How to Tell If Your Life Insurance Policy Is Eligible for Sale

Life insurance is often thought of as a safety net for your loved ones, but many policyholders don’t realize that their policies can also be sold for cash while they’re still alive. This process, known as a life settlement, allows you to access the hidden value of your policy, turning it into a financial asset you can use now. But how do you know how to tell if your life insurance policy is eligible for sale? Understanding the criteria for eligibility, gathering the right documentation, and knowing what questions to ask your insurance carrier are key steps in this process.

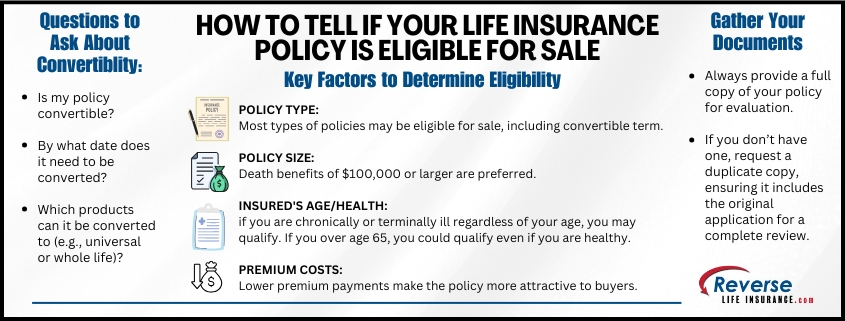

Factors That Determine Eligibility

Not all life insurance policies qualify for sale. Here are the primary factors that determine eligibility:

- Policy Type:

Permanent policies, such as whole life or universal life insurance, are the most commonly sold because they have ongoing cash value and lifetime coverage. However, term policies may also qualify if they are convertible to permanent insurance. - Policy Size:

Policies must usually have a death benefit of $100,000 or more to be eligible for sale. However, some smaller policies may still qualify, so it is always best to ask. - Insured’s Age and Health:

Policies covering individuals over 65 or those with serious health conditions are will often qualify. Buyers consider life expectancy when determining whether a policy is a good investment. - Premium Costs:

Policies with lower premiums relative to the death benefit are more marketable. High premiums can reduce the policy’s appeal to potential buyers because they increase the overall cost of maintaining the policy.

Why Convertibility Matters for Term Policies

If you own a term policy, one of the most important factors in determining its eligibility for sale is whether it is convertible. Many term policies come with a provision that allows you to convert them into permanent insurance, such as whole or universal life, before a specific deadline. This is a crucial detail because only permanent or convertible term policies can typically be sold in the life settlement market.

When reviewing your term policy, ask your insurance carrier the following questions:

- Is my policy convertible?

- By what date does it need to be converted?

- Which products is it eligible to be converted to? (e.g., universal life or whole life insurance?)

Convertible term policies allow you to change the term coverage into permanent insurance, which can then often be sold without the need to complete the conversion process yourself. Understanding these details is crucial to determining your options.

The Importance of Having a Copy of Your Policy

To accurately evaluate your life insurance policy, you will need to provide a complete copy of the policy, including the original application. This documentation is essential for buyers to understand the policy’s terms, premiums, and other critical details.

If you don’t have a copy of your policy, you can request a duplicate from your insurance carrier. Be sure to specify that you need a copy of the policy that includes the original application, as this is often a requirement in the life settlement process. Having all the necessary paperwork ready can streamline the evaluation and help you get an accurate assessment of your policy’s value.

Additional Considerations for Selling Your Policy

Once you’ve determined that your policy might be eligible for sale, it’s important to consider the following steps:

- Work with an Experienced Life Settlement Company:

Navigating the life settlement market can be complex, and working with an experienced life settlement company is essential. We have been helping policy holders sell their policies to direct buyers for nearly 20 years. - Evaluate Your Financial Needs:

Selling a life insurance policy can be a valuable financial resource, but it’s not the right choice for everyone. Consider your long-term financial goals and how selling your policy fits into your overall strategy. - Understand the Tax Implications:

Are life settlement proceeds taxed? Proceeds from a life settlement may be subject to taxation, depending on factors like the cash surrender value of the policy and how much you’ve paid in premiums. Consult with a tax advisor to understand the potential impact on your financial situation.

Why Selling Your Policy Can Be a Smart Choice

For many people, selling a life insurance policy is a way to access funds for medical expenses, retirement needs, or other financial priorities. Whether your policy has become a burden due to high premiums or you no longer need the coverage, a life settlement can provide an immediate cash payout that can make a significant difference in your financial well-being.

Understanding how to tell if your life insurance policy is eligible for sale begins with knowing your policy’s type, terms, and value. Asking the right questions about convertibility, gathering all necessary documentation, and consulting with a professional can help you make an informed decision.

If you’re considering selling your policy, start by requesting a copy of your policy and ensuring it includes the original application. Then, give us a call at 800-727-7654 for a no obligation policy appraisal. With the right guidance, you can turn your policy into a valuable financial asset that works for you now.