Using Life Settlements to Pay for Long-Term Care

As the cost of long-term care continues to rise, many individuals and families are seeking alternative ways to finance these expenses. One option that is growing in popularity is using life settlements to pay for long-term care. A life settlement allows policyholders to sell their life insurance policy for a lump sum, providing much-needed funds that can be used for care-related costs. Whether you’re facing the prospect of entering an assisted living facility, needing in-home care, or planning for future healthcare needs, a life settlement could offer a practical financial solution.

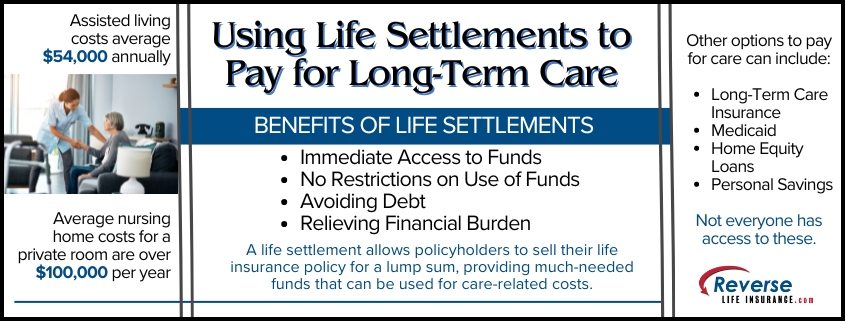

Understanding the Cost of Long-Term Care

The cost of long-term care can be staggering. According to the U.S. Department of Health and Human Services, the average nursing home costs for a private room are over $100,000 per year, and assisted living costs average around $54,000 annually. In-home care, while sometimes more affordable, can still cost thousands of dollars each month, especially if extensive medical or personal care is required.

Unfortunately, most traditional health insurance plans, including Medicare, provide limited coverage for long-term care. This means that individuals often need to rely on personal savings, family support, or alternative financial products to cover the costs.

What is a Life Settlement?

A life settlement is a financial transaction where a policyholder sells their life insurance policy to a third party in exchange for a lump sum payment. This payment is more than the policy’s cash surrender value but less than its death benefit. The buyer of the policy assumes responsibility for paying future premiums and becomes the beneficiary upon the policyholder’s death.

Life settlements are most commonly an option when an insured is over the age of 65, but they can also be an option for younger policyholders with serious health conditions, such as chronic or terminal illnesses.

Why Consider a Life Settlement?

For many, a life settlement offers a way to access the value of a life insurance policy while they are still alive, especially if the original purpose of the policy—such as income replacement or estate planning—is no longer relevant. The funds from a life settlement can be used for any purpose, but using life settlements to pay for long-term care is a particularly compelling reason to explore this option.

Benefits of a Life Settlement for Long-Term Care

- Immediate Access to Funds

Life settlements provide a lump sum payment that can be used to cover immediate care costs. This can be especially useful if savings or other financial resources are limited. - No Restrictions on Use of Funds

Unlike some long-term care insurance policies, there are no restrictions on how the funds from a life settlement can be used. This flexibility allows you to cover not only healthcare costs but also living expenses, home modifications, or even travel for medical treatments. - Avoiding Debt

By using the proceeds from a life settlement, individuals may be able to avoid taking on debt or exhausting retirement savings to pay for care. - Relieving Family Burden

Life settlements can help relieve the financial burden on family members who may otherwise feel compelled to contribute to the cost of care.

Comparing Life Settlements to Other Financial Options

When planning for long-term care, it’s essential to compare a life settlement to other financial options:

- Long-Term Care Insurance:

While long-term care insurance can be a great resource for covering nursing home or home care expenses, not everyone qualifies for a policy, and premiums can be prohibitively expensive for older individuals or those with pre-existing conditions. - Medicaid:

Medicaid is a government program that helps cover long-term care costs for low-income individuals, but it requires individuals to spend down their assets to qualify. This can be a significant disadvantage for those who wish to preserve their savings for family or other uses. A Medicaid life settlement may be an option in this scenario. - Home Equity Loans:

Some people turn to home equity loans or reverse mortgages to cover long-term care costs. While these options can provide substantial funds, they also require repayment, often leaving the homeowner in debt.

In contrast, a life settlement offers a debt-free way to tap into the value of an existing asset—your life insurance policy.

Key Considerations

Before pursuing a life settlement, there are a few important factors to consider:

- Impact on Beneficiaries

When you sell your life insurance policy through a life settlement, your beneficiaries will no longer receive the death benefit. If your policy was intended to provide financial security for loved ones, this may affect your decision. - Taxes

The proceeds from a life settlement may be taxable, depending on your situation. It’s important to consult with a tax advisor to understand how a life settlement could affect your tax liability. - Eligibility

Not all policies qualify for a life settlement. Generally, policies must have a death benefit of at least $100,000, and the insured person should be over a certain age or have specific health conditions. However, each situation is unique, and working with a life settlement provider can help clarify whether you qualify for a life settlement or a viatical settlement.

How to Get Started

If you think a life settlement could help you pay for long-term care, start by contacting us. Our platform allows direct buyers to evaluate your policy and provide you with an appraisal, allowing you to decide whether to move forward with a life settlement.

For more information on long-term care and financial planning, visit the U.S. Department of Health and Human Services at acl.gov/ltc and explore Medicaid eligibility requirements at medicaid.gov.

Using life settlements to pay for long-term care is an option worth considering for individuals who need financial flexibility in their later years. By accessing the value of a life insurance policy, policyholders can fund their care without dipping into savings or taking on debt.

With careful planning and the right guidance, a life settlement could be the key to securing the care you need while maintaining financial stability. To find out if you’re likely to qualify, please give us a call today at 800-727-7654.