How to Cancel a Life Insurance Policy

If you’re looking for guidance on how to cancel a life insurance policy, you’re likely considering this option for financial reasons or because the policy no longer serves its original purpose. While canceling is a fairly straightforward process, it’s important to explore whether it’s truly the best decision. For many policyholders, a life settlement may offer a more beneficial alternative, especially if you’re unaware of the potential hidden value in certain policies like convertible term life insurance.

In this guide, we’ll walk you through the steps of canceling a life insurance policy, explore why cancellation might not always be the best idea, and explain how a life settlement could provide significantly more value.

Steps to Cancel a Life Insurance Policy

Canceling a life insurance policy isn’t complicated, but it does involve specific steps to ensure you’re no longer responsible for premiums. Here’s how to cancel your policy:

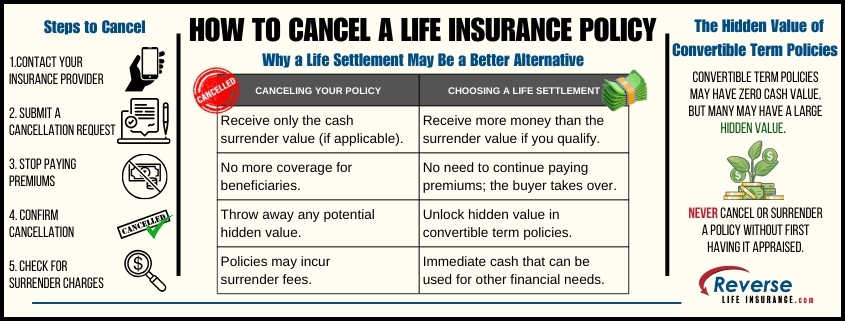

- Contact Your Insurance Provider

The first step is to get in touch with your insurance company. You can usually do this by phone or email, and they’ll provide specific instructions on how to cancel your policy. Be sure to ask about any forms or documentation they may require. - Submit a Formal Cancellation Request

Most insurance companies will ask you to fill out a cancellation form or submit a written request. Make sure to double-check your policy’s terms to ensure that there are no hidden fees or waiting periods before the cancellation becomes effective. - Stop Paying Premiums

If you’ve already decided to cancel, you’ll need to stop paying your monthly premiums. However, this alone won’t officially cancel your policy—formal cancellation is required to avoid any potential misunderstandings or future charges. - Confirm Cancellation in Writing

Always ask for written confirmation from your insurer once your policy has been canceled. This serves as your proof that your obligation to the policy has ended, and it can be important if any billing issues arise later. - Understand Surrender Charges

If you have a whole life or universal life insurance policy, canceling may incur a surrender charge. These are fees your insurer charges for canceling before the policy’s maturity date. Review your policy’s details to see if surrender charges apply.

Why Canceling Might Not Be the Best Idea

Canceling a life insurance policy seems like a straightforward way to stop paying premiums, but there are significant downsides to consider. Once your policy is canceled, your coverage is gone, and so are any future benefits. Additionally, if you want to purchase another policy later, you may find that it’s much more expensive due to age or health conditions that weren’t an issue when you first took out the original policy.

Before you cancel, it’s essential to weigh the pros and cons. If you’re struggling with premium payments or no longer need the coverage, you might think cancellation is the easiest route. However, there’s another option that can potentially give you more value for your policy—a life settlement.

Life Settlements: A Better Alternative if You Qualify

A life settlement allows you to sell your life insurance policy to a third party for a lump sum of cash. This payout is often much higher than the cash surrender value that comes with canceling a policy, making it a more financially sound choice for many policyholders.

Life settlements are especially valuable for individuals who no longer need their life insurance coverage but don’t want to walk away from the investment they’ve made. By selling the policy, you can receive an amount that is typically greater than the cash surrender value but less than the policy’s full death benefit. The buyer will take over paying the premiums and receive the death benefit when the original policyholder passes away.

This option is often available for people over the age of 65 with policies valued at $100,000 or more, but younger individuals with certain health conditions or convertible term policies may also qualify.

Hidden Value in Convertible Term Life Insurance Policies

If you have a convertible term life insurance policy, you might assume it has no value because term policies don’t accumulate cash value. However, convertible term policies can be incredibly valuable in the secondary market for life insurance.

Convertible term policies allow you to convert your term life insurance into a permanent policy without undergoing a medical exam. Once converted, the policy can be sold as part of a life settlement. For individuals with a term life insurance policy nearing the end of its term, this can be a game-changer, providing a hidden value where you thought there was none.

Rather than canceling a convertible term policy with no return, selling it through a term life insurance settlement can result in a substantial payout—far greater than the $0 value you’d receive by letting it expire or canceling it outright.

Advantages of Choosing a Life Settlement Over Cancellation

There are several reasons why a life settlement may be a better choice than canceling your life insurance policy:

- Higher Cash Value

When you cancel a life insurance policy, especially a whole or universal life policy, you may receive its cash surrender value. This is typically far less than what the policy is worth. In contrast, a life settlement offers a much larger payout, often between 10% to 30% of the policy’s death benefit. The amount that your specific policy is worth can vary widely depending on your age, health, and the policy provisions, so it is always best to have your policy appraised for value. - Eliminates Premium Payments

In a life settlement, the buyer takes over paying your premiums, freeing you from future financial obligations. If premiums are becoming too burdensome, this is a great way to relieve that pressure without giving up the policy’s value entirely. - Utilize the Hidden Value in Convertible Term Policies

As mentioned earlier, a convertible term policy may seem worthless at first glance. However, these types of policies are often attractive to life settlement purchasers. Selling the policy allows you to unlock hidden value that would otherwise go to waste if you canceled the policy or allowed it to lapse. - Provide Financial Flexibility

Life settlements offer immediate access to cash, which can be used for a variety of financial needs, including medical bills, long-term care, or retirement expenses. This liquidity can be especially beneficial for seniors who no longer need life insurance but could use additional funds.

Canceling a life insurance policy might seem like the simplest solution, but it’s important to explore all your options before making a final decision. A life settlement could provide significantly more value, especially for those with whole life, universal life, or convertible term policies. Before you cancel, consider whether a life settlement might be a better alternative for your financial future.

If you’re curious about whether you qualify for a life settlement or want to learn more about how much your policy might be worth, contact us at Reverse Life Insurance for a no-obligation appraisal. We can help you learn if you’re likely to qualify and explore the best options for maximizing the value of your life insurance policy. 800-727-7654

Do You Qualify?

Do You Qualify?