What is a Life Settlement and How Does it Work?

A life settlement is an option for qualifying seniors who no longer need or want their life insurance policy. Instead of letting the policy lapse or surrendering it for its cash value, policyholders may be able to sell the policy for a lump sum that is more than the cash surrender value of the policy, but less than the death benefit. But what exactly is a life settlement, and how does it work? Here we’ll explore the details, benefits, and key considerations to help you determine if a life settlement is right for you. Not everyone or every policy will qualify.

What is a Life Settlement?

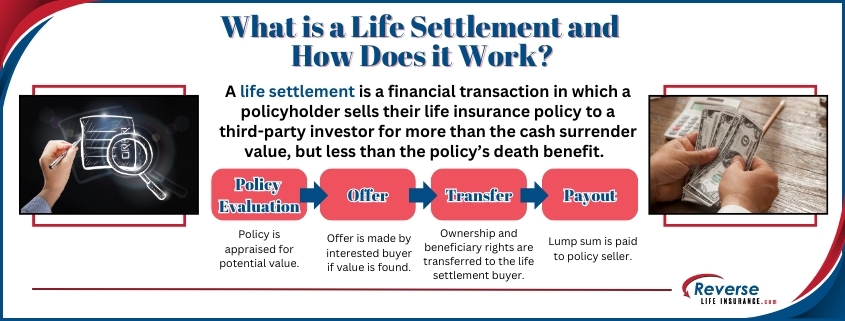

A life settlement is a financial transaction in which a policyholder sells their life insurance policy to a third-party investor. In exchange for a lump-sum payment, the buyer (most often an institutional investor) takes over the ownership and beneficiary rights of the policy and pays any future premiums. The payment received for your policy in this transaction is typically higher than the policy’s surrender value, but lower than its face value (the death benefit).

This option appeals to those who no longer need their policy for estate planning, have changing financial circumstances, or are facing increased medical costs in their senior years.

How Does a Life Settlement Work?

The life settlement process involves several key steps:

- Evaluation of Policy and Health

The first step is determining whether your life insurance policy qualifies for a life settlement. Typically, policies with a face value of at least $100,000 can be eligible and most policyholders who qualify are 65 years or older. The insured’s health also plays a significant role in the valuation, as investors calculate how long they may need to pay premiums before receiving the death benefit. - Appraisal of Policy Value

After determining eligibility, the life insurance policy is appraised by potential buyers. Factors such as the insured’s age, health, cost of premiums, and desired return on investment for the purchaser are evaluated to calculate an offer amount. - Policy Offer

If your policy qualifies and a buyer is interested, you’ll receive an offer based on the policy appraisal. - Acceptance and Transfer

If an offer is accepted, policy contracts and change of ownership and beneficiary forms will be completed. Once complete, policy ownership is transferred to the buyer. From that point on, the buyer is responsible for paying future premiums, and they become the beneficiary upon your passing. - Receiving the Lump-Sum Payment

After the transfer, the seller receives a lump-sum payment. The amount can vary based on factors like the insured’s life expectancy and policy value, but generally provides more cash than surrendering the policy directly to the insurance company.

Why Consider a Life Settlement?

There are several reasons why a policy owner might consider a life settlement over other options, such as letting the policy lapse or surrendering it for its cash value.

- You No Longer Need the Policy

Life insurance is often purchased to provide financial security for loved ones. As children grow up or financial situations change, the need for a life insurance policy may diminish. A life settlement allows you to convert your policy into cash rather than letting it lapse. - Premium Payments Have Become Unaffordable

As policyholders age, paying life insurance premiums may become burdensome, especially for those on a fixed income. A life settlement can help alleviate this financial pressure by eliminating the need to pay future premiums. - Increased Healthcare Costs

Seniors often face rising medical expenses. The lump-sum payment from a life settlement can help cover medical bills, long-term care, or other healthcare-related costs. - Improved Financial Flexibility

The cash from a life settlement provides immediate liquidity, which can be used for various purposes, such as debt repayment, travel, or reinvesting for future needs.

Who Qualifies for a Life Settlement?

Not every life insurance policyholder qualifies for a life settlement, but there are some general eligibility criteria:

- Age: Most insureds who qualify are at least 65 years old. Younger insureds may be considered if they have significant health issues.

- Policy Size: Typically, life insurance policies with a face value of $100,000 or more are eligible for life settlements. Some smaller policies may qualify, so it is always worth checking with us.

- Health Condition: The insured’s health plays a significant role in determining the policy’s value. This is because life settlement purchasers must consider how long they will be paying policy premiums or other related costs before receiving a death benefit.

- Policy Type: Universal life, whole life, and convertible term life insurance policies are most commonly accepted for life settlements. Term life policies that cannot be converted are generally not eligible unless the insured has had a significant slippage in health. Some survivor life policies as well as group policies can qualify. Please give us a call to learn if your policy type may be eligible.

Tax Considerations

Before proceeding with a life settlement, it’s important to understand the potential tax implications. The proceeds from a life settlement may be considered taxable income, depending on how much you’ve paid into the policy versus how much you receive. Consult your trusted tax advisor to clarify your individual tax situation.

Other Considerations

While life settlements offer numerous benefits, there are also some risks and drawbacks to consider:

- Loss of Death Benefit

Once the policy is sold, your beneficiaries will no longer receive the death benefit. For some, this might not be an issue, but it’s essential to assess whether your loved ones still rely on the payout from the policy. Some policy holders choose to share a portion of the funds received in a life settlement with loved ones. - Transaction Costs

Some life settlement transactions involve broker commissions that may reduce the overall payout. Be sure to understand the full financial picture before agreeing to a sale. Through our Reverse Life Insurance direct platform, there is no need to subtract a broker commission from the offer presented to you. - Limited Eligibility

Not all policies qualify for a life settlement, and even if you do qualify, the payout may not meet your financial expectations. A policy appraisal can help you learn if a life settlement is a viable option for you.

Alternatives to Life Settlements

When considering a life settlement or viatical settlement, there are alternative options to explore:

- Surrendering the Policy: Surrendering a policy returns its cash value to the policyholder but generally results in a lower payout than a life settlement.

- Policy Loans: Some life insurance policies allow for borrowing against the policy’s cash value. Be aware of interest rates and repayment amounts when considering this option.

- Reducing Premium Payments: Depending on the type of policy, it may be possible to adjust premiums or convert the policy to a lower-cost option, usually reducing the death benefit.

- Accelerated Death Benefits: This option is available for policies that have an accelerated death benefit (ADB) rider. Qualification varies by carrier and policy. Insureds are typically required to have a terminal health condition in order to receive accelerated benefits.

A life settlement can be a beneficial option for policyholders who no longer need their life insurance policy, find it difficult to keep up with premium payments, or who could benefit from a lump sum of cash for expenses such as medical bills. By selling the policy, you can receive a lump-sum payment that provides immediate financial flexibility.

Ultimately, understanding what is a life settlement and how does it work can help you make an informed choice that aligns with your financial goals. To learn if you are likely to qualify, please give us a call at 800-727-7654. We can assist you with a no obligation policy appraisal.

Do You Qualify?

Do You Qualify?