Cashing out the hidden value in life insurance is a strategy many policyholders overlook. Most people assume their policy only provides benefits after death, but the truth is that it can also serve as a living financial resource. Through a life settlement, you may be able to sell your policy for a cash payout that far exceeds the surrender value offered by the insurance company.

Why Life Insurance Has Hidden Value

Life insurance policies, especially permanent and convertible term policies, can hold financial value that isn’t immediately obvious. Some policies accumulate cash value, while others may qualify to be sold in the secondary market. Investors purchase these policies, continue paying the premiums, and receive the eventual death benefit.

For policyholders, this creates an opportunity. Instead of walking away with little or nothing when a policy is no longer needed, selling it to a direct buyer through a life settlement can unlock far more than what the insurance company would pay out in surrender value.

What It Means to Cash Out Through a Life Settlement

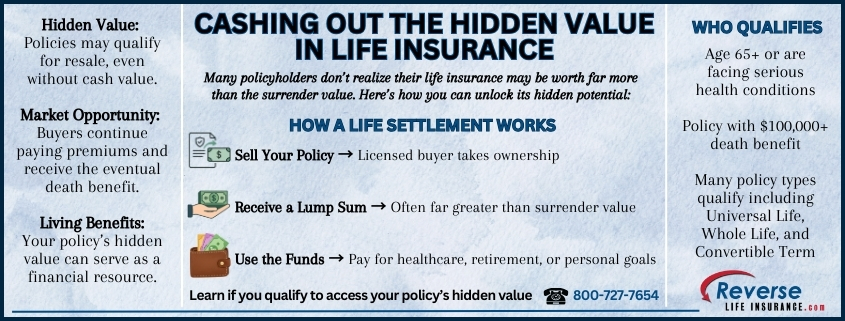

A life settlement involves selling your life insurance policy to a licensed buyer in exchange for a lump-sum payment. Once the sale is complete, the buyer takes over responsibility for premium payments and becomes the new owner and beneficiary. The policyholder receives immediate cash, which can be used for:

- Covering healthcare or long-term care costs

- Paying off debt or household expenses

- Supplementing retirement income

- Funding lifestyle goals or personal priorities

Unlike borrowing against your policy or making withdrawals, this option completely transfers ownership and premium responsibility to the buyer. If your policy qualifies, you may even be eligible for a retain a portion settlement where you keep part of the death benefit for your family while the buyer still takes over premium payments.

Who Qualifies to Access This Hidden Value

Not every policy qualifies for a life settlement, but many do. Common eligibility factors include:

- Policyholder age, often 65 or older, or having a serious health condition

- A policy with a death benefit of $100,000 or more

- Permanent coverage types (universal, whole life) or term policies that are convertible

Even policies with little or no cash surrender value may still qualify, making it worthwhile to explore the option. Because every case is unique, it is always best to call.

Why Policyholders Consider This Option

The reasons people choose to cash out vary, but they usually center on changing financial needs. Some policyholders no longer want to pay premiums, while others realize the original purpose of the policy, such as providing for dependents, is no longer relevant.

For many, selling a policy creates the flexibility to cover current expenses. A settlement can mean the difference between struggling to keep up with bills and having funds available to improve quality of life.

Taking the Next Step

If you are considering cashing out the hidden value in life insurance, the first step is to request a no-obligation appraisal of your policy. This evaluation will show whether your coverage qualifies for a life settlement and how much you could potentially receive.

To learn if you qualify, please give us a call at 800-727-7654

Do You Qualify?

Do You Qualify?