Sell My Life Insurance for Cash

As life circumstances change, many policyholders find themselves reconsidering the value of their life insurance policies. If you’ve ever wondered, “Can I sell my life insurance for cash?” you’re not alone. This option is becoming popular among those looking to unlock the cash value of their policies for immediate financial needs. In this post, we’ll explore how to sell your life insurance for cash, the benefits of doing so, and key considerations to keep in mind.

What Does It Mean to Sell My Life Insurance for Cash?

Selling your life insurance policy as reverse life insurance, often referred to as a life settlement, means transferring ownership of the policy to a third party in exchange for a lump sum payment. The option to turn life insurance into cash is appealing for various reasons, from financial necessity to changing life situations. When selling a policy through a life settlement, the offer you receive will always be higher than the cash surrender value offered by the insurance company, but lower than the death benefit of the policy.

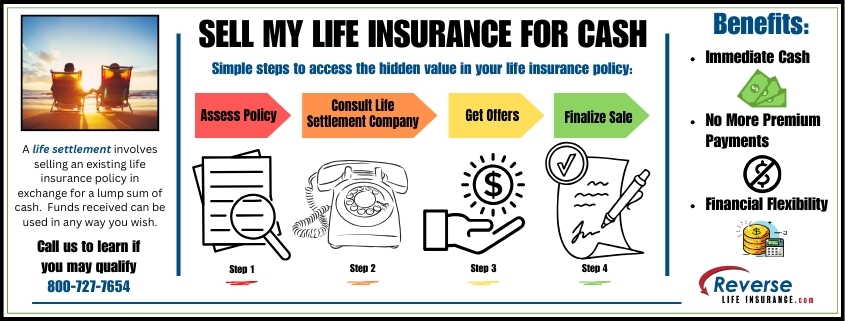

Steps to Sell Your Life Insurance Policy

The process of selling your life insurance can be straightforward if you understand the steps involved:

- Assess Your Policy: Start by reviewing the details of your life insurance policy. Note the face value, type of policy, and your current health status. Policies typically eligible for sale have a face value of $100,000 or more. Some smaller policies can qualify. Please give us a call and we’ll be happy to help you learn if your policy may be eligible.

- Consult with Professionals: Engage with a reputable life settlement company who can guide you through the evaluation process. They will help you determine if your policy qualifies and what its potential market value might be. Reverse Life Insurance has been helping people sell their policies direct to life settlement purchasers for nearly 20 years.

- Obtain a Policy Appraisal: A thorough appraisal will consider factors like your age, health, and the policy’s terms. Life settlement companies will use this information to estimate the amount you could receive from the sale.

- Review Offers: After the appraisal, you will receive offers from potential buyers if value is found and they are interested in purchasing your policy.

- Complete the Sale: If you accept an offer, you’ll need to sign the necessary paperwork to transfer ownership and beneficiary rights of the policy. Once the sale is finalized, the new owner takes over premium payments and becomes the beneficiary.

- Receive Your Cash: After the transfer, you will receive your lump-sum payment, providing you with immediate funds to use as needed.

Benefits of Selling Your Life Insurance

Selling your life insurance for cash can offer several advantages:

- Immediate Cash Flow: The most significant benefit is the immediate access to cash. This can be crucial for paying off debts, covering unexpected expenses, or simply improving your financial situation. Some policy sellers even use the funds to pay for vacations with loved ones.

- No More Premium Payments: Once you sell your policy, you are relieved of the obligation to make ongoing premium payments, which can be a significant relief.

- Flexibility: The cash obtained from selling your policy can be used for a wide range of purposes—whether you want to invest in a new opportunity, fund medical expenses, or treat yourself to a long-deserved vacation.

- Tailored Financial Strategy: By converting your life insurance into cash, you can reassess your financial strategy to better align with your current needs and goals.

Who Should Consider Selling Their Life Insurance?

Not every policyholder should sell their life insurance policy. However, certain situations may warrant this decision:

- Changing Life Circumstances: If your financial needs have changed—perhaps you no longer have dependents or your circumstances have shifted—it may be time to reconsider the necessity of your life insurance.

- Unmanageable Premium Payments: For many, the cost of premiums can become a financial burden, especially for those on fixed incomes. Selling the policy can relieve this pressure.

- Underperforming Policies: Sometimes, it can be beneficial to sell an underperforming policy and use the funds received to purchase a new policy. This does not make sense for everyone, but is an option you may want to discuss with your trusted personal financial advisors.

- Increased Healthcare Costs: Rising medical expenses can be a challenge. The cash received from a life insurance policy sale can help cover these costs.

Considerations Before Selling

While there are many benefits to selling your life insurance, it’s important to consider a few key factors:

- Loss of Coverage: Selling your policy means you will no longer have the life insurance coverage provided by that policy. This is a critical consideration, especially if you have dependents who may rely on the death benefit. Some policyholders choose to sell only some of their policies or a portion of a policy. If you are considering a life settlement, but may be interested in a retain a portion settlement, please reach out to see if you may qualify for this option.

- Tax Implications: The proceeds from selling your life insurance may be subject to taxes, depending on the difference between what you paid into the policy and what you receive from the sale. Consulting your trusted tax professional is recommended to understand your specific situation. If you qualify for a viatical settlement, the proceeds are usually tax-free.

- Potentially Lower Offers: Not every policy will fetch a high price. Be prepared for the possibility that offers may not meet your expectations, especially if your health is relatively good or the market conditions are unfavorable.

Real-Life Scenarios

Consider these examples of individuals who successfully sold their life insurance for cash:

- Debt Management: A retiree facing credit card debt sold their life insurance policy to pay off their balance, achieving peace of mind and financial stability. They no longer needed the policy as they did not have any beneficiaries to leave it to.

- Healthcare Needs: An individual diagnosed with a chronic illness opted to sell their policy to cover mounting medical bills, alleviating financial stress during a difficult time. They were also able to pay for alternative treatments not covered by their medical insurance.

- Investment Opportunities: A policyholder who no longer needed their life insurance sold their policy to invest in real estate, leading to long-term financial growth.

Selling your life insurance for cash can be a smart financial decision that offers immediate benefits and enhances your overall financial flexibility. If you’re considering this option, it’s essential to understand the process, weigh the benefits against the potential drawbacks, and consult with professionals who can guide you.

We specialize in helping policyholders navigate the life settlement process. If you’re ready to explore your options, contact us today to see if selling your life insurance policy may be an option for you. 800-727-7654