Policyowners sometimes reach a point where continuing life insurance coverage no longer fits their financial situation or long-term plans. Premiums may become difficult to maintain, or the estate planning purpose of the policy may have changed. When this happens, a common question arises: can a survivorship life insurance policy be sold for a lump-sum payment? In some situations, the answer may be yes. Certain policies that insure two individuals may qualify for a life settlement, allowing the policyowner to transfer the policy to a licensed purchaser in exchange for cash.

Understanding Survivorship Life Insurance Policies

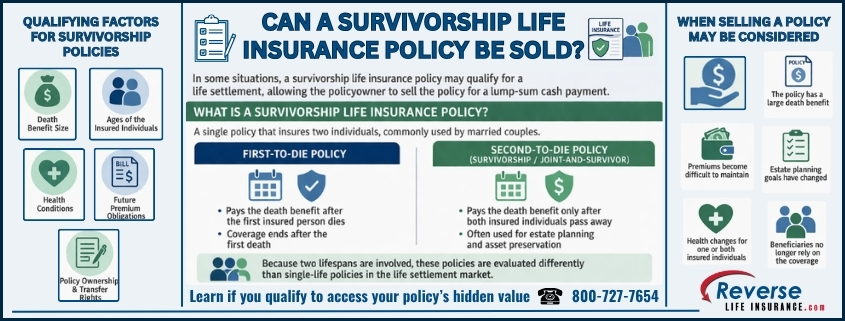

A survivorship life insurance policy insures two individuals under a single contract. These policies are commonly used by married couples as part of estate planning strategies.

There are two general structures used when a policy covers two insured individuals.

First-to-die policies

• The death benefit is paid when the first insured individual passes away.

• After the benefit is paid, coverage ends.

Second-to-die policies

• Often referred to as survivorship or joint-and-survivor policies.

• The death benefit is paid only after both insured individuals have passed away.

Because these policies rely on two lifespans, they are evaluated differently than single-life insurance policies when considering a life settlement.

When a Survivorship Policy May Qualify for a Life Settlement

In some situations, a policy covering two individuals may qualify for the life settlement market. Purchasers review a variety of factors to determine eligibility and whether acquiring the policy represents a reasonable long-term investment.

Common evaluation factors include:

• Policy structure

• Death benefit size

• Age of the insured individuals

• Health conditions of the insured individuals

• Required future premium payments

• Ownership rights and transfer provisions

Not every survivorship policy will qualify, but some may still have value depending on these factors. Because every case is different, it is always best to ask even if you aren’t sure of whether your policy qualifies.

Why Policies Covering Two Lives Are Evaluated Carefully

A survivorship policy pays benefits only after both insured individuals have passed away. Because of this structure, the expected timeline for the death benefit can be longer than with a single-life policy.

These policies are frequently purchased to help families manage estate taxes or preserve wealth for heirs. Over time, however, the financial situation that originally justified the policy may change. When that occurs, some policyowners begin exploring whether selling the policy may be an alternative to continuing premium payments.

Situations Where Selling the Policy May Be Considered

While eligibility varies, certain circumstances sometimes lead policyowners to explore a life settlement.

• The policy has a large death benefit

• Health changes have occurred for one or both insured individuals

• Premium payments have become difficult to maintain

• The original estate planning objective no longer applies

• Beneficiaries no longer rely on the coverage

Each policy is unique, so reviewing the contract details is the best way to understand what options may exist.

Alternatives to Canceling a Survivorship Policy

Many policyowners assume that if they no longer want life insurance coverage, their only choices are to keep paying premiums or cancel the policy. However, survivorship policies may present several possible paths depending on the contract terms.

Possible options may include:

• Keeping the policy if it still serves a financial planning purpose

• Surrendering the policy to the insurance company for any available cash value

• Adjusting coverage if the policy allows changes

• Requesting a life settlement appraisal to determine whether selling the policy may be possible

Understanding the policy provisions can help clarify which option makes the most financial sense.

Determining Whether a Survivorship Policy May Have Value

If you own a survivorship, joint life, or second-to-die life insurance policy, a policy appraisal can help determine whether the contract may qualify for the secondary market. This type of evaluation reviews the policy structure, premium obligations, and information about the insured individuals to determine whether purchasers may be interested.

In many cases, the review process takes only a few minutes and can help clarify whether selling the policy may be possible or whether another option may be more appropriate. To learn whether your policy may qualify, contact us today to request a no obligation policy review. 800-727-7654

Do You Qualify?

Do You Qualify?