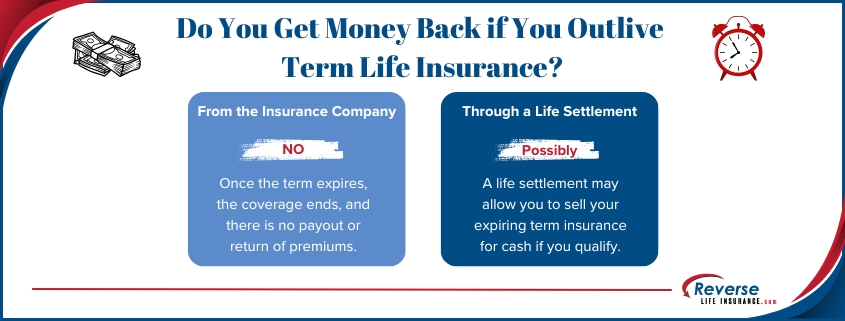

Many policyholders are surprised to learn that a life settlement for term insurance may be possible. While term policies typically do not build cash value, they can sometimes be sold for a lump sum if the policy includes a conversion option and the insured has a qualifying health condition.

Can You Sell a Term Life Insurance Policy?

Most term policies cannot be sold on the secondary market unless they include a conversion privilege. This feature allows the policy to be converted into permanent coverage, which meets the requirements of most life settlement buyers. However, the policy does not always need to be converted in advance. It only needs to be eligible for conversion to be likely to qualify for a life settlement.

Buyers may also consider term policies that remain in force beyond the level term period, such as annual renewable term policies. If premiums are being paid and the insured meets the usual health and age criteria, a sale might still be possible.

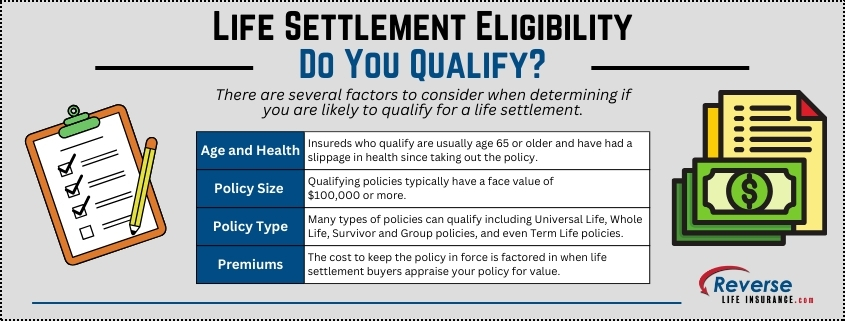

Key Factors That Determine Eligibility

Several factors influence whether a term policy may qualify for a life settlement:

- Conversion deadline: Many term policies have a limited window during which they can be converted. If that window has passed, the policy may no longer be eligible

- Insured’s health: Life expectancy is a major factor. Policies held by individuals with serious health conditions tend to be more attractive to buyers

- Policy size: Most buyers look for policies with a death benefit of at least $100,000

- Age of the insured: Seniors over the age of 65 are most likely to qualify, but exceptions may apply. Younger insureds with significant health concerns can qualify.

What Is the Process?

The process begins with a review of your policy and some basic health information. If the policy has a conversion option and you meet other eligibility criteria, buyers be interested and make you an offer.

If you accept an offer, the direct buyer takes over premium payments and receives the death benefit in the future. You receive a lump-sum cash payout now.

Why Consider Selling a Term Policy?

Many people let term policies lapse once they are no longer needed or become too expensive. If your policy qualifies for a life settlement, it may offer:

- A cash payout that can be used for any purpose

- Relief from paying future premiums

- Greater financial flexibility during retirement or illness

Selling a term policy can be a practical way to unlock value from coverage that would otherwise expire unused.

Check Before You Let It Lapse

Before you stop paying premiums or allow a term policy to expire, find out whether you may qualify for a term life insurance settlement. A quick policy review could reveal unexpected value, especially if your coverage includes a conversion option and your health has changed since the policy was issued.

Many people simply cancel their expiring term policies at the end of the term as premiums can steeply rise after the initial term period. A life settlement for term insurance may allow you to access your policy’s hidden value rather than throwing it away. Please give us a call at 800-727-7654 to learn if you qualify.

Do You Qualify?

Do You Qualify?