available to individuals over age 65, but younger people may qualify if they have serious health conditions such as the aftereffects of a stroke.

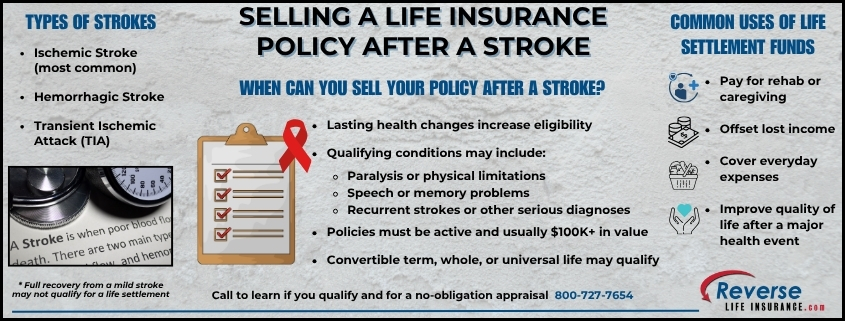

When a Stroke May Qualify Someone for a Life Settlement

A stroke, or cerebrovascular accident (CVA), can vary significantly in severity. A policy may be eligible for a life settlement if the insured has ongoing complications such as:

- Partial paralysis or weakness (hemiparesis)

- Difficulty speaking or swallowing

- Cognitive decline or memory problems

- Dependence on a caregiver for daily tasks

- Recurrent strokes or other comorbid conditions (such as heart disease or diabetes)

These long-term effects signal a substantial change in health from when the policy was originally issued, which is a key factor in determining eligibility. Those with a severely shortened life expectancy may be eligible for a viatical settlement.

When a Stroke May Not Qualify

It’s important to understand that not all strokes result in long-term health deterioration. If the stroke was mild (a transient ischemic attack or mini-stroke) and the individual made a full recovery with no lasting impairment, selling a life insurance policy after a stroke may not be an option. Life settlement buyers typically require evidence of a serious decline in health or a shortened life expectancy when considering a policy for purchase.

Types of Policies That May Be Eligible

The following types of policies are generally considered:

- Universal Life

- Whole Life

- Convertible Term Life (must still be within the conversion window)

Policies should generally have a face value of at least $100,000. The premium costs and remaining coverage length will also factor into a policy’s life settlement value. If your policy type is not listed, please give us a call. Every case is unique and it is always best to ask.

Using Funds from a Life Settlement

Proceeds from a life settlement can be used for:

- Home health care or assisted living

- Rehabilitation therapy or equipment

- Paying off debt or medical bills

- Covering everyday expenses during recovery

There are no restrictions on how funds are used. This financial flexibility can make a major difference during a time of uncertainty.

Selling a life insurance policy after a stroke is worth exploring for individuals whose stroke has led to lasting health challenges. It’s not always a guaranteed option, especially if the stroke caused no permanent damage, but for many, it may offer a source of much needed financial support.

To learn if you’re likely to qualify, please give us a call today at 800-727-7654. It usually only takes a 5-10 minute phone call to learn if you’re eligible to access the hidden value in your life insurance policy through a life settlement.

Do You Qualify?

Do You Qualify?