Are Life Settlement Proceeds Taxed?

If you’re considering selling your life insurance policy, one important question to address is: are life settlement proceeds taxed? The answer isn’t straightforward, as it depends on a number of factors, including your cost basis, the amount you receive, and whether the policy is classified as a term or permanent policy. In this post, we will break down how life settlements are taxed and help you understand what you might owe in taxes after cashing in your life insurance policy.

What is a Life Settlement?

A life settlement is a financial transaction where a policyholder sells their life insurance policy to a third party for a lump sum cash payment. Typically, the payment is higher than the surrender value offered by the insurance company but lower than the death benefit. Life settlements can be an attractive option for those who no longer need or want to keep paying premiums on their policy, are facing financial challenges, or are interested in monetizing their policy to improve their quality of life.

Taxation Basics for Life Settlements

The proceeds from a life settlement can be subject to taxes, but the specific tax treatment depends on a variety of factors. The Tax Cuts and Jobs Act (TCJA) of 2017 also impacted the taxation of life settlements, altering some of the rules around policy valuation and reporting requirements. It’s important to understand how these changes may affect the tax treatment of your life settlement. Let’s break down the general rules for life settlement taxation.

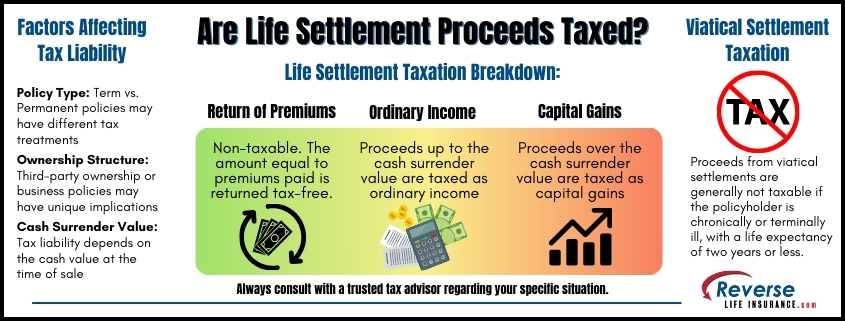

Return of Premiums

The first portion of the life settlement proceeds, up to the amount of premiums you’ve paid, is generally considered a return of your investment and is not subject to income tax. For example, if you have paid $50,000 in premiums over the life of the policy and receive $100,000 from the sale, the first $50,000 would be tax-free.

Taxation of Gains Above Cost Basis

Once you exceed the amount you have paid in premiums (your cost basis), the next portion is considered a gain. This gain is subject to income tax, but the classification of that tax depends on the nature of the gains.

Capital Gains Tax

If the proceeds you receive from the sale exceed the cost basis but do not exceed the policy’s cash surrender value, the difference is treated as ordinary income. Any amount above the cash surrender value may be considered a capital gain, which could qualify for lower tax rates.

In summary, life settlement proceeds are typically divided into three categories:

- The return of premiums (not taxable)

- Ordinary income (taxable up to the policy’s cash value)

- Capital gains (taxable at capital gains rates for any amount above the cash value)

An Example of Life Settlement Taxation

To make this clearer, let’s look at an example. Suppose you have a life insurance policy for which you have paid $60,000 in premiums. The cash surrender value of the policy is $80,000, and you manage to sell it for $120,000 in a life settlement.

- The first $60,000 you receive is not taxable because it represents the return of the premiums you paid.

- The next $20,000 (which represents the difference between your cost basis and the cash surrender value) is taxable as ordinary income.

- The remaining $40,000 (the amount over the cash surrender value) is taxable as a capital gain.

Factors that Affect Taxation

There are several factors that can affect how much tax you owe on your life settlement proceeds:

Policy Type

The type of life insurance policy (permanent vs. term) can influence the taxation. For instance, term policies may be eligible for different treatment since they often lack a cash surrender value.

Ownership and Beneficiaries

If the policy was part of a business, or if a third party paid the premiums, the tax implications might be different. Ownership structure plays a crucial role in determining taxable events.

Age and Health

Your age and health condition might also influence the settlement offer and taxation implications. Generally, older policyholders or those with health concerns might receive higher offers, impacting how much is taxable.

Are There Any Exemptions?

In certain circumstances, life settlement proceeds may be tax-exempt. For instance, if the policy qualifies as a viatical settlement—meaning it was sold by someone who is chronically or terminally ill—then the proceeds are often entirely exempt from taxation. Viatical settlements are treated differently because they are considered to be an advance of the death benefit and a source of financial support for individuals dealing with severe health challenges.

Consult a Tax Professional

It’s essential to consult with a trusted tax professional to make sure you understand the tax implications. The TCJA introduced new reporting requirements for insurance companies, which means you may need to provide additional documentation when filing your taxes. A tax advisor can help you navigate these complexities. Tax rules can be complicated, and missteps can be costly. A tax advisor can help you determine your cost basis, calculate potential taxes owed, and even explore strategies to minimize your tax liability. Since the IRS treats life settlements differently depending on each policyholder’s unique situation, professional advice can ensure you fully understand your obligations.

Other Financial Considerations

Beyond taxation, there are additional financial implications to consider before deciding on a life settlement:

- Impact on Government Benefits: Receiving a lump sum from a life settlement could impact your eligibility for certain government benefits, like Medicaid. It’s important to understand how the extra income will affect your financial standing. A medical life settlement might be a valuable option if this is a concern for you.

- Estate Planning: If your life insurance policy was part of your estate plan, selling it may impact the inheritance you leave behind. The death benefit that would have gone to your beneficiaries will be forfeited once the policy is sold.

So, are life settlement proceeds taxed? Yes, in most cases, life settlement proceeds are taxable, but how much you owe will depend on factors like your cost basis, the cash surrender value, and whether the policy qualifies as a viatical settlement.

Understanding the tax implications is important. If you’re considering a life settlement, it’s wise to understand the financial and tax consequences fully. Consult with a tax advisor and evaluate your options carefully to ensure that you make the best decision for your financial future.

To learn if you are likely to qualify for a life settlement, please give us a call today at 800-727-7654.